Quick Summary: Predictive analytics in lending uses historical data, machine learning algorithms, and real-time information to forecast borrower behavior, assess credit risk, and prevent loan defaults. Financial institutions deploy models like Random Forest, XGBoost, and neural networks to improve approval accuracy, reduce fraud losses, and comply with regulatory requirements from the CFPB and Federal Reserve.

Lending institutions face mounting pressure to approve creditworthy borrowers while keeping default rates low. Traditional credit scoring alone doesn’t cut it anymore.

Predictive analytics applies statistical algorithms and machine learning to historical loan data, alternative data sources, and behavioral patterns. The goal? Forecast which applicants will repay and which carry higher risk.

Research demonstrates that artificial neural networks can improve default prediction rates by as much as 20% over classical methods. That’s not incremental improvement—it’s a fundamental shift in how financial institutions manage risk.

What Is Predictive Analytics in Lending?

At its core, predictive analytics examines patterns in past lending outcomes to forecast future results. Lenders feed their systems years of loan performance data—payment histories, defaults, prepayments, recoveries—and train algorithms to spot the warning signs of trouble.

Modern systems incorporate far more than credit bureau scores. Employment stability, transaction velocity, even home search behavior can signal a borrower’s financial trajectory.

The process typically unfolds in four stages:

- Data collection from credit bureaus, transaction logs, application forms, and third-party sources

- Feature engineering to transform raw data into predictive variables

- Model training using historical outcomes to identify risk patterns

- Real-time scoring that applies trained models to new applications

According to Fannie Mae’s 2025 lender sentiment survey, 55% of mortgage lenders plan to pilot or expand AI and machine learning tools this year, with the majority targeting underwriting and risk assessment as their first application.

Apply Predictive Analytics in Lending with AI Superior

AI Superior builds predictive models on financial and behavioral data to support credit assessment, risk analysis, and decision workflows. They focus on models that integrate into existing systems, starting with data assessment and a working prototype before scaling.

Looking to Use Predictive Analytics in Lending?

AI Superior can help with:

- evaluating financial and customer data

- building predictive models

- integrating models into existing systems

- refining outputs based on results

👉 Contact AI Superior to discuss your project, data, and implementation approach.

How Machine Learning Models Perform Against Traditional Methods

Here’s where the numbers get interesting. Academic research comparing default prediction accuracy reveals stark differences between traditional statistical methods and modern machine learning approaches.

Logistic regression—the traditional workhorse—produced 79% accuracy with a ROC-AUC of 0.58. But it identified only 22% of actual defaulters. That’s a critical weakness when imbalanced datasets contain far more successful loans than defaults.

Random Forest increased recall to 68%, demonstrating better sensitivity to defaults, though overall accuracy dropped to 65%.

XGBoost hit 86% accuracy with a ROC-AUC of 0.74, though its recall for actual defaulters remained low at just 2.4%.

The clear winner? MLP neural networks achieved 95% accuracy with 0.95 balanced precision and recall. These models learn complex non-linear relationships that simpler algorithms miss entirely.

Real-World Applications Across Lending Segments

Banks deploy predictive models differently depending on the loan type and risk profile.

Credit Card Lending

The U.S. credit card market tops $1 trillion, making even small improvements in default prediction worth millions. Card issuers monitor transaction patterns, payment timing, balance utilization, and spending category shifts to spot early warning signs.

Machine learning models flag behavioral changes—sudden cash advances, minimum-only payments, maxed-out limits—that precede default by three to six months. That advance notice lets issuers intervene with payment plans or credit line adjustments before losses materialize.

Mortgage Risk Assessment

Mortgage lenders incorporate property-level data, neighborhood trends, and borrower search behavior into their risk models. One emerging approach leverages home search data—how long borrowers spend researching, how many properties they view, whether they’re searching in declining markets—as predictive signals.

Modern scoring models like FICO Score 10T use trended data to improve precision in default forecasting.

Commercial Lending

Business loans require different risk signals. Lenders analyze cash flow volatility, supplier payment patterns, customer concentration risk, and industry-specific economic indicators.

Continuous loan monitoring systems track commercial borrowers in near-real-time, closing the risk visibility gap that plagues quarterly review cycles. If a borrower’s customer base suddenly contracts or receivables age past normal terms, the model flags the loan for immediate review.

