Quick Summary: Machine learning has transformed finance through algorithmic trading, fraud detection, risk assessment, and customer service automation. According to Bank of England data, 75% of major financial firms now deploy AI in operations, up from 53% in 2022. These technologies enable real-time pattern recognition in market data, automated compliance monitoring, and personalized financial recommendations at scale.

Financial services have undergone a dramatic shift. Where human analysts once pored over spreadsheets for hours, algorithms now process millions of transactions in seconds, spotting patterns invisible to the naked eye.

But here’s the thing—this isn’t just about speed. Machine learning fundamentally changes what’s possible in finance.

Recent 2026 benchmarks show that standalone generative agents (GenAI-Agents) now achieve 0.3% error rates in document verification. Now imagine applying that same improvement trajectory to credit decisions, market predictions, and fraud detection.

The Rapid Adoption of Machine Learning in Financial Services

The numbers tell a compelling story. According to Bank of England research published in 2024, 75% of surveyed financial institutions now use some form of AI in their operations. That’s a jump from 53% just two years earlier.

This includes all major UK and international banks, insurers, and asset managers that participated in the study.

Data availability has exploded alongside computing power. The Federal Reserve highlighted that in 2013, 90% of the world’s data had been created in the prior two years. By 2016, that same proportion—90%—had been generated in just the previous year alone.

Financial institutions suddenly had fuel for their machine learning engines. Public cloud providers began offering pre-trained models through developer-friendly interfaces, lowering the barrier to entry dramatically.

Build Machine Learning Software With AI Superior

AI Superior develops custom AI software, including machine learning models, AI-based applications, web and mobile apps, and custom software products. Their team can support projects from discovery and data review to MVP development, integration, and result evaluation.

For finance teams, this can support use cases like fraud detection, risk scoring, customer behavior analysis, forecasting, or decision-support tools built around existing business data.

Need Machine Learning Built Around Your Data?

AI Superior can help with:

- building custom machine learning solutions

- testing ideas through PoC or MVP development

- developing predictive analytics tools

- integrating AI into existing systems

👉 Contact AI Superior to discuss your project.

Core Applications Transforming Financial Operations

Fraud Detection and Prevention

Financial fraud costs consumers billions annually. The Federal Trade Commission reported that in 2019 alone, people lost more than $1.9 billion to fraud—and that represents only a fraction of all fraudulent activity banks encounter.

Machine learning excels at spotting anomalies in transaction patterns. Traditional rule-based systems flag specific triggers—say, a purchase in a foreign country. But ML models analyze behavioral variables such as transaction timing, merchant categories, device characteristics, and typing rhythms.

The algorithms learn what “normal” looks like for each customer, then identify deviations that warrant investigation. This approach catches sophisticated fraud schemes that simple rules miss entirely.

Real talk: false positives remain a challenge. Banks must balance fraud prevention against customer friction. Nobody wants their card declined while traveling legitimately.

Algorithmic Trading and Market Prediction

Trading floors aren’t what they used to be. Algorithms now execute the majority of equity trades, making split-second decisions based on market data, news sentiment, and statistical patterns.

Recent research from arXiv examined machine learning trading strategies using Bitcoin data from 2024. An LSTM (Long Short-Term Memory) neural network achieved 65.23% cumulative returns, outperforming both a LightGBM model at 53.38% and a simple buy-and-hold strategy at 42.51%.

Even after accounting for 0.1% transaction fees, the LSTM strategy maintained 53.23% returns compared to LightGBM’s 39.78%—though it generated 120 trades versus 136 for the gradient boosting approach.

Classification accuracy metrics showed LightGBM at 0.5840 versus LSTM’s 0.5611. Modest improvements in prediction accuracy can translate into substantial portfolio differences when compounded across thousands of trades.

Risk Assessment and Credit Scoring

Banks traditionally evaluated creditworthiness using a handful of variables—income, existing debt, payment history. Machine learning models incorporate hundreds of features, including less obvious signals like utility payment consistency or educational background.

This expanded feature set helps lenders make more nuanced decisions. Someone with a thin credit file might still demonstrate creditworthiness through alternative data signals that traditional scoring overlooks entirely.

But wait—there’s a significant challenge here. The Federal Reserve has emphasized the importance of ensuring AI models produce equitable outcomes. Models trained on historical data can perpetuate past biases unless carefully designed and monitored.

Regulators require that credit decisions remain explainable and fair across demographic groups. This isn’t just an ethical imperative—it’s a legal one under fair lending laws.

Customer Service and Chatbots

Bank of England research indicates customer support enhancement is among the surveyed AI applications. Chatbots handle routine queries—balance checks, transaction histories, basic troubleshooting—freeing human agents for complex issues.

Natural language processing has improved dramatically. Early chatbots frustrated users with rigid, keyword-matching responses. Modern systems powered by large language models understand context, handle follow-up questions, and even detect customer sentiment.

That said, most banks maintain human escalation paths. Nobody wants an algorithm making judgment calls on disputed charges or sensitive account issues.

Internal Process Optimization

Bank of England research indicates internal process optimization as a significant AI application area among surveyed institutions.

This includes document processing, compliance monitoring, and workflow automation. Machine learning models extract data from unstructured documents—loan applications, legal contracts, regulatory filings—with accuracy approaching or exceeding human performance.

Remember that Federal Reserve statistic about image recognition? Error rates dropped to 0.3%, compared to 5% for humans working alone. The combined AI-human approach achieved just 0.5% errors.

Apply that same collaborative model to regulatory compliance. Algorithms screen millions of transactions for suspicious patterns, flagging outliers for human review. The combination catches more violations while reducing false positives that waste investigator time.

| Application Area | Adoption Rate | Primary Benefit |

|---|---|---|

| Internal process optimization | Significant | Efficiency and accuracy |

| Customer support | Notable | 24/7 availability, cost reduction |

| Foundation models (LLMs) | Emerging | Natural language understanding |

Economic Impact and Productivity Gains

The macroeconomic implications extend beyond individual firms. OECD analysis suggests that AI diffusion could contribute between 0.4 and 1.3 percentage points to annual labor productivity growth in G7 economies over the next decade.

That range reflects uncertainty about adoption pace and implementation effectiveness. The higher end assumes rapid deployment and successful integration across sectors. Even the conservative estimate represents meaningful economic acceleration.

Financial services sit at the forefront of this transformation. These institutions have the data infrastructure, technical talent, and capital to invest in sophisticated ML systems.

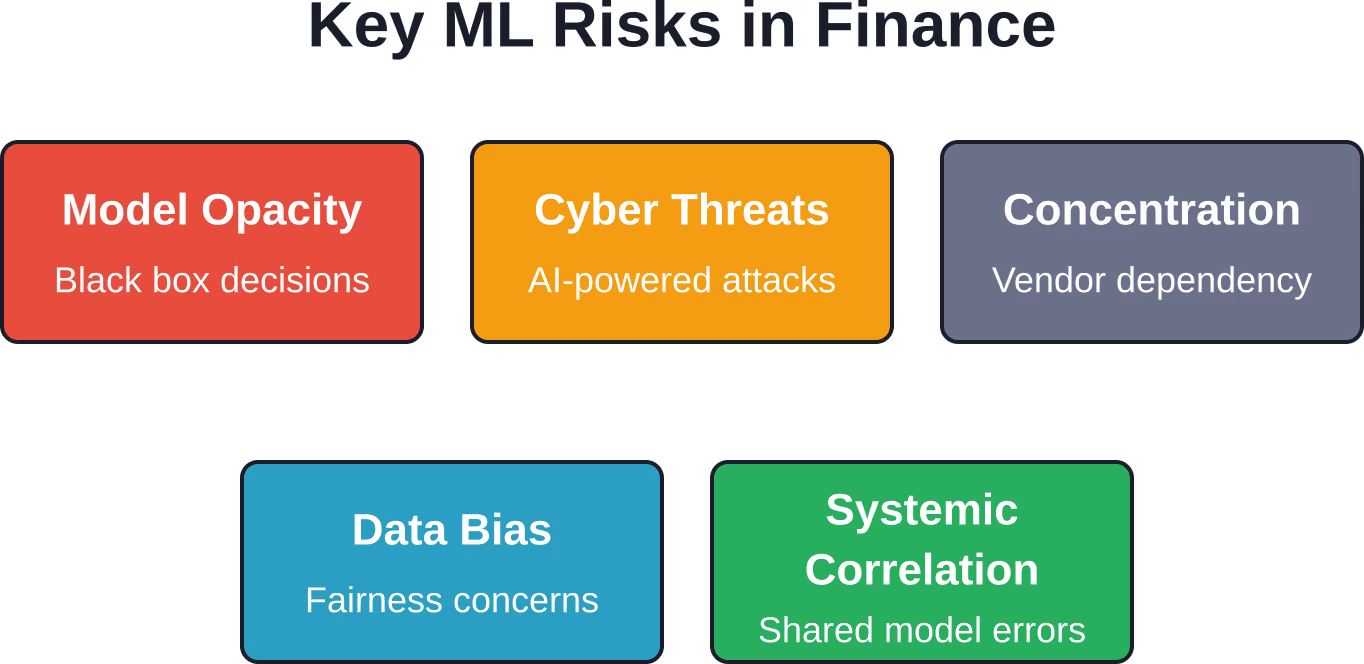

Emerging Risks and Stability Concerns

Rapid adoption brings new vulnerabilities. The Bank for International Settlements has examined financial stability implications of widespread AI deployment, identifying several concern areas.

Model Risk and Opacity

Deep learning models often function as “black boxes.” A neural network might make accurate predictions without offering clear explanations for its decisions. This opacity complicates risk management and regulatory oversight.

When models fail—and they occasionally do—the consequences propagate quickly. If multiple institutions use similar models trained on similar data, they might make correlated errors during market stress.

Cybersecurity Threats

Machine learning creates new attack vectors. Cybersecurity vulnerabilities including AI-powered phishing attacks represent emerging concerns identified in BIS research on AI financial stability implications. Adversaries use language models to craft convincing fake communications at scale.

Deepfake technology poses risks for authentication systems relying on voice or video verification. Financial institutions must continuously update security measures to counter evolving threats.

Concentration and Vendor Dependencies

Many institutions rely on third-party AI services from a small number of cloud providers. This concentration creates systemic risk—a major outage or security breach affecting one provider could disrupt multiple financial institutions simultaneously.

Regulators monitor these dependencies closely. The Bank of England noted that understanding interconnections through technology vendors has become a financial stability priority.

Regulatory Response and Governance

Policymakers walk a tightrope—fostering innovation while managing risks. The Federal Reserve has hosted symposiums on responsible AI use, bringing together researchers, industry practitioners, and consumer advocates.

Governor Lael Brainard emphasized in 2021 that supporting responsible AI adoption requires understanding both potential benefits and risks to equitable outcomes. Regulatory frameworks continue evolving as use cases mature.

Banks must maintain robust model governance: documentation of training data, validation procedures, ongoing performance monitoring, and clear accountability structures. When algorithms make consequential decisions affecting consumers, institutions bear responsibility for outcomes.

The Road Ahead

Foundation models and large language models represent an emerging frontier in financial AI applications.

These models excel at understanding natural language, generating text, and even writing code. Potential applications include automated report generation, contract analysis, and sophisticated customer interactions.

But foundation model deployment raises new questions. These systems sometimes produce plausible-sounding but factually incorrect outputs—so-called “hallucinations.” Using them for financial advice or regulatory compliance requires careful safeguards.

The technology continues advancing rapidly. Computational power grows, training techniques improve, and data accumulates. What seemed impossible five years ago has become routine; what seems futuristic today may be standard practice tomorrow.

Frequently Asked Questions

How widely is machine learning currently used in finance?

According to Bank of England research from 2024, 75% of major financial institutions now deploy some form of AI in their operations, up significantly from 53% in 2022. This includes all large UK and international banks, insurers, and asset managers surveyed. The most common applications are internal process optimization and customer support enhancement.

Can machine learning models really outperform traditional trading strategies?

Research evidence suggests ML models can generate superior returns under certain conditions. ArXiv research examining 2024 Bitcoin trading found LSTM neural networks achieved 65.23% cumulative returns compared to 42.51% for buy-and-hold strategies. However, these results reflect specific market conditions and asset classes. Performance varies significantly based on model architecture, training data quality, and market regime.

What are the biggest risks of using AI in financial services?

The Bank for International Settlements identifies several key concerns: model opacity making risk assessment difficult, cybersecurity vulnerabilities including AI-powered phishing attacks, concentration risk from shared technology vendors, potential for systemic correlation when multiple institutions use similar models, and fairness concerns around biased training data producing inequitable outcomes.

How much could AI improve economic productivity?

OECD analysis projects that AI diffusion could contribute between 0.4 and 1.3 percentage points to annual labor productivity growth in G7 economies over the next decade. The range reflects uncertainty about adoption pace and implementation success. Financial services, with robust data infrastructure and technical capacity, are positioned to capture gains on the higher end of this spectrum.

Do regulators support machine learning adoption in banking?

Regulatory bodies take a balanced approach—encouraging innovation while managing risks. The Federal Reserve has hosted symposiums on responsible AI use and published research on applications. Regulators require that institutions maintain robust model governance, ensure decisions remain explainable and fair, and establish clear accountability for algorithmic outcomes. The focus is on responsible deployment rather than restriction.

What’s the difference between traditional rules-based systems and machine learning in fraud detection?

Rule-based systems flag specific predetermined triggers, like foreign transactions or unusually large purchases. Machine learning models analyze behavioral variables such as transaction timing, merchant patterns, device characteristics, and typing rhythms—learning what constitutes “normal” behavior for each customer. This approach catches sophisticated fraud schemes that evade simple rules, though managing false positives remains an ongoing challenge.

Will AI replace human financial analysts and advisors?

Current evidence suggests augmentation rather than wholesale replacement. The Federal Reserve noted that combining AI with human judgment produces better outcomes than either alone—image recognition error rates achieved 0.5% for AI-human teams versus 0.3% for AI alone or 5% for humans alone. Complex decisions requiring contextual understanding, ethical judgment, or relationship management still benefit from human expertise, while algorithms handle data-intensive analysis and routine tasks.

Conclusion

Machine learning has moved from experimental technology to core infrastructure in modern finance. Three-quarters of major institutions now deploy these systems for everything from fraud prevention to algorithmic trading to customer service.

The productivity gains are real—potentially adding over a percentage point to annual GDP growth across developed economies. Financial institutions that successfully integrate ML capabilities gain competitive advantages in efficiency, risk management, and customer experience.

But the technology brings risks alongside opportunities. Model opacity, cybersecurity vulnerabilities, concentration concerns, and fairness challenges require ongoing attention from both institutions and regulators.

The trajectory points toward deeper integration. As foundation models mature and computational power grows, the boundary between possible and impossible continues shifting. Financial professionals who understand both the capabilities and limitations of machine learning will be best positioned to navigate this evolving landscape.

Ready to explore how machine learning could transform your financial operations? Start by identifying high-impact use cases where pattern recognition or process automation could deliver measurable value—then build governance structures ensuring responsible deployment from day one.