Résumé rapide : L'apprentissage automatique révolutionne la détection des fraudes en analysant en temps réel d'immenses ensembles de données transactionnelles et en identifiant des schémas complexes que les systèmes traditionnels basés sur des règles ne repèrent pas. Des algorithmes avancés, tels que les réseaux neuronaux, les arbres de décision et les méthodes d'ensemble, s'adaptent en permanence à l'évolution des tactiques de fraude, réduisant ainsi les faux positifs tout en détectant les menaces sophistiquées. Les institutions financières, les plateformes de commerce électronique et les processeurs de paiement s'appuient de plus en plus sur des systèmes pilotés par l'apprentissage automatique qui concilient sécurité et expérience client, atteignant des taux de précision de détection bien supérieurs aux approches traditionnelles.

Les pertes financières mondiales dues à la fraude aux paiements ont atteint des niveaux vertigineux ces dernières années, les fraudeurs faisant constamment évoluer leurs tactiques. Les systèmes de détection traditionnels, basés sur des règles, ne peuvent plus suivre le rythme.

L'apprentissage automatique change complètement la donne. En traitant des volumes de transactions massifs et en repérant des schémas imperceptibles pour l'humain, les algorithmes d'apprentissage automatique sont devenus la première ligne de défense contre la criminalité financière.

Mais voilà le hic : l’application du machine learning à la détection des fraudes ne se résume pas à appliquer des algorithmes à des données. Elle exige de comprendre quelles techniques sont les plus efficaces, comment gérer les ensembles de données déséquilibrés et quand la supervision humaine reste indispensable.

Ce guide détaille tout, des concepts fondamentaux aux stratégies de mise en œuvre avancées, que les institutions financières, les plateformes de commerce électronique et les processeurs de paiement utilisent actuellement.

Pourquoi l'apprentissage automatique est-il essentiel à la détection des fraudes ?

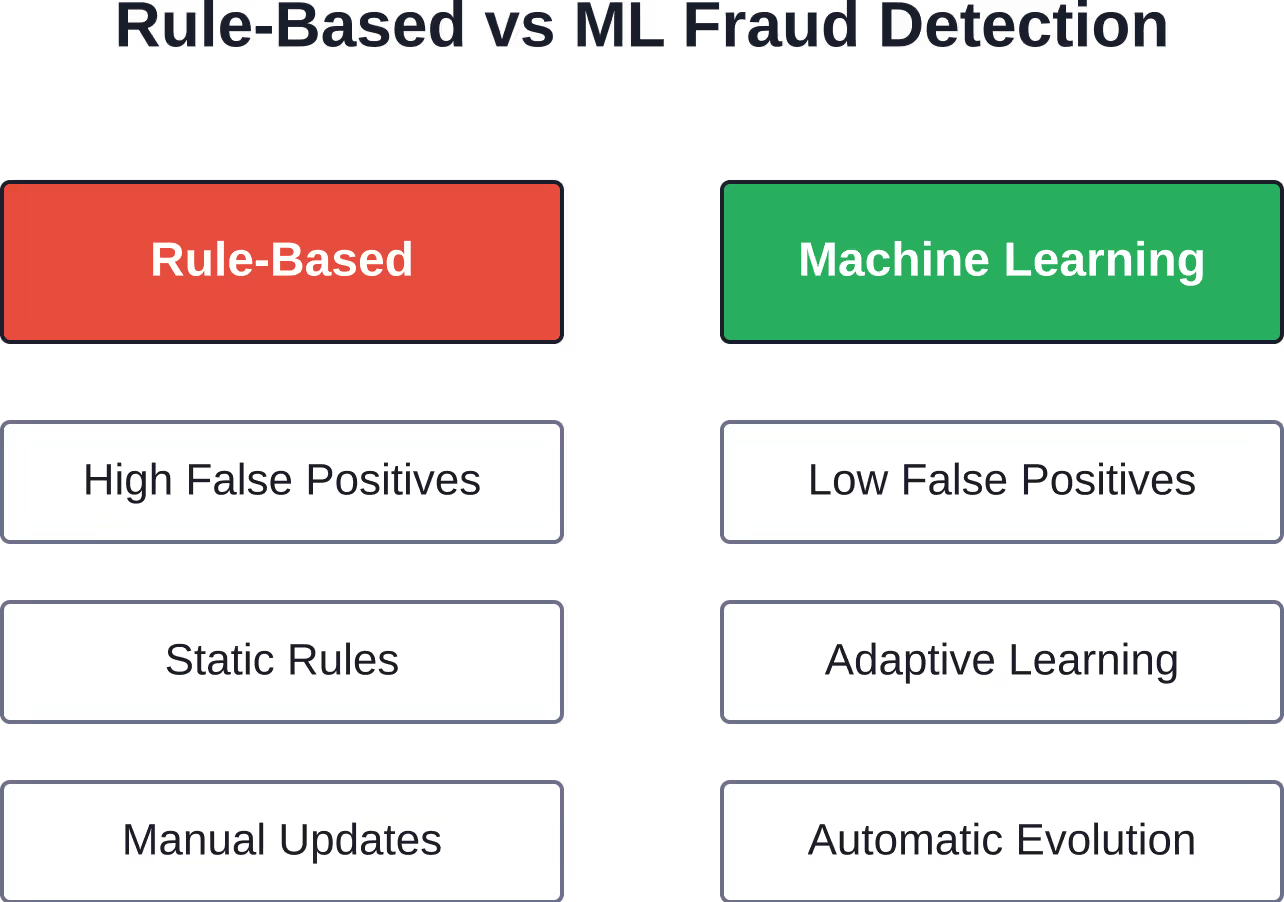

Les systèmes de détection de fraude basés sur des règles fonctionnent selon des conditions prédéterminées. Si une transaction dépasse 100 USD et provient d'une zone à haut risque, elle est bloquée. Simple, non ?

Trop simpliste. Ces règles rigides génèrent un nombre alarmant de faux positifs. Un achat d'un montant inhabituellement élevé déclenche des alertes même lorsque la transaction est légitime, ce qui engendre des frictions et des pertes de revenus.

Les algorithmes d'apprentissage automatique analysent simultanément des centaines de variables : montant de la transaction, lieu, heure, empreinte digitale de l'appareil, historique des achats, habitudes comportementales. Ils identifient des corrélations subtiles que les règles statiques ne détectent absolument pas.

D'après une étude, les méthodes traditionnelles de détection des fraudes peinent à suivre l'évolution des stratégies frauduleuses, contribuant ainsi à une perte financière mondiale estimée à environ 1 450 milliards de dollars. Il ne s'agit pas d'une erreur : cinq mille milliards de dollars.

Les modèles d'apprentissage automatique s'adaptent. À mesure que les fraudeurs modifient leurs tactiques, les algorithmes apprennent de nouveaux schémas sans reprogrammation manuelle. Cette adaptation dynamique les rend fondamentalement supérieurs aux systèmes traditionnels.

L'avantage de l'échelle

Les institutions financières traitent quotidiennement des millions de transactions. Les algorithmes d'apprentissage automatique analysent chacune d'elles en quelques millisecondes, établissant ainsi des profils comportementaux pour l'ensemble de leurs clients.

Les analystes humains ne pourraient jamais atteindre une telle échelle. Même les grandes équipes de lutte contre la fraude chargées d'examiner les transactions signalées adoptent une approche réactive : elles détectent la fraude une fois les schémas apparus, au lieu de la prévenir en temps réel.

Les recherches d'IBM sur la détection de la fraude par l'IA dans le secteur bancaire mettent en lumière comment les algorithmes d'apprentissage automatique analysent de vastes ensembles de données pour identifier des schémas qu'il serait impossible pour des équipes humaines de détecter manuellement.

Techniques fondamentales d'apprentissage automatique pour la détection de la fraude

Les différentes approches d'apprentissage automatique permettent de résoudre différents problèmes de détection de la fraude. Savoir quand privilégier l'apprentissage supervisé plutôt que non supervisé est essentiel pour une mise en œuvre efficace.

Modèles d'apprentissage supervisé

L'apprentissage supervisé s'appuie sur des ensembles de données étiquetées — des transactions déjà marquées comme frauduleuses ou légitimes. L'algorithme apprend les caractéristiques distinctives et les applique aux nouvelles transactions.

Les techniques supervisées courantes comprennent :

- Régression logistique : Simple mais efficace pour la classification binaire (fraude/non-fraude), notamment lorsque l'interprétabilité est importante pour la conformité réglementaire.

- Arbres de décision : Créer des chemins basés sur des règles à travers de multiples variables, faciles à expliquer aux parties prenantes non techniques

- Forêts aléatoires : Méthode d'ensemble combinant plusieurs arbres de décision, réduisant le surapprentissage et améliorant la précision

- Réseaux neuronaux : Modèles d'apprentissage profond qui identifient des schémas non linéaires complexes dans des données de grande dimension

- Boost de gradient : Technique d'ensemble séquentielle qui corrige les erreurs des modèles précédents, atteignant souvent les taux de précision les plus élevés.

Une étude publiée par l'Université Georgia Southern démontre comment les réseaux neuronaux profonds détectent la fraude dans les transactions financières, en particulier pour les schémas qui changent constamment.

Le problème ? L’apprentissage supervisé nécessite un volume important de données d’entraînement étiquetées. Or, pour les nouvelles formes de fraude, ces données historiques n’existent pas encore.

Approches d'apprentissage non supervisé

Les algorithmes non supervisés n'ont pas besoin de données étiquetées. Ils identifient plutôt les anomalies, c'est-à-dire les transactions qui s'écartent significativement des schémas normaux.

Principales techniques non supervisées :

- Clustering (K-means, DBSCAN) : Regroupe les transactions similaires, en signalant les valeurs aberrantes qui ne correspondent à aucun groupe.

- Forêts d'isolement : Spécialement conçu pour la détection d'anomalies, l'isolement des points de données inhabituels

- Autoencodeurs : Des réseaux neuronaux qui apprennent à reconstituer les transactions normales, mais qui ont du mal avec les transactions frauduleuses.

L'apprentissage non supervisé excelle dans la détection de nouvelles techniques de fraude. Lorsque les fraudeurs inventent des tactiques entièrement inédites, ces algorithmes repèrent les activités suspectes sans aucun exemple préalable.

Le compromis ? Un taux de faux positifs plus élevé qu’avec les méthodes supervisées. Inhabituel ne signifie pas forcément frauduleux, simplement différent.

Méthodes hybrides et semi-supervisées

De nombreux systèmes de production combinent différentes approches. L'apprentissage semi-supervisé utilise de petites quantités de données étiquetées et de grands volumes de transactions non étiquetées, tirant ainsi profit des deux paradigmes.

Les réseaux neuronaux graphiques constituent une autre technique avancée. Ils analysent les relations entre les entités, non seulement les transactions individuelles, mais aussi les réseaux de comptes, d'appareils et de commerçants connectés. Cela permet de déceler les réseaux de fraude coordonnés que l'analyse des transactions individuelles ne permet pas de détecter.

| Technique | Idéal pour | Exigences en matière de données | Taux de faux positifs |

|---|---|---|---|

| Apprentissage supervisé | Schémas de fraude connus | Grands ensembles de données étiquetées | Faible |

| Apprentissage non supervisé | Détection de fraude novatrice | Aucune étiquette nécessaire | Modéré à élevé |

| Réseaux neuronaux | Motifs complexes | Ensembles de données très volumineux | Faible (lorsqu'il est bien entraîné) |

| Méthodes d'ensemble | Maximiser la précision | Grands ensembles de données étiquetées | Très faible |

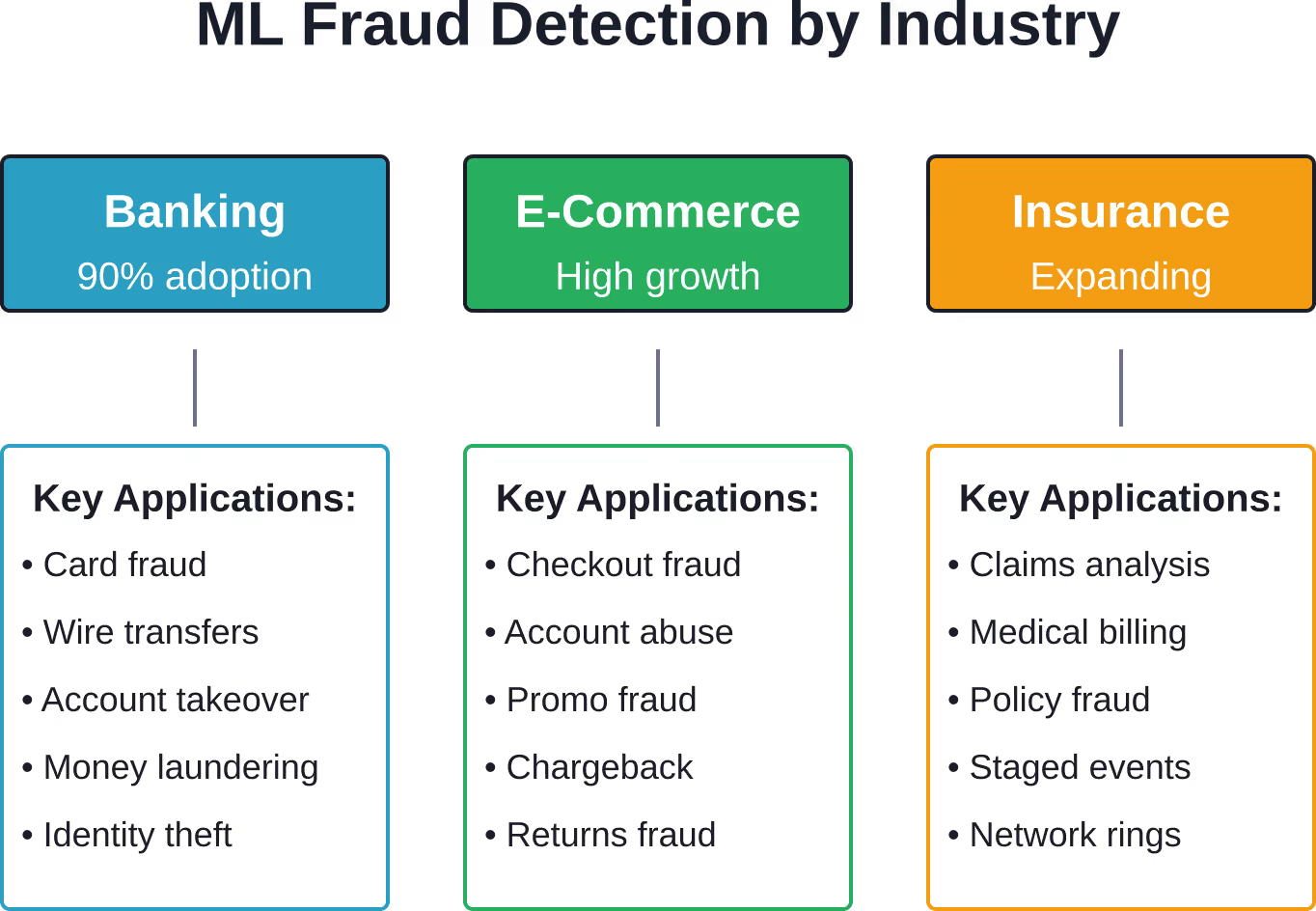

Applications concrètes dans tous les secteurs d'activité

La détection de la fraude par apprentissage automatique ne se limite pas à un seul secteur. Différents secteurs d'activité sont confrontés à des défis uniques en matière de fraude, que l'apprentissage automatique permet de relever de manière spécialisée.

Services bancaires et financiers

Les banques déploient l'apprentissage automatique simultanément sur de multiples vecteurs de fraude. La détection de la fraude à la carte de crédit reste l'application la plus visible : elle permet de signaler les achats suspects avant leur validation.

Mais ML surveille également :

- Tentatives de prise de contrôle de compte (schémas de connexion inhabituels, changements d'appareil)

- Fraude par virement bancaire (analyse du compte destinataire, anomalies de montant)

- Réseaux de blanchiment d'argent (chaînes de transactions, schémas de structuration)

- Vol d'identité lors de l'ouverture d'un compte (vérification de documents, biométrie comportementale)

Selon le rapport 2025 de Feedzai sur les tendances de l'IA en matière de fraude et de criminalité financière, 901 000 000 institutions financières utilisent déjà l'IA et l'apprentissage automatique pour la prévention de la fraude.

Les normes NIST spécifient les exigences techniques en matière de vérification d'identité et d'authentification numérique, mais les seuils spécifiques de taux de faux positifs biométriques doivent être vérifiés dans la documentation complète NIST SP 800-63.

Commerce électronique et vente au détail

Les commerçants en ligne sont confrontés à des défis différents de ceux des banques. Ils doivent détecter les fraudes sans créer de frictions lors du paiement qui fassent fuir les clients.

Les modèles d'apprentissage automatique pour le commerce électronique analysent :

- Vitesse d'achat (commandes multiples dans des délais très courts)

- Empreinte digitale de l'appareil (configuration du navigateur, cohérence de l'adresse IP)

- Analyse des adresses de livraison (transitaires, boîtes postales, incohérences avec la facturation)

- Signaux comportementaux (mouvements de la souris, schémas de frappe, durée de la session)

L’objectif n’est pas seulement de bloquer la fraude, mais d’approuver un maximum de transactions légitimes tout en minimisant les rétrofacturations.

Traitement des demandes d'indemnisation

La fraude à l'assurance coûte chaque année des milliards au secteur. Les algorithmes d'apprentissage automatique évaluent les demandes d'indemnisation afin de détecter des schémas suspects tels que :

- Délai de déclaration de sinistre (immédiatement après la prise d'effet de la police)

- Schémas historiques (réclamations multiples de parties liées)

- Détails de la réclamation (descriptions d'accidents correspondant à des modèles de fraude connus)

- Anomalies de facturation médicale (interventions inutiles, coûts gonflés)

Ces systèmes privilégient l'examen des demandes par les enquêteurs plutôt que de les rejeter automatiquement, ce qui permet d'équilibrer la prévention de la fraude et le traitement légitime des demandes.

Appliquer l'apprentissage automatique à la détection des fraudes grâce à l'IA supérieure

La détection des fraudes nécessite souvent l'analyse en temps réel de volumes importants de transactions, de signaux comportementaux et de données opérationnelles. IA supérieure peut aider les organisations à développer des systèmes d'apprentissage automatique capables d'identifier plus efficacement les activités suspectes, les schémas inhabituels ou les risques potentiels.

AI Superior peut soutenir les projets de détection de la fraude grâce à :

- Analyse des ensembles de données transactionnelles et comportementales

- Définition des cas d'utilisation et des scénarios de risque en matière de détection des fraudes

- Construction de modèles de validation de concept

- Développement de systèmes de détection ou de classification des anomalies

- Fiabilité du modèle et taux de faux positifs

- Intégration de la planification aux systèmes de surveillance des fraudes existants

- Soutien au déploiement dans les flux de travail opérationnels

En matière de détection des fraudes, cela peut s'appliquer à la fraude aux paiements, à la détection des abus de comptes, à la surveillance des transactions, à l'analyse des fraudes à l'assurance, à la vérification d'identité et à l'analyse des risques financiers.

Parlez à un supérieur de l'IA à propos du processus de détection des fraudes.

Défis critiques liés à la détection de la fraude par apprentissage automatique

La mise en œuvre de l'apprentissage automatique pour la détection des fraudes n'est pas simple. Plusieurs obstacles surgissent systématiquement lors des déploiements.

Ensembles de données déséquilibrés

Voici le problème : les transactions frauduleuses représentent une infime fraction du volume total, souvent moins de 11 TP3T. Lorsque les données d’entraînement contiennent 99,51 TP3T de transactions légitimes et 0,51 TP3T de transactions frauduleuses, les modèles d’apprentissage automatique ont tendance à optimiser les performances pour la classe majoritaire.

L'algorithme apprend à tout étiqueter comme légitime et atteint tout de même une précision de 99,51 % (TP3T). Inutile.

Les solutions comprennent :

- Cas de fraude par suréchantillonnage (technique de suréchantillonnage de la minorité synthétique – SMOTE)

- Sous-échantillonnage des transactions légitimes

- Ajustement des pondérations de classe dans la fonction de perte

- Utiliser des indicateurs d'évaluation autres que l'exactitude (précision, rappel, score F1)

L'approche appropriée dépend des priorités de l'entreprise. Le secteur bancaire privilégie généralement la détection des fraudes (accepter un plus grand nombre de faux positifs), tandis que le commerce électronique optimise la précision (minimiser les obstacles pour le client).

Explicabilité du modèle et conformité réglementaire

Les autorités de régulation financière exigent de plus en plus d'explications concernant les décisions automatisées. Lorsqu'un modèle d'apprentissage automatique refuse une transaction, l'établissement doit en justifier les raisons.

Les réseaux neuronaux profonds fonctionnent comme des boîtes noires. Ils atteignent une grande précision, mais ne fournissent pas de raisonnement interprétable par l'humain. Cela engendre un risque réglementaire.

La Commission fédérale du commerce (FTC) a annoncé l'opération AI Comply en septembre 2024, visant à lutter contre les allégations trompeuses concernant l'intelligence artificielle. Les entreprises doivent prouver que leurs systèmes de détection de fraude fonctionnent comme annoncé et respectent la législation sur la protection des consommateurs.

Certaines institutions privilégient les modèles interprétables comme les arbres de décision ou la régression logistique, malgré une précision légèrement inférieure. D'autres utilisent des techniques d'explication a posteriori comme SHAP (SHapley Additive exPlanations) ou LIME (Local Interpretable Model-agnostic Explanations) pour interpréter les modèles complexes.

Adversaires adaptatifs

Les fraudeurs ne sont pas statiques. Ils testent constamment les défenses, apprenant quels comportements déclenchent des blocages et lesquels parviennent à les contourner.

Cela engendre une course aux armements. Les modèles d'apprentissage automatique doivent être régulièrement réentraînés sur des données actualisées, intégrant les nouveaux schémas de fraude dès leur apparition. La fréquence de réentraînement varie : certains systèmes sont mis à jour quotidiennement, d'autres hebdomadairement ou mensuellement.

Les discussions entre professionnels de la prévention de la fraude mettent régulièrement en lumière ce problème. Les réseaux de fraude partagent des informations sur les tactiques qui fonctionnent actuellement contre certains commerçants ou banques.

Confidentialité et sécurité des données

La mise au point de modèles efficaces de détection des fraudes nécessite l'accès à des données transactionnelles détaillées, aux informations clients et aux schémas comportementaux. Cela soulève des questions de confidentialité.

Des réglementations comme le RGPD et le CCPA encadrent la collecte, le stockage et le traitement des données personnelles par les organisations. Les solutions d'apprentissage automatique doivent s'y conformer tout en préservant leur efficacité.

L'apprentissage fédéré offre une solution : l'entraînement de modèles sur des ensembles de données distribués sans centralisation des informations sensibles. Chaque institution effectue l'entraînement localement et ne partage que les mises à jour des modèles, et non les données brutes.

Meilleures pratiques de mise en œuvre

Les organisations qui déploient des systèmes de détection de fraude par apprentissage automatique devraient suivre ces approches éprouvées pour maximiser leurs chances de succès.

Commencez par les indicateurs de performance de l'entreprise

Les indicateurs techniques, comme la précision du modèle, ne se traduisent pas directement en valeur commerciale. Définissez ce qui compte vraiment :

- Pourcentage de fraudes détectées parmi les tentatives de fraude (taux de détection)

- Taux de faux positifs et coûts de friction client associés

- Volume de révision manuelle (heures d'analyse requises)

- Revenus perdus en raison de transactions légitimes bloquées

- Délai moyen de détection de la fraude (latence de détection)

Optimisez les modèles en fonction de ces résultats commerciaux, et non de mesures techniques abstraites.

Créer des pipelines de données robustes

Les modèles d'apprentissage automatique sont aussi performants que leurs données d'entraînement. Investissez massivement dans :

- Validation de la qualité des données (détection et correction des erreurs)

- Ingénierie des caractéristiques (création de variables significatives à partir de données brutes)

- Infrastructure de données en temps réel (scoring à faible latence)

- Précision de l'étiquetage (identification correcte des fraudes dans les ensembles d'entraînement)

Les recherches montrent que la qualité des données compte souvent plus que le choix de l'algorithme. Un modèle simple appliqué à des données propres et pertinentes surpasse un modèle sophistiqué appliqué à des données bruitées et mal organisées.

Combiner l'apprentissage automatique et l'expertise humaine

La détection de fraude entièrement automatisée semble efficace, mais elle fonctionne rarement de manière optimale. Les meilleurs systèmes combinent l'apprentissage automatique et le jugement humain.

Les algorithmes d'apprentissage automatique gèrent le filtrage à haut volume et en temps réel. Ils évaluent chaque transaction et l'approuvent ou la refusent automatiquement en fonction de seuils de risque.

Des analystes humains examinent les cas limites, c'est-à-dire les transactions qui se situent dans la zone d'incertitude. Ils fournissent également des commentaires qui améliorent l'entraînement du modèle, corrigeant les faux positifs et confirmant les fraudes avérées.

Cette approche hybride tire parti des atouts de chaque composante. Les machines assurent l'échelle et la rapidité du traitement. Les humains apportent leur compréhension du contexte et leur capacité d'adaptation aux situations inédites.

Mettre en œuvre une surveillance continue

Les modèles d'apprentissage automatique se dégradent avec le temps, à mesure que les schémas de fraude évoluent. Le suivi des performances des modèles doit prendre en compte :

- Précision des prédictions sur les transactions récentes

- Taux de faux positifs et de faux négatifs par type de fraude

- Évolution de l'importance des caractéristiques (quelles variables sont les plus importantes)

- Dérive des données (propriétés statistiques du décalage des données entrantes)

En cas de baisse de performance, déclenchez un réentraînement du modèle ou une mise à jour des fonctionnalités. Certaines équipes utilisent des pipelines de réentraînement automatiques ; d’autres procèdent à une vérification manuelle avant le déploiement des modèles mis à jour.

Technologies émergentes et orientations futures

La détection de la fraude par apprentissage automatique continue d'évoluer rapidement. Plusieurs technologies émergentes sont très prometteuses.

Réseaux neuronaux graphiques

L'apprentissage automatique traditionnel analyse les transactions individuelles de manière isolée. Les réseaux neuronaux graphiques, quant à eux, examinent les relations — les connexions entre les comptes, les commerçants, les appareils et les emplacements géographiques.

Cette analyse de réseau permet de déceler les réseaux de fraude coordonnés. Lorsque plusieurs comptes apparemment sans lien partagent des empreintes digitales d'appareils, des adresses IP ou des schémas de transactions, les GNN identifient les connexions qui indiquent une fraude organisée.

Les institutions financières utilisent de plus en plus des modèles graphiques pour la détection du blanchiment d'argent, où les chaînes de transactions impliquant de multiples intermédiaires masquent l'origine des fonds.

Apprentissage fédéré

Traditionnellement, les banques et les commerçants ne peuvent pas partager les données relatives à la fraude en raison de problèmes de concurrence et de réglementations sur la protection de la vie privée. L'apprentissage fédéré permet un entraînement collaboratif des modèles sans partage de données.

Chaque établissement effectue l'entraînement localement sur ses propres données. Seules les mises à jour du modèle — les ajustements mathématiques des pondérations — sont partagées avec un coordinateur central. Ce dernier intègre ces mises à jour dans un modèle global amélioré sans jamais avoir accès aux données transactionnelles brutes.

Cette approche permet à l'industrie de lutter collectivement contre la fraude tout en préservant les informations concurrentielles et la confidentialité des données clients.

Techniques d'IA explicables

Face à la demande croissante de transparence des autorités de réglementation, les méthodes d'IA explicables prennent de l'importance. Ces techniques génèrent des explications compréhensibles par l'humain pour les prédictions de l'apprentissage automatique.

Les valeurs SHAP quantifient la contribution de chaque caractéristique à une prédiction spécifique. LIME approxime localement les modèles complexes par des modèles interprétables. Les mécanismes d'attention dans les réseaux neuronaux mettent en évidence les éléments de données qui ont influencé les décisions.

Les futurs systèmes de détection des fraudes intégreront l'explicabilité dès leur conception plutôt que de l'ajouter a posteriori.

Traitement de flux en temps réel

Le traitement par lots traditionnel analyse les transactions des heures, voire des jours, après leur survenue. Les systèmes en temps réel évaluent les transactions lors de l'autorisation, avant même que les fonds ne soient transférés.

L'intelligence artificielle en périphérie et les systèmes distribués permettent cette analyse à très faible latence. Les plateformes de cloud computing fournissent l'infrastructure nécessaire au traitement de millions de transactions par seconde avec des temps de réponse de l'ordre de la milliseconde.

Plus la fraude est détectée rapidement, moins on perd d'argent.

Choisir la bonne plateforme d'apprentissage automatique

Lorsqu'il s'agit de mettre en place un système de détection des fraudes, les organisations doivent choisir entre développer en interne ou acheter une solution. Plusieurs facteurs influencent ce choix.

Développement interne

La conception de systèmes d'apprentissage automatique personnalisés offre une flexibilité et un contrôle optimaux. Les organisations peuvent ainsi les adapter à leurs schémas de fraude spécifiques, à leurs sources de données et à leurs besoins métiers.

Mais cette approche nécessite un investissement substantiel :

- Équipe de science des données possédant une expertise dans le domaine de la fraude

- Ingénierie ML pour le déploiement et la mise à l'échelle en production

- Infrastructure pour la notation en temps réel et l'entraînement des modèles

- Maintenance continue et mises à jour du modèle

Seules les grandes institutions dotées de ressources techniques importantes optent généralement pour un développement entièrement en interne.

Solutions fournisseurs

Les plateformes tierces de détection de fraude proposent des modèles d'apprentissage automatique préconfigurés, des pipelines de données et des outils d'intégration. Elles permettent un retour sur investissement plus rapide et un investissement initial moindre.

Les principaux critères d'évaluation comprennent :

- Performance du modèle sur des types de fraude et des volumes de transactions similaires.

- Exigences d'intégration (API, formats de données, latence)

- Possibilités de personnalisation (réglage des seuils, ajout de fonctionnalités)

- Fonctionnalités d'explicabilité et de conformité

- Structure tarifaire (par transaction, par abonnement, au risque)

De nombreux fournisseurs se spécialisent dans des secteurs d'activité ou des types de fraude spécifiques. Une solution optimisée pour la fraude à la carte bancaire ne sera pas forcément efficace pour les demandes d'indemnisation ou la prise de contrôle de compte.

Approches hybrides

Certaines organisations combinent les plateformes de fournisseurs avec des modèles personnalisés. Elles peuvent utiliser des solutions commerciales pour les schémas de fraude standard tout en développant des modèles spécialisés pour les risques uniques.

Cela permet de concilier rapidité de mise sur le marché et personnalisation, en tirant parti de l'expertise externe tout en développant les capacités internes.

| Approche | Idéal pour | Il est temps de déployer | Personnalisation | Structure des coûts |

|---|---|---|---|---|

| Construction interne | Grandes institutions avec des besoins uniques | 12 à 24 mois | Contrôle total | Investissement initial élevé, développement continu |

| Plateforme fournisseur | Déploiement rapide, modèles éprouvés | 3 à 6 mois | Configuration dans les limites | À la transaction ou par abonnement |

| Solution hybride | Équilibre entre vitesse et personnalisation | 6 à 12 mois | Flexibilité modérée | Modèle mixte |

Mesurer le succès et le retour sur investissement

Les investissements dans la détection de la fraude par apprentissage automatique nécessitent des indicateurs de réussite clairs pour justifier les dépenses continues.

Impact financier direct

Calculer les pertes dues à la fraude évitées :

- Nombre total de tentatives de fraude (détectées + non détectées)

- Fraude détectée par un système d'apprentissage automatique

- Valeur monétaire des fraudes évitées

Comparez cela aux coûts du système (développement, infrastructure, maintenance, temps d'analyse) pour déterminer le retour sur investissement net.

N'oubliez pas de tenir compte des faux positifs. Les transactions légitimes bloquées représentent un manque à gagner et l'insatisfaction des clients. Certains clients abandonnent définitivement les commerçants après une baisse de leurs achats légitimes.

Efficacité opérationnelle

Les systèmes d'apprentissage automatique devraient réduire la charge de travail liée à la vérification manuelle. Suivi :

- Heures d'analyse consacrées à l'examen des transactions signalées

- Pourcentage de transactions nécessitant une vérification humaine

- Il est temps de régler les cas de fraude.

À mesure que les modèles s'améliorent, davantage de transactions devraient être décidées (approuvées ou refusées) automatiquement, et moins d'entre elles devraient nécessiter une enquête d'analyste.

Indicateurs de l'expérience client

La prévention de la fraude ne doit pas nuire à l'expérience client. Surveiller :

- taux d'approbation des transactions

- Plaintes de clients concernant des refus injustifiés

- Frictions liées à l'authentification (étapes de vérification supplémentaires requises)

- Fidélisation de la clientèle après des incidents de fraude ou des refus injustifiés

L’objectif reste d’approuver le maximum de transactions légitimes tout en détectant les fraudes, et non de minimiser les risques à tout prix.

Questions fréquemment posées

Dans quelle mesure l'apprentissage automatique est-il précis pour la détection des fraudes ?

La précision de la détection de la fraude par apprentissage automatique varie considérablement selon le type de fraude, la qualité des données et la méthode d'implémentation. Les systèmes bien implémentés atteignent généralement des taux de précision compris entre 70 et 951 TP3T et des taux de rappel compris entre 80 et 951 TP3T, surpassant largement les systèmes basés sur des règles. Cependant, la précision seule ne suffit pas : des indicateurs clés comme les taux de faux positifs, le volume de vérifications manuelles et l'expérience client sont tout aussi importants. Les méthodes d'ensemble combinant plusieurs algorithmes atteignent généralement les taux de précision les plus élevés, tandis que des modèles plus simples peuvent suffire pour les schémas de fraude les plus courants.

Quelle est la différence entre l'apprentissage supervisé et l'apprentissage non supervisé pour la détection des fraudes ?

L'apprentissage supervisé s'appuie sur des données historiques étiquetées (transactions marquées comme frauduleuses ou légitimes), ce qui le rend idéal pour détecter avec une grande précision les schémas de fraude connus. L'apprentissage non supervisé, quant à lui, identifie les anomalies sans données étiquetées ; il excelle dans la détection de nouvelles techniques de fraude, mais génère davantage de faux positifs. La plupart des systèmes de production utilisent des approches hybrides : des modèles supervisés pour les types de fraude établis et des algorithmes non supervisés pour signaler les schémas inhabituels qui méritent une investigation. Le choix dépend des données d'entraînement disponibles, de la stabilité des schémas de fraude et de la tolérance aux faux positifs.

Comment les systèmes d'apprentissage automatique gèrent-ils les nouveaux types de fraude qu'ils n'ont jamais rencontrés auparavant ?

Les algorithmes d'apprentissage non supervisé et de détection d'anomalies identifient les transactions qui s'écartent significativement des schémas habituels, détectant ainsi les fraudes inédites sans exemples préalables. De plus, la plupart des systèmes mettent en œuvre un réentraînement continu, actualisant régulièrement les modèles avec les transactions récentes, notamment les nouveaux types de fraudes découverts. Certaines implémentations avancