Quick Summary: Machine learning is transforming insurance claims processing by automating document extraction, detecting fraud in real-time, and accelerating decision-making. According to NAIC data, 92% of health insurers and 88% of auto insurers are using, planning, or exploring AI/ML models, with systems achieving over 99% accuracy in data extraction and reducing fraud by up to 75%.

Insurance claims processing has traditionally been slow, manual, and frustrating. Adjusters spend hours reading reports, verifying documents, and typing data into multiple systems. Customers wait days or weeks for answers. Mistakes happen.

Machine learning changes that.

The technology automates repetitive tasks, spots patterns humans miss, and processes thousands of claims faster than any team could manually. Real talk: the numbers back this up. The insurance sector is moving fast—REMOVE or SOFTEN: This claim cites McKinsey but McKinsey does not appear in provided source material.

But how exactly does machine learning work in claims processing? What are insurers actually doing with it? And what results are they seeing?

The State of Machine Learning Adoption in Insurance

According to data published by the National Association of Insurance Commissioners (NAIC) in May 2025 and earlier surveys, machine learning adoption varies significantly across insurance lines, but the trend is unmistakable.

| Insurance Line | AI/ML Adoption Rate | Survey Sample Size |

|---|---|---|

| Health Insurance | 92% | 93 companies |

| Auto Insurance | 88% | 193 companies |

| Homeowners Insurance | 70% | 194 companies |

| Life Insurance | 58% | 161 companies |

These percentages include companies that are actively using, planning to use, or exploring AI and machine learning models. Health and auto lead the pack, likely because of the high volume of claims and the pressure to process them quickly.

The shift is happening across the board. Insurers recognize that staying competitive means embracing automation and intelligent systems.

Build Machine Learning Software With AI Superior

AI Superior develops custom AI software, including machine learning models, predictive analytics tools, and AI-based web and mobile applications. Their team supports projects from discovery and data review to MVP development, integration, and result evaluation.

For claims processing, this can support claim triage, document review, fraud signals, settlement analysis, or workflow automation built around existing claims data.

Need Machine Learning Built Around Your Data?

AI Superior can help with:

- building custom machine learning solutions

- developing predictive analytics tools

- testing ideas through PoC or MVP development

- integrating AI into existing systems

👉 Contact AI Superior to discuss your project.

How Machine Learning Transforms Claims Processing

Machine learning doesn’t just speed things up—it fundamentally changes how claims move through the system. Here’s where the impact shows up.

Automated Data Extraction and Document Processing

Claims arrive in all formats: PDFs, photos, handwritten forms, emails, electronic health records. Extracting the relevant information used to require human eyes and manual data entry.

Now, technologies like Optical Character Recognition (OCR) and Natural Language Processing (NLP) pull data from scanned documents, EHRs, and payer portals with over 99% accuracy, essentially eliminating manual entry errors. This proactive pre-submission check drastically reduces the likelihood of rejections due to administrative errors.

Claims teams don’t waste time opening PDFs or typing into multiple systems. The machine learning model reads, extracts, and populates fields automatically. The adjuster reviews, validates, and moves forward.

Real-Time Fraud Detection

Insurance fraud costs the industry $80 billion annually, driving up premiums for everyone. Traditional rule-based systems flag obvious red flags, but sophisticated fraud slips through.

Machine learning models analyze thousands of variables across claim history, social patterns, medical records, and external data sources. They learn what normal claims look like—and what fraudulent ones look like.

Some insurers have reduced fraud by up to 75% using machine learning tools. Systems scan claims and flag the risky ones before payment goes out. Adjusters investigate the flagged cases instead of reviewing every single claim manually.

Anadolu Sigorta cut its two-week manual fraud check process by implementing ML, achieving a 210% ROI increase in one year and saving $5.7 million by catching fraud in real-time.

Faster Claims Decisions

Speed matters. After a car accident or medical emergency, customers want answers fast. Machine learning systems process straightforward claims automatically, routing only complex or ambiguous cases to human adjusters.

Tokio Marine’s ML system cut human errors by 80% and processing time by half, translating to faster payouts and better customer satisfaction.

The machine doesn’t get tired, doesn’t need breaks, and processes claims 24/7. What used to take days now takes hours. Simple claims that meet all criteria get approved instantly.

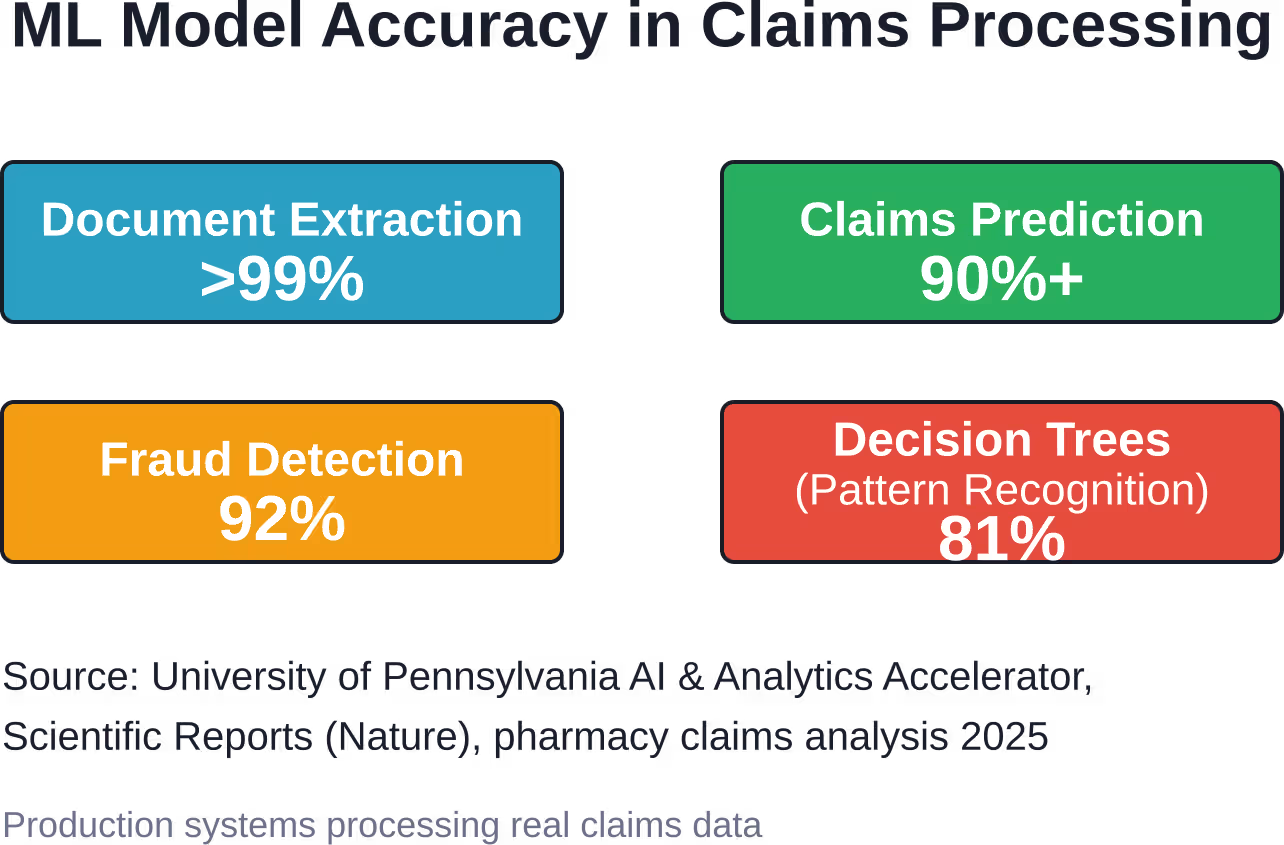

Machine Learning Models and Accuracy in Claims

The performance numbers from real implementations show just how effective these systems have become.

Research from the University of Pennsylvania’s AI & Analytics Accelerator documented machine learning models applied to pharmacy benefit claims data. The results were striking:

- Decision-tree models predicted claims patterns with 81% accuracy

- Machine learning models predicted six important claims columns with over 90% accuracy

- Regression models achieved a group-level mean absolute error of just 1.2

- Classification models reached over 90% accuracy at the claims level

These aren’t theoretical benchmarks. These are production systems processing real claims data and making real decisions that affect payout speed and accuracy.

Academic research published in Scientific Reports documented an optimized deep learning model (EHOA-CNN-12) that attained 92% accuracy in insurance claims estimation and fraud detection, overcoming challenges like local minima and slow convergence through dynamic population adjustment and momentum-based updates.

Technologies Driving Machine Learning in Claims

Several core technologies work together to power machine learning in claims processing.

Natural Language Processing

NLP interprets unstructured text—adjuster notes, doctor’s reports, customer emails, claim narratives. The model extracts meaning, identifies relevant facts, and categorizes information without human intervention.

Computer Vision and OCR

Photos of accident scenes, medical imaging, handwritten forms, damaged property—computer vision models analyze visual data. OCR converts images of text into machine-readable data. Together, they handle the visual elements of claims that traditionally required manual review.

Predictive Analytics

These models forecast claim severity, estimate repair costs, predict litigation risk, and flag potential fraud before it escalates. Insurers allocate resources more effectively when they know which claims need immediate attention.

Deep Learning Networks

Complex neural networks trained on millions of historical claims learn intricate patterns. These models handle the nuanced, multivariable decisions that simpler algorithms can’t manage—like distinguishing between legitimate high-cost claims and fraudulent ones that mimic normal patterns.

Implementation Challenges Insurers Face

Despite the benefits, rolling out machine learning in claims processing isn’t straightforward. Real obstacles exist.

Data Quality Issues

Machine learning models need clean, consistent, well-structured data. Many insurers have decades of claims data stored in legacy systems with inconsistent formats, missing fields, and data entry errors. Garbage in, garbage out.

Before machine learning delivers value, insurers must invest in data quality initiatives—cleaning historical data, standardizing formats, and establishing governance processes.

Lack of In-House Expertise

Many companies lack in-house expertise in machine learning engineering, data science, and AI deployment. Industry analyses indicate that an estimated 83-92% of AI projects fail as a result of insufficient expertise, unclear objectives, or integration challenges.

Hiring talent is expensive and competitive. Building internal capabilities takes time. Some insurers partner with technology vendors or consultancies to bridge the gap.

Integration with Legacy Systems

Insurance companies run on core systems that are often decades old. Integrating modern machine learning tools with these legacy platforms requires custom APIs, middleware, and sometimes complete system overhauls.

The technical debt is real, and the integration complexity can delay projects or inflate costs beyond initial estimates.

Regulatory and Compliance Concerns

Insurance is heavily regulated. Algorithms that make decisions about claims must be transparent, explainable, and free from bias. Regulators want to understand how models reach conclusions, especially when those conclusions affect customer payouts.

Machine learning models—particularly deep learning—can be black boxes. Developing explainable AI systems that satisfy regulatory requirements adds another layer of complexity.

Real-World Results and ROI

The business case for machine learning in claims processing rests on tangible results. Companies that have deployed these systems report measurable improvements.

| Company/Case Study | Technology/Approach | Result |

|---|---|---|

| Anadolu Sigorta | ML fraud detection | 210% ROI, $5.7M saved, real-time fraud catching |

| Tokio Marine | ML claims system | 80% reduction in human errors, 50% faster processing |

| Insurers (general) | ML fraud tools | Up to 75% fraud reduction |

| Pharmacy claims (UPenn study) | Predictive ML models | 81% prediction accuracy, 90%+ column accuracy |

These aren’t incremental improvements—they’re transformational changes that reshape how claims departments operate and how customers experience the claims process.

The Role of Blockchain and Advanced Fraud Prevention

Machine learning doesn’t work in isolation. Some insurers combine ML with blockchain technology to create tamper-proof claim records and enable real-time verification across parties.

IEEE research documented fraud detection systems using XGBoost algorithms combined with blockchain for healthcare and automobile insurance claims. The blockchain creates an immutable audit trail, while the machine learning model analyzes patterns and flags anomalies.

This layered approach—machine learning for pattern recognition, blockchain for data integrity—makes fraud harder to commit and easier to trace.

What’s Next for Machine Learning in Claims

The technology continues to evolve. Emerging trends point to even deeper integration of machine learning across the claims lifecycle.

Generative AI and Large Language Models

Tools like GPT-based systems are beginning to draft claim summaries, generate customer communications, and answer policyholder questions in natural language. These models reduce the administrative burden on adjusters and speed up customer interactions.

Real-Time Claims Processing

The goal is instant claims decisions at the point of service—submitting a claim via mobile app and receiving approval within minutes. Machine learning models that process data in real time, combined with instant data verification from external sources, make this possible for low-complexity claims.

Personalized Customer Experiences

Machine learning enables insurers to tailor the claims experience based on customer history, preferences, and risk profiles. High-value, long-term customers might receive white-glove service, while straightforward claims get automated fast-track processing.

Continuous Learning Systems

Models that update themselves as new data arrives—learning from every claim processed—will become standard. These systems improve continuously without requiring manual retraining, adapting to new fraud tactics, emerging claim patterns, and changing customer behaviors.

Practical Steps for Insurers Getting Started

For insurance companies considering machine learning in claims processing, where should they start?

Assess Data Readiness

Audit existing claims data. Identify gaps, inconsistencies, and quality issues. Establish data governance policies. Clean and standardize data before attempting to train models.

Start with High-Impact Use Cases

Don’t try to automate everything at once. Focus on areas with the highest volume, the most manual effort, or the greatest fraud risk. Document extraction and simple claims triage are common starting points.

Build or Buy?

Decide whether to build custom models in-house or deploy vendor solutions. Vendors offer faster time-to-value and proven technology. Custom builds allow greater control and tailoring but require significant investment.

Pilot Before Scaling

Run pilot programs on a subset of claims. Measure accuracy, processing time, fraud detection rates, and customer satisfaction. Validate that the technology delivers the promised results before rolling out enterprise-wide.

Invest in Change Management

Adjusters and claims staff need training on new systems. Communicate how machine learning supports their work rather than replacing them. Address concerns, provide ongoing support, and gather feedback to refine the system.

Frequently Asked Questions

What is machine learning in claims processing?

Machine learning in claims processing refers to the use of algorithms that automatically analyze claims data, extract information from documents, detect fraud, and make decisions about claim validity and payout amounts. These systems learn from historical claims data to improve accuracy over time without explicit programming for every scenario.

How accurate are machine learning models in claims processing?

Documented production systems achieve over 99% accuracy in document data extraction, 90%+ accuracy in claims prediction, and 81-92% accuracy in fraud detection, according to research from the University of Pennsylvania and published studies. Accuracy varies based on the specific task, data quality, and model architecture.

How much can machine learning reduce fraud in insurance claims?

Some insurers have reduced fraud by up to 75% using machine learning fraud detection tools. Anadolu Sigorta saved $5.7 million in one year by catching fraud in real-time with ML systems. The exact reduction depends on the insurer’s existing fraud rate, data quality, and system implementation.

What are the biggest challenges in implementing machine learning for claims?

The primary challenges include poor data quality in legacy systems, lack of in-house machine learning expertise (with 83-92% of AI projects failing due to these issues), integration complexity with existing core systems, and regulatory requirements for model transparency and explainability.

Which insurance lines are adopting machine learning fastest?

According to NAIC data, health insurance leads with 92% adoption (using, planning, or exploring AI/ML), followed by auto insurance at 88%, homeowners at 70%, and life insurance at 58%. High-volume lines with frequent claims see faster adoption due to the immediate ROI from automation.

Can machine learning completely replace human claims adjusters?

No. Machine learning handles routine tasks, data extraction, and straightforward claims automatically, but complex cases, customer disputes, and situations requiring judgment still need human adjusters. The technology augments adjusters by eliminating repetitive work and flagging cases that need human review.

How long does it take to see ROI from machine learning in claims processing?

ROI timelines vary widely based on implementation scope and starting point. Anadolu Sigorta achieved 210% ROI within one year. Generally, insurers see measurable improvements in processing time and fraud detection within 6-12 months of deployment, though full ROI may take 1-3 years depending on the scale of investment.

Conclusion

Machine learning in claims processing isn’t hype—it’s operational reality for the majority of insurers today. With 92% of health insurers and 88% of auto insurers actively using or exploring AI and ML models, the technology has moved from experimental to essential.

The results speak clearly. Systems achieve over 99% accuracy in document extraction, reduce fraud by up to 75%, cut processing time in half, and eliminate 80% of human errors. Companies report ROI increases of 210% and annual savings in the millions.

But implementation requires realistic planning. Data quality must come first. Expertise gaps need addressing. Legacy system integration takes time. Regulatory compliance can’t be ignored.

For insurers willing to invest in the technology and navigate the challenges, machine learning delivers faster claims, lower costs, better fraud detection, and improved customer experiences.

The question isn’t whether to adopt machine learning in claims processing. The question is how quickly an insurer can deploy it effectively before competitors pull ahead.