Quick Summary: Predictive analytics in payment processing uses machine learning and historical transaction data to forecast payment behaviors, detect fraud, optimize approval rates, and reduce processing costs. Financial institutions leverage these models to predict payment success rates, identify high-risk transactions in real-time, and personalize customer payment experiences. As of 2026, this technology has become essential for managing the complexity of digital payments, with the financial sector showing approximately 2.5% to 3% of job listings now requiring AI-related skills.

Payment processing has evolved far beyond simple authorization and settlement. Every transaction now generates data points that, when analyzed properly, reveal patterns about customer behavior, fraud indicators, and operational efficiency.

The financial industry is rapidly integrating artificial intelligence into core operations. According to the Federal Reserve, in the financial sector, 1 in 10 job postings mention AI-related skills, reflecting how deeply these capabilities have become embedded in modern payment infrastructure.

But here’s the thing—predictive analytics isn’t just about having sophisticated algorithms. It’s about extracting actionable intelligence from transaction streams that can prevent losses, improve customer experiences, and optimize working capital.

What Predictive Analytics Means for Payment Processing

Predictive analytics in this context refers to using historical payment data, customer information, and external signals to forecast future payment outcomes. The models answer questions like: Will this transaction complete successfully? Is this payment likely fraudulent? When will a customer actually pay an invoice?

These aren’t theoretical exercises. Payment processors handle billions of transactions, and even small improvements in prediction accuracy translate to massive financial impact.

The technology relies on machine learning models trained on vast datasets. These models identify correlations that humans couldn’t spot manually—connections between transaction timing, merchant categories, geographic patterns, device fingerprints, and payment success rates.

Core Components of Payment Prediction Systems

Modern payment analytics platforms typically combine several data layers:

- Transaction history and patterns for individual customers

- Merchant and industry-specific payment behavior benchmarks

- Device and network metadata for fraud signals

- External data like credit scores, employment verification, and economic indicators

- Real-time behavioral signals during the payment flow

The models process these inputs in milliseconds, generating risk scores and predictions before authorization decisions are made.

Use Predictive Analytics with AI Superior

AI Superior works with transaction and behavioral data to build predictive models for monitoring, risk detection, and operational decisions. The focus is on integrating models into existing systems for continuous use.

Looking to Apply Predictive Analytics in Payment Processing?

AI Superior can help with:

- evaluating transaction data

- building predictive models

- integrating models into existing systems

- improving detection based on results

👉 Contact AI Superior to discuss your project, data, and implementation approach.

Fraud Detection Through Predictive Models

Fraud prevention represents the most mature application of predictive analytics in payments. Financial institutions have been refining these models for years, but recent advances in machine learning have dramatically improved performance.

Traditional rule-based systems flagged transactions based on fixed thresholds—transaction amounts over certain limits, unusual geographic patterns, or merchant category anomalies. These systems generated high false positive rates, blocking legitimate transactions and frustrating customers.

Predictive models take a different approach. They build dynamic profiles of normal behavior for each customer and merchant, then calculate deviation scores for incoming transactions. A purchase that looks suspicious for one customer might be perfectly normal for another.

Real talk: according to Stripe’s analysis, large banks like JPMorgan Chase have used prescriptive analytics in fraud detection models to reduce false positives to 30 percent. That’s not just a technical win; it directly impacts customer satisfaction and revenue.

Real-Time vs. Batch Processing

Payment fraud models operate in two modes. Real-time scoring happens during transaction authorization, requiring sub-second response times. Batch analysis runs periodically on historical data, identifying patterns and refining models.

The real-time constraint is demanding. Models must balance accuracy against speed, sometimes using simplified algorithms that can execute in under 100 milliseconds. More complex ensemble methods run in batch mode, feeding insights back to improve the real-time models.

Payment Authorization Optimization

Beyond fraud, predictive analytics optimizes authorization decisions themselves. The goal: maximize approval rates for legitimate transactions while minimizing risk exposure.

Payment processors face a constant tension. Declining legitimate transactions costs merchants revenue and damages customer relationships. Approving risky transactions leads to chargebacks, fraud losses, and regulatory penalties.

Predictive models help thread this needle by estimating the true probability that a transaction will complete successfully and that the customer will not dispute it. These probability scores inform smarter authorization rules.

Now, this is where it gets interesting. Some payment platforms use predictive analytics to route transactions through different payment networks or authentication methods based on success probability. If a transaction has a high predicted failure rate through one card network, the system might attempt an alternative payment method or trigger step-up authentication.

| Authorization Strategy | Traditional Rule-Based | Predictive Analytics |

|---|---|---|

| Decision Logic | Fixed thresholds and rules | Dynamic probability scoring |

| Customer Context | Limited (basic segmentation) | Individual behavior profiles |

| Adaptation Speed | Manual rule updates | Continuous automated learning |

| False Decline Rate | Higher (3-5% typical) | Lower (2-3% achievable) |

| Fraud Loss Rate | Varies widely | Reduced 20-30% reported |

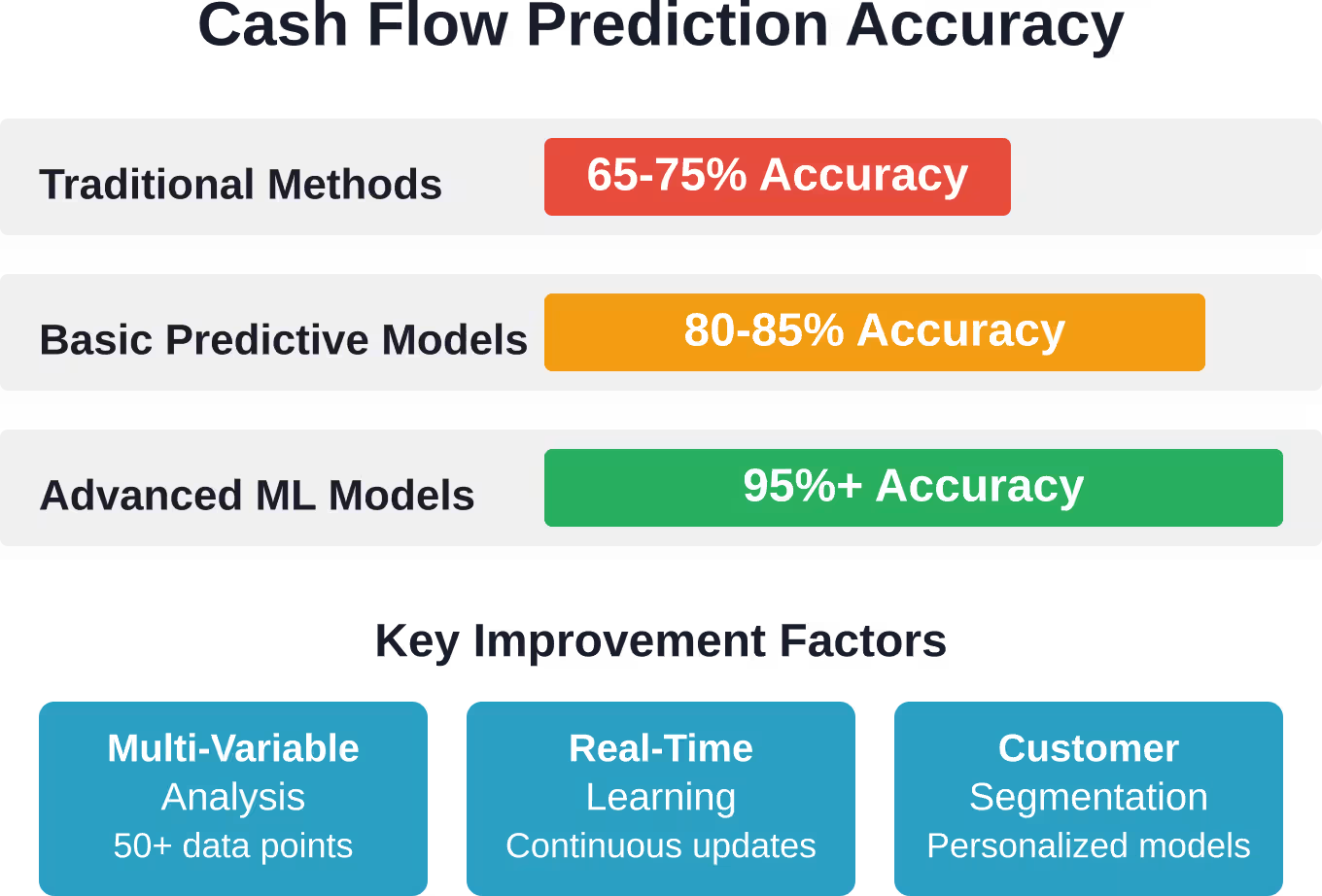

Cash Flow Forecasting for Merchants

For businesses that process payments—especially those dealing with invoices and delayed settlements—predictive analytics transforms cash flow management.

Traditional cash flow forecasting relied on simple aging reports and historical averages. Predictive models incorporate dozens of variables: customer payment history, invoice characteristics, industry benchmarks, seasonal patterns, economic conditions, and even individual customer financial health signals.

The result is significantly more accurate forecasting. Analysis of accounts receivable predictive analytics shows that companies can fine-tune payment cycles to cut delays and interruptions by analyzing when and how customers pay outstanding invoices.

Propensity-to-Pay Modeling

One specific application is propensity-to-pay scoring—predicting which customers are likely to pay invoices on time, which will pay late, and which represent collection risks.

These scores inform multiple operational decisions:

- Credit limit adjustments for individual customers

- Early intervention strategies for at-risk accounts

- Optimal timing for payment reminders and collection outreach

- Resource allocation for collection teams

- Pricing adjustments to account for payment risk

Some organizations achieve forecast accuracy thresholds of 95 percent or higher using sophisticated predictive models, with many areas realizing 98 percent or greater accuracy. One company forecasts 70,000 different data points monthly using data science models with a 95% accuracy threshold and realizes 98% or greater in many areas. This level of precision enables much tighter working capital management.

Processing Cost Reduction

Payment processing carries direct costs—network fees, gateway charges, fraud losses, chargeback penalties. Predictive analytics identifies opportunities to reduce these expenses.

One approach: intelligent routing. By predicting which payment method or processor will have the highest success rate and lowest cost for a given transaction, systems can route dynamically. A transaction might go through a lower-cost network if it has high predicted success probability, while riskier transactions use more robust (but expensive) authentication flows.

Chargeback prediction represents another cost-saving application. Models identify transactions with elevated dispute risk before they’re approved, allowing merchants to take preventive action—additional verification, proactive customer service outreach, or enhanced documentation.

Customer Experience Personalization

Predictive analytics enables payment experiences tailored to individual customer risk profiles and preferences.

Low-risk customers with strong payment histories get frictionless checkout—saved payment methods, one-click purchasing, minimal authentication challenges. Higher-risk transactions or new customers encounter additional verification steps, but only when genuinely warranted by the data.

This risk-based authentication balances security and convenience. Instead of applying uniform friction to all transactions, the system adapts to each situation.

Payment timing optimization also improves customer experience. By predicting when individual customers are most likely to complete payments—based on historical patterns, income cycles, and behavioral signals—systems can time invoice delivery and payment reminders for maximum effectiveness.

Building Effective Prediction Models

Implementing predictive analytics for payment processing isn’t plug-and-play. It requires thoughtful data architecture, model selection, and ongoing refinement.

Data Foundation Requirements

Quality predictions require quality data. The essential inputs include:

- Complete transaction history with outcomes (approved, declined, fraud, chargeback)

- Customer demographic and account information

- Device and session metadata

- Merchant and product category details

- Temporal features (time of day, day of week, seasonality)

- External data sources (credit bureaus, fraud networks, economic indicators)

Data quality matters more than quantity. Incomplete records, inconsistent labeling, and outdated information degrade model performance. Many organizations spend more time on data cleaning and feature engineering than on actual model training.

Model Selection and Validation

Different payment use cases require different modeling approaches. Fraud detection often uses ensemble methods combining multiple algorithms—decision trees, neural networks, and anomaly detection techniques—to catch diverse fraud patterns.

Cash flow forecasting might use time series models or regression techniques. Authorization optimization could employ classification models that output probability scores.

But here’s what really matters: rigorous validation. Models must be tested on held-out data that wasn’t used in training, mimicking real-world deployment conditions. Performance metrics need to align with business objectives—not just overall accuracy, but false positive rates, false negative rates, and the financial impact of each error type.

Regulatory and Compliance Considerations

Payment processing operates under strict regulatory oversight. Predictive analytics implementations must navigate complex compliance requirements.

Data privacy regulations like GDPR and CCPA impose constraints on what customer data can be collected, how it’s used, and how long it’s retained. Payment systems must implement proper consent mechanisms, data minimization practices, and customer rights to access and deletion.

Fair lending and anti-discrimination laws present another challenge. Predictive models cannot discriminate based on protected characteristics like race, gender, or age. Even when these attributes aren’t explicitly included in models, they can be proxied by other variables (neighborhood, name patterns, spending categories).

Financial institutions must conduct regular bias audits of their models, testing for disparate impact across demographic groups. Some jurisdictions require explainability—the ability to provide human-understandable reasons for automated decisions.

Model Governance Frameworks

Sound governance practices for payment prediction models include:

- Documentation of model development methodology and validation results

- Regular performance monitoring and revalidation schedules

- Change management processes for model updates

- Clear accountability and oversight structures

- Procedures for handling model failures or unexpected behavior

- Audit trails for automated decisions

Regulatory guidance is evolving rapidly. The Federal Reserve and other financial regulators have increased focus on artificial intelligence risk management, as evidenced by recent testimony on innovation and supervision frameworks.

Infrastructure and Technology Stack

Deploying production-grade predictive analytics for payment processing requires robust technical infrastructure.

Real-Time Processing Requirements

Payment authorization decisions happen in milliseconds. The entire chain—data collection, feature computation, model inference, and response—must complete within strict latency budgets, typically under 100-200 milliseconds.

This demands high-performance computing infrastructure, optimized model architectures, and careful engineering. Many organizations use specialized frameworks for low-latency machine learning inference, GPU acceleration for complex models, and extensive caching to avoid repeated calculations.

Scalability Considerations

Payment volumes fluctuate dramatically—seasonal peaks, promotional events, geographic patterns. Infrastructure must scale elastically to handle volume spikes without degrading latency or accuracy.

Cloud platforms offer advantages here, allowing organizations to provision computing resources dynamically. But cloud deployment introduces its own complexities around data residency, network latency, and cost management.

as organizations build capacity for these applications.

Emerging Trends and Future Directions

Predictive analytics in payment processing continues to evolve rapidly. Several trends are shaping the next generation of capabilities.

Graph-Based Fraud Detection

Traditional models analyze transactions in isolation. Graph-based approaches examine the network of relationships between customers, devices, merchants, and accounts. Fraud rings and organized schemes create detectable patterns in these networks that aren’t visible in individual transaction analysis.

These methods can identify subtle connections—shared devices across supposedly unrelated accounts, velocity patterns across linked entities, and coordinated attack patterns.

Federated Learning for Privacy

Federated learning allows multiple organizations to collaboratively train models without sharing raw customer data. Models learn from distributed datasets while keeping sensitive information local.

This approach could enable payment networks to build better fraud models by learning from patterns across many financial institutions while maintaining strict data privacy boundaries.

Explainable AI Implementations

As regulatory scrutiny increases, demand grows for models that can explain their predictions in human-understandable terms. Newer techniques provide explanations alongside predictions—identifying which specific factors contributed most to a particular decision.

These explanations serve multiple purposes: regulatory compliance, customer service (explaining why a transaction was declined), and model debugging (identifying unexpected behavior).

Implementation Challenges and Solutions

Organizations attempting to deploy predictive analytics for payments encounter common obstacles.

Data Silos and Integration

Payment data often lives in multiple disconnected systems—transaction processors, fraud platforms, customer databases, accounting systems. Creating unified datasets for model training requires extensive integration work.

Many organizations invest in data lakes or warehouses specifically to consolidate payment-related information. ETL (extract, transform, load) pipelines pull data from source systems, standardize formats, and make it available for analytics.

Model Maintenance Burden

Payment patterns shift constantly. New fraud techniques emerge, customer behaviors evolve, and market conditions change. Models trained on historical data gradually lose accuracy as the world changes around them—a phenomenon called model drift.

Successful implementations include automated monitoring for drift, scheduled retraining cycles, and processes for rapid model updates when performance degrades. Some organizations retrain critical models weekly or even daily to stay current.

Skills and Talent Gaps

Building effective payment prediction systems requires hybrid expertise—understanding both payment operations and data science. These skills rarely exist in single individuals, requiring cross-functional teams.

The financial sector has recognized this need, reflected in the fact that 10 percent of job listings in the industry now mention AI-related skills according to Federal Reserve analysis. Organizations are investing heavily in hiring and training to build these capabilities internally.

Measuring Success and ROI

Predictive analytics initiatives must demonstrate business value. Common metrics for payment processing applications include:

| Metric Category | Specific Measurements | Target Improvements |

|---|---|---|

| Fraud Prevention | Fraud detection rate, false positive rate, fraud loss ratio | 20-30% reduction in losses, 30%+ reduction in false positives |

| Authorization | Approval rate, false decline rate, customer authentication friction | 2-5% improvement in approval rates |

| Cash Flow | Forecast accuracy (MAPE), days sales outstanding, collection efficiency | 95%+ forecast accuracy, 5-10% DSO reduction |

| Operations | Processing costs, manual review volume, chargeback rate | 15-25% cost reduction, 40%+ reduction in manual reviews |

Financial impact calculations should account for both direct benefits (reduced fraud losses, lower processing fees) and indirect gains (improved customer satisfaction, reduced customer service costs, better working capital efficiency).

Frequently Asked Questions

How accurate are predictive analytics models for payment fraud detection?

Accuracy varies based on implementation quality, data availability, and fraud sophistication. Well-designed systems achieve fraud detection rates above 90 percent while maintaining false positive rates below 1-2 percent. Major banks using advanced analytics have reported reducing false positives by up to 30 percent compared to traditional rule-based systems. Accuracy improves continuously as models learn from new fraud patterns and legitimate transaction behaviors.

What data is required to implement payment prediction models?

Core requirements include complete transaction history with outcomes (approved, declined, fraudulent, chargeback), customer account and demographic information, payment method details, and device/session metadata. Enhanced models incorporate merchant category data, geographic information, temporal features, and external signals like credit scores or fraud network intelligence. Data quality and completeness matter more than volume—clean, well-labeled datasets of moderate size outperform large but messy datasets.

Can small businesses benefit from predictive analytics in payment processing?

Yes, though implementation approaches differ. Small businesses typically leverage predictive capabilities built into their payment platforms rather than developing custom models. Modern payment processors and fintech platforms increasingly embed analytics into their offerings, providing fraud scoring, authorization optimization, and cash flow forecasting as platform features. These turnkey solutions make advanced analytics accessible without requiring in-house data science teams.

How do predictive models handle new types of fraud or payment patterns?

Models use several approaches to adapt to novel patterns. Continuous learning systems retrain regularly on recent data, incorporating new fraud techniques as they’re identified. Anomaly detection components flag unusual patterns that don’t match historical behaviors, catching zero-day fraud attempts. Ensemble methods combine multiple model types, increasing the likelihood that at least one component will detect new attack vectors. Organizations also maintain rapid-response processes to update models when security teams identify emerging threats.

What are the privacy implications of payment prediction analytics?

Payment prediction requires processing sensitive financial and personal data, raising legitimate privacy concerns. Implementations must comply with regulations like GDPR, CCPA, and PCI-DSS, which mandate data minimization, purpose limitation, and customer consent. Best practices include encrypting data at rest and in transit, limiting access to authorized systems and personnel, implementing retention policies that delete data when no longer needed, and providing customers transparency about how their data is used. Some newer approaches like federated learning enable model training without centralizing raw customer data.

How long does it take to implement predictive analytics for payment processing?

Timeline varies dramatically based on scope and organizational readiness. Enabling embedded analytics in existing payment platforms might take weeks to configure and validate. Building custom models from scratch typically requires 3-6 months for initial deployment—data collection and preparation, model development and testing, integration with payment systems, and validation. Production-ready systems with full monitoring and governance often need 6-12 months. Organizations with mature data infrastructure and existing analytics capabilities move faster than those starting from scratch.

What’s the difference between predictive and prescriptive analytics in payments?

Predictive analytics forecasts what is likely to happen—will this transaction be fraudulent, will this customer pay on time, what’s the probability of authorization success. Prescriptive analytics recommends what action to take—which payment method to use, when to send payment reminders, how to route transactions for optimal cost and success rates. Predictive models generate probabilities and forecasts; prescriptive systems use those predictions plus business rules and optimization algorithms to recommend specific decisions. Most payment applications use both: predictions inform the prescriptive decision engine.

Conclusion

Predictive analytics has transformed payment processing from reactive transaction handling to proactive risk management and optimization. The technology delivers measurable improvements in fraud prevention, authorization rates, cash flow forecasting, and operational efficiency.

Success requires more than deploying algorithms. Organizations need quality data infrastructure, rigorous model validation, continuous monitoring and maintenance, regulatory compliance frameworks, and cross-functional teams combining payment expertise with data science capabilities.

The trend is clear—as the financial sector continues integrating AI capabilities, with 10 percent of job listings now requiring AI-related skills, predictive analytics is becoming table stakes rather than competitive advantage. Organizations that haven’t begun building these capabilities risk falling behind as customer expectations and competitive pressures intensify.

Whether you’re evaluating payment platforms, building internal capabilities, or optimizing existing implementations, focus on business outcomes rather than technical sophistication. The best models aren’t necessarily the most complex—they’re the ones that reliably improve the metrics that matter to your operations, your customers, and your bottom line.