Fraud Detection and Prevention

Fraud costs lenders billions annually. According to the Federal Trade Commission, consumers reported losing more than $10 billion to fraud in 2023, and these figures continued to escalate through 2025.

Check fraud exploded in recent years. From February to August 2023, the Financial Crimes Enforcement Network noted over 15,000 reports related to check fraud, associated with more than $688 million in transactions (including both actual and attempted fraud).

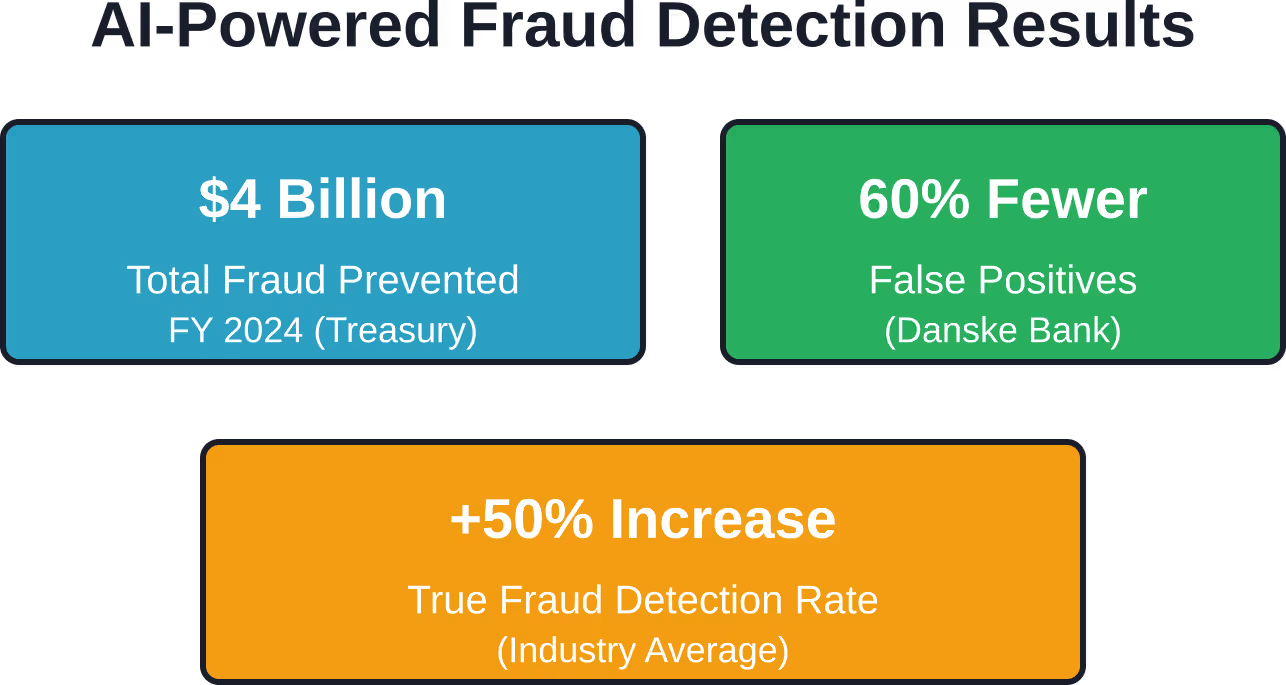

But here’s where AI delivers measurable impact: the U.S. Treasury announced that machine learning AI prevented and recovered over $4 billion in fraud in fiscal year 2024.

Modern fraud detection goes beyond simple rule engines. Machine learning models establish baseline behavioral profiles for each account, then flag deviations—unusual transaction locations, atypical purchase categories, velocity spikes—in milliseconds.

Danske Bank’s fraud detection implementation achieved approximately 60% fewer false positives alongside a 50% increase in true-fraud detection. That dual improvement matters: fewer false alarms reduce customer friction while better detection cuts actual losses.

Regulatory Compliance and Explainability Requirements

Here’s where things get thorny. Federal law requires lenders to explain specific reasons for denying credit applications, even when using complex algorithms.

The Consumer Financial Protection Bureau issued guidance in September 2023 confirming that federal anti-discrimination law requires companies to provide specific reasons for adverse actions. There’s no exception for black-box credit models using complex algorithms.

That creates a real challenge. Neural networks achieve superior accuracy precisely because they capture non-linear interactions that humans can’t easily articulate. But CFPB regulations under the Equal Credit Opportunity Act demand accurate, specific explanations.

Lenders can’t simply use CFPB sample adverse action forms and checklists if they don’t reflect the actual reason for the denial. The model must produce interpretable feature importance scores that translate into compliant adverse action notices.

Building Compliant Risk Models

Financial institutions address this tension through several approaches:

- Layer interpretable models (decision trees, rule-based systems) on top of complex algorithms to generate explanations

- Use SHAP values or LIME techniques to decompose individual predictions into feature contributions

- Maintain model documentation showing feature selection, validation testing, and bias audits

- Implement human review processes for borderline cases where model confidence is low

The Federal Reserve emphasized in November 2024 that discussions of artificial intelligence inevitably center on two main points: risks and benefits. Institutions must balance the performance gains from advanced models against the operational and legal risks of insufficient transparency.

Alternative Data Sources Transform Credit Decisions

Traditional credit bureau data tells an incomplete story. Millions of consumers lack sufficient credit history—the “credit invisible” population that traditional scoring excludes.

Predictive models increasingly incorporate alternative data:

| Data Category | Predictive Signals | Risk Considerations |

|---|---|---|

| Bank Transaction Data | Income stability, savings patterns, recurring payments, overdraft frequency | Privacy concerns, data aggregation consent requirements |

| Utility and Rent Payments | Consistent payment history for consumers without traditional credit | Reporting infrastructure gaps, data standardization challenges |

| Employment and Income Verification | Job tenure, income growth trajectory, employer stability | Real-time verification costs, informal economy exclusions |

| Behavioral Analytics | Application completion patterns, time-of-day behaviors, device usage | Potential proxy discrimination, difficult to explain in adverse actions |

Each data source introduces new predictive power and new compliance obligations. Lenders must ensure alternative data doesn’t create disparate impact on protected classes while still delivering better risk differentiation.

Implementation Challenges Financial Institutions Face

Deploying predictive analytics isn’t plug-and-play. Banks encounter real obstacles.

Data Quality and Integration

Legacy core banking systems weren’t designed for real-time analytics. Loan data lives in one system, transaction data in another, customer demographics in a third. Building unified data pipelines requires significant infrastructure investment.

Poor data quality undermines model performance. Missing fields, inconsistent formats, outdated records—each introduces noise that degrades predictions. AI systems can help organizations address data quality issues more efficiently.

Model Validation and Testing

Federal Reserve SR 11-7 guidance requires banks to validate models before deployment and monitor performance continuously. That means establishing separate validation teams, documenting model assumptions, testing against holdout data, and auditing for bias.

Small and mid-sized institutions often lack the staff or expertise to meet these requirements. Third-party model risk management creates its own challenges—lenders remain responsible for vendor model failures.

Change Management and Staff Training

Underwriters accustomed to manual review processes resist black-box systems that override their judgment. Successful implementations invest heavily in training, demonstrate model accuracy on historical portfolios, and preserve human override authority for edge cases.

Measuring Return on Investment

CFOs demand quantifiable results. Predictive analytics delivers ROI through several channels:

- Reduced charge-offs: Better default prediction directly cuts loan losses. Reduced charge-offs from better default prediction represent significant savings for lending institutions.

- Improved approval rates: More accurate risk assessment lets lenders approve previously marginal applicants with confidence. That expands the addressable market without increasing risk.

- Operational efficiency: Automated decisioning reduces manual underwriting costs. Faster approvals improve customer experience and conversion rates.

- Fraud prevention: As demonstrated by the Treasury’s $4 billion recovery, AI-powered fraud systems deliver returns that dwarf implementation costs.

HSBC’s anti-money laundering implementation achieved 2-4× more true positives with approximately 60% reduction in alert volumes. That combination—better detection with less noise—frees compliance staff to focus on genuine risks.

Ethical Considerations and Bias Mitigation

Predictive models inherit biases from training data. If historical lending decisions reflected discriminatory practices, models trained on that data perpetuate those patterns.

The CFPB has been clear: there’s no AI exception to anti-discrimination law. Lenders must actively test for disparate impact across protected classes—race, gender, age, national origin.

Bias mitigation strategies include:

- Removing protected attributes from training data (though proxy variables remain a concern)

- Testing model predictions for disparate impact using adverse impact ratio analysis

- Applying fairness constraints during model training to equalize approval rates

- Conducting periodic bias audits by independent third parties

Some institutions establish AI ethics committees to review high-risk model deployments before launch. Others implement algorithmic impact assessments similar to privacy impact assessments under GDPR.

The Future: LLM-Powered Risk Models

Large language models represent the next frontier. These systems process unstructured text—loan officer notes, borrower correspondence, news articles about employer health—to extract risk signals unavailable in structured databases.

Early applications focus on credit memo analysis, automatically flagging inconsistencies between loan application narratives and supporting documentation. More ambitious implementations generate risk summaries by synthesizing dozens of data sources into coherent assessments.

But LLMs introduce new explainability challenges. When a model bases its risk assessment partly on semantic patterns in borrower emails, translating that into compliant adverse action notices becomes extraordinarily difficult.

Expect regulatory guidance to evolve as these technologies mature. The Bank of France emphasized in February 2025 that trustworthy AI in the financial sector requires robust foundations—transparency, fairness, accountability—before deployment.

Frequently Asked Questions

How accurate are predictive analytics models for loan defaults?

Accuracy varies by model type and data quality. Academic studies show neural networks achieving 95% accuracy with balanced precision and recall, while traditional logistic regression reaches 79% accuracy but identifies only 22% of actual defaulters. XGBoost models hit 86% accuracy with 0.74 ROC-AUC. Real-world performance depends on training data quality, feature engineering, and ongoing model maintenance.

Do lenders have to explain AI credit decisions?

Yes. The Consumer Financial Protection Bureau confirmed in October 2024 that federal anti-discrimination law requires specific explanations for credit denials, with no exception for complex algorithms or black-box models. Lenders must provide accurate reasons reflecting the actual factors that drove the adverse action, not generic form responses.

What alternative data sources improve credit predictions?

Common alternative data includes bank transaction histories showing income stability and spending patterns, utility and rent payment records for credit-invisible consumers, employment verification data revealing job tenure and income growth, and behavioral analytics from application processes. Each source requires careful compliance review to avoid proxy discrimination.

How much does implementing predictive analytics cost?

Implementation costs vary widely based on institution size and system complexity. Financial institutions vary widely in implementation costs based on size and system complexity. Ongoing expenses include model monitoring, periodic retraining, and compliance auditing. ROI comes from reduced charge-offs, lower fraud losses, and operational efficiency gains.

Can predictive models discriminate against protected classes?

Models can perpetuate historical biases if training data reflects discriminatory past practices. Even without explicit protected attributes, proxy variables—ZIP codes, name patterns, shopping behaviors—can create disparate impact. Responsible lenders conduct regular bias audits, test for adverse impact ratios across demographic groups, and apply fairness constraints during model training.

How long does it take to deploy a predictive lending model?

Typical implementations span 12-18 months across four phases: data audit and integration (3-6 months), model training and validation (4-8 months), pilot testing and refinement (2-4 months), then full deployment with ongoing monitoring. Timeframes extend when legacy system integration proves complex or when regulatory validation requirements demand extensive documentation.

What happens when predictive models make mistakes?

Model governance frameworks require continuous monitoring, quarterly performance reviews, and clear escalation procedures. When models systematically underperform—higher-than-expected defaults in a risk tier, disparate impact on protected classes—lenders must investigate root causes, potentially retrain on updated data, or revert to prior decisioning methods. Federal Reserve SR 11-7 guidance mandates documented remediation processes.

Conclusion

Predictive analytics fundamentally reshapes how financial institutions assess credit risk. Neural networks now outperform traditional methods by 20% in default prediction. The Treasury prevented $4 billion in fraud using machine learning in fiscal year 2024 alone.

But performance gains must balance against regulatory requirements and ethical obligations. The CFPB’s guidance makes clear that algorithmic complexity doesn’t exempt lenders from providing specific, accurate explanations for adverse actions.

Institutions that succeed combine advanced models with robust governance—bias testing, model validation, continuous monitoring, and transparent documentation. They treat predictive analytics not as a replacement for human judgment but as a tool that augments it.

The competitive advantage goes to lenders who deploy these systems thoughtfully. Better risk assessment means approving more creditworthy borrowers while reducing losses from defaults and fraud. That’s the promise of predictive analytics in lending—when implemented right.

Ready to modernize credit risk processes? Start with a comprehensive data audit, establish model governance frameworks that meet regulatory standards, and pilot models on historical portfolios before full deployment. The technology works. The question is whether institutions commit the resources and discipline to implement it responsibly.