Quick Summary: AI won’t replace auditors, but it will fundamentally transform their role. While artificial intelligence automates data-intensive tasks and improves efficiency, the audit profession still requires human judgment, skepticism, and ethical reasoning that machines can’t replicate. Auditors who embrace AI tools will thrive; those who resist risk obsolescence.

The question keeps surfacing in conference rooms and LinkedIn discussions: will artificial intelligence eventually replace auditors? It’s a reasonable concern given how rapidly AI is transforming professional services.

But here’s the thing—the answer isn’t a simple yes or no.

According to a Thomson Reuters Audit Survey, 68% of accounting firms are currently struggling to hire qualified talent, and 74% said their inability to attract and retain skilled professionals is a hurdle to achieving strategic goals. AI isn’t arriving to eliminate jobs. It’s arriving at precisely the moment when the profession desperately needs efficiency gains.

The International Auditing and Assurance Standards Board (IAASB) published findings from global Technology Quality Management roundtables in February 2026, exploring how emerging technologies—including artificial intelligence—are affecting audit and assurance engagements. Their conclusion? Technology is reshaping processes, not replacing professionals.

How AI Is Currently Transforming Audit Work

Artificial intelligence isn’t some distant future threat. It’s already embedded in audit workflows across major firms and internal audit departments.

Robotic process automation (RPA) and cognitive intelligence can execute audit tasks around the clock at an accelerated pace—in many cases, more than 90 percent faster than manual processes, according to Deloitte research on adopting automation capabilities for internal audit. That’s not theoretical. It’s happening now.

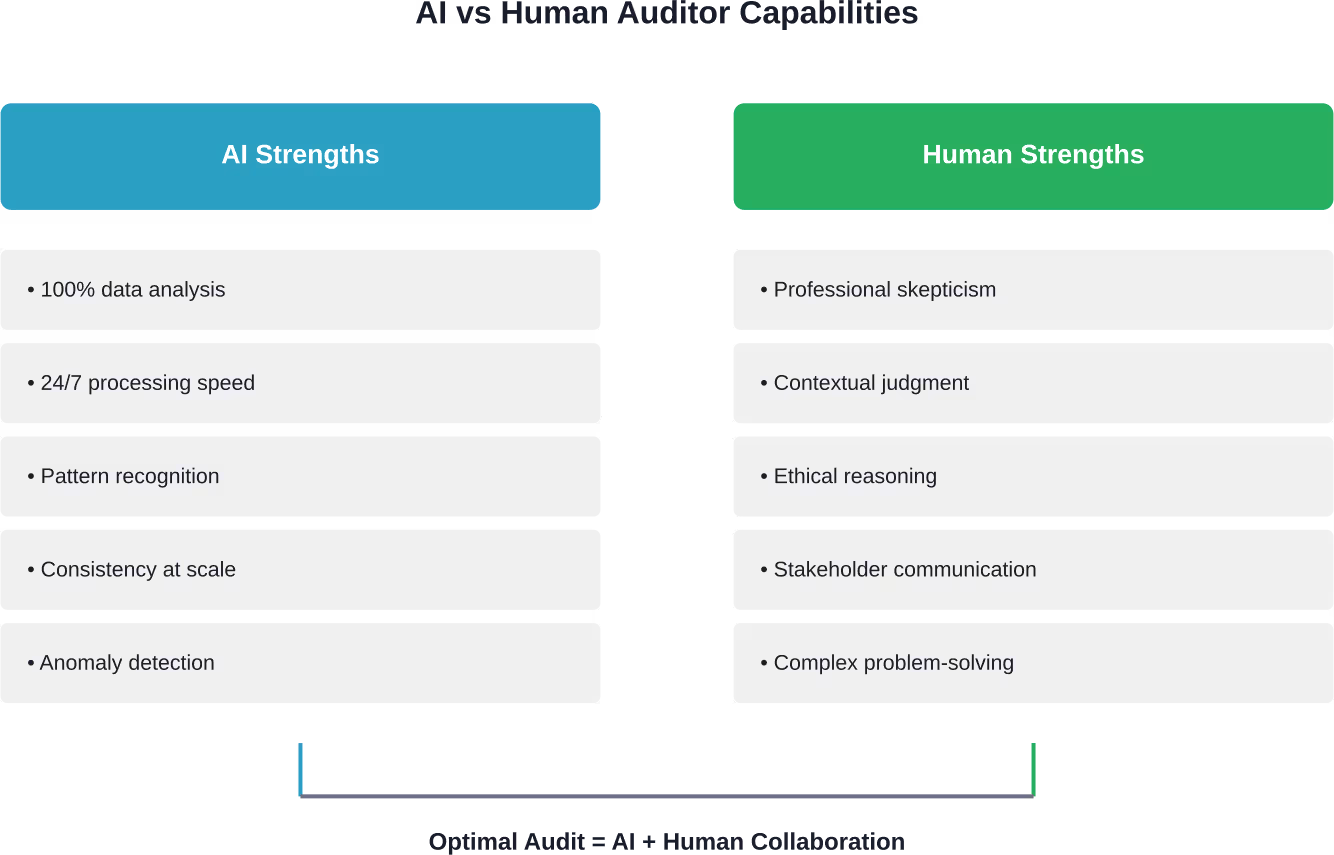

What does this look like in practice? AI systems analyze massive datasets that would take human auditors weeks to review. They identify anomalies, flag potential risks, and perform continuous monitoring instead of periodic sampling.

Take journal entry testing, for example. Traditionally, auditors would sample a small percentage of transactions. AI can now analyze 100% of journal entries, identifying unusual patterns or potentially fraudulent activity that statistical sampling might miss.

But wait—if AI can do all that, why do firms still need human auditors?

AI Development for Operational Use With AI Superior

AI Superior focuses on building AI systems that can be applied directly within business operations. The process typically starts with understanding the problem and evaluating available data, followed by model development and integration into existing workflows.

Considering AI for Internal Processes?

AI Superior can help with:

- developing AI solutions tailored to specific operational tasks

- assessing feasibility and data readiness

- integrating AI into existing systems and tools

👉 Contact AI Superior to discuss your project, data, and implementation approach

The Irreplaceable Human Element in Auditing

Data analysis is only one component of auditing. The profession fundamentally depends on judgment, skepticism, and contextual understanding that artificial intelligence simply can’t replicate.

According to the 2024 BDO Audit Innovation Survey, 54% of leaders expect their audit firm to use artificial intelligence and other advanced technologies to enhance the audit experience. Notice the language: enhance, not replace.

Consider what auditors actually do beyond number-crunching:

- Assessing management’s intent and organizational culture

- Evaluating the reasonableness of estimates and assumptions

- Understanding business context and industry-specific risks

- Applying professional skepticism to contradictory evidence

- Communicating complex findings to stakeholders

- Making ethical judgments in ambiguous situations

These aren’t tasks that can be automated away. They require human intelligence, experience, and professional judgment.

An AI system can flag that a company’s revenue recognition pattern looks unusual. But it takes a human auditor to investigate whether that pattern reflects legitimate business changes, aggressive accounting, or potential fraud.

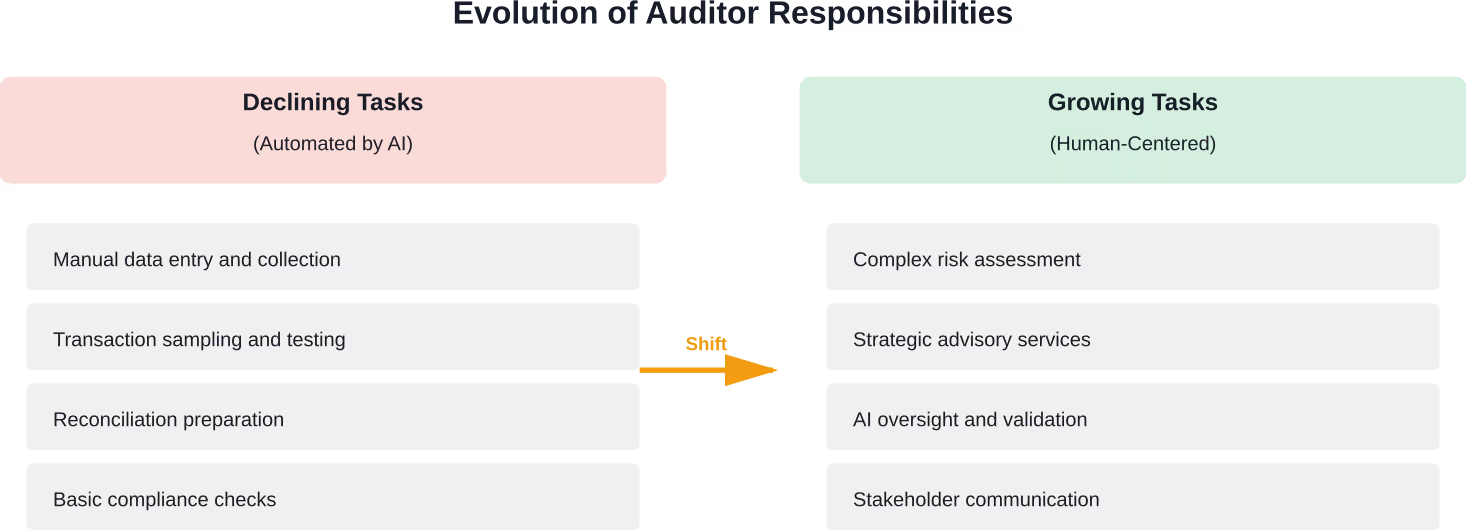

The Real Transformation: Changing Roles, Not Disappearing Jobs

So what’s actually happening to auditor roles? They’re evolving, not vanishing.

The widespread growth of GenAI-powered tools for audit firms has made it possible to scale quickly. For firms that haven’t yet committed to adapting, however, the performance gap with firms that have will soon start to reveal itself.

Auditors are spending less time on manual data collection and more time on analysis, risk assessment, and strategic advisory work. That’s not a downgrade—it’s an upgrade.

Junior auditors once spent weeks manually testing transactions and preparing reconciliations. Now AI handles those tasks, freeing junior staff to develop analytical and interpretive skills earlier in their careers.

Senior auditors and partners are shifting toward higher-value activities: complex judgment areas, client relationships, and strategic risk advisory. The technical grind gets automated. The strategic thinking gets emphasized.

According to industry research, auditors who’ve integrated AI tools report reduced burnout from repetitive tasks and increased job satisfaction from more intellectually engaging work.

Data Governance and the AI Implementation Challenge

Here’s where it gets complicated. Implementing AI in auditing isn’t as simple as flipping a switch.

More than two-thirds (69%) of finance leaders said establishing data governance and internal data management is a barrier to a smooth audit experience, followed by having the proper people and resources (60%), according to recent industry research.

Real talk: AI systems are only as strong as the data on which they’re trained and the frameworks that govern their use. Concerns about data security, privacy, and algorithmic bias represent legitimate risks that the profession must address.

The IAASB unveiled a new Technology Position in October 2024 to guide how it adapts its work to embrace the intersection of audit, assurance, and technology. In February 2026, the IAASB published feedback from global Technology Quality Management roundtables. This marks a significant step forward in enhancing the quality and relevance of standards in the face of rapid technological advancement.

| Implementation Challenge | Impact on Audit Firms | Required Response |

|---|---|---|

| Data governance frameworks | 69% cite as barrier to smooth audits | Establish clear data management protocols |

| Talent acquisition and retention | 68% struggling to hire qualified staff | Invest in AI training for existing teams |

| Technology integration | Performance gap emerging between early and late adopters | Commit to systematic technology adoption |

| Security and privacy concerns | Risk of data breaches and compliance issues | Implement robust cybersecurity measures |

What the SEC and Financial Regulators Are Saying

Regulatory bodies aren’t standing idle while AI transforms auditing. They’re actively examining the implications.

The SEC hosted a roundtable discussion on artificial intelligence in the financial industry on April 2, 2025. The event brought together industry leaders, academics, and regulators to discuss the risks, benefits, and governance of AI in finance and auditing.

The message from regulators is clear: AI tools must enhance audit quality, not compromise it. Firms adopting these technologies need robust governance frameworks to ensure AI-driven audits meet professional standards.

This regulatory attention isn’t about blocking innovation. It’s about ensuring that as the profession evolves, audit quality and public trust remain paramount.

The Skills Auditors Need to Thrive in an AI-Enhanced Profession

If the role is changing, what skills do auditors need to develop?

Technical accounting knowledge remains essential, but it’s no longer sufficient. Auditors now need a hybrid skill set that combines traditional audit expertise with technological fluency.

Critical skills for the AI era include:

- Data analytics and interpretation

- Understanding AI and machine learning fundamentals

- Critical thinking and professional skepticism

- Technology risk assessment

- Change management and adaptability

- Communication and stakeholder management

Deloitte’s Tech Trends 2026 report, published in February 2026, identifies five AI trends reshaping accounting opportunities. The emphasis is on auditors who can bridge the gap between technology capabilities and professional judgment.

The profession isn’t looking for people who can compete with AI at data processing. It’s looking for professionals who can leverage AI tools while applying uniquely human capabilities.

What This Means for Firms and Internal Audit Departments

The strategic implications extend beyond individual auditors to entire organizations.

Audit firms that aggressively adopt AI technologies are gaining competitive advantages in efficiency, quality, and scalability. Those that delay face growing performance gaps.

Internal audit departments are experiencing similar transformations. According to Deloitte research, automation technologies can increase efficiency throughout the internal audit life cycle while creating more value for the business and making better use of human talent.

But this isn’t just about buying software. Successful AI implementation requires:

- Investment in training and upskilling staff

- Redesigning workflows and methodologies

- Establishing governance frameworks for AI use

- Building partnerships between IT and audit functions

- Developing change management capabilities

Organizations that treat AI as purely a technology initiative rather than a strategic transformation typically struggle with adoption and realize limited benefits.

The Verdict: Transformation, Not Termination

So, will AI replace auditors? The evidence points to a clear conclusion: no, but the profession will look dramatically different.

Artificial intelligence is eliminating the tedious, repetitive aspects of audit work that drove many talented professionals out of the field. It’s enhancing capabilities, expanding what’s possible, and allowing auditors to focus on work that requires human judgment.

The auditors at risk aren’t those whose jobs will be automated away. They’re those who refuse to adapt and develop the skills needed for an AI-enhanced profession.

As the AICPA, IAASB, and other professional organizations emphasize, technology is a tool that serves the audit function—not a replacement for professional judgment and ethical reasoning.

The future belongs to auditors who embrace AI as a powerful ally rather than viewing it as an existential threat. That’s not speculation. It’s already happening across firms and internal audit departments worldwide.

Frequently Asked Questions

Will AI completely replace auditors in the future?

No. While AI will automate many data-intensive tasks, auditing fundamentally requires professional judgment, skepticism, and ethical reasoning that artificial intelligence cannot replicate. The profession will transform, with auditors focusing more on analysis, risk assessment, and advisory work rather than manual testing.

What audit tasks will AI automate first?

AI is already automating transaction testing, journal entry analysis, reconciliation preparation, anomaly detection, and compliance checking. According to Deloitte research, these automated processes can operate more than 90 percent faster than manual methods, allowing auditors to analyze 100% of data rather than statistical samples.

Do auditors need to learn programming to stay relevant?

Not necessarily. While understanding AI and data analytics fundamentals is increasingly valuable, auditors don’t need to become software developers. The critical skills involve knowing how to leverage AI tools, interpret their outputs, and apply professional judgment to the results.

How are professional organizations responding to AI in auditing?

Organizations like the IAASB, AICPA, and SEC are actively addressing AI’s impact. The IAASB published a Technology Position in October 2024 and held global roundtables on technology and quality management in early 2026. The SEC hosted a roundtable on AI in financial services in March 2025, focusing on governance and audit quality.

What’s the biggest challenge firms face implementing AI in audits?

According to recent research, 69% of finance leaders cite data governance and internal data management as the primary barrier. Other significant challenges include talent acquisition (68% of firms struggle to hire qualified staff), security concerns, and establishing proper oversight frameworks for AI systems.

Are junior auditor positions disappearing because of AI?

Junior positions are evolving rather than disappearing. While AI handles many tasks traditionally assigned to junior staff, firms still need entry-level auditors to develop analytical skills and professional judgment. The difference is that juniors now spend less time on manual data work and more time on substantive analysis earlier in their careers.

How can auditors prepare for an AI-driven profession?

Auditors should develop hybrid skill sets combining traditional audit expertise with data analytics, technology risk assessment, and critical thinking capabilities. Focus on areas where human judgment is essential: complex risk assessment, stakeholder communication, ethical reasoning, and professional skepticism that AI cannot replicate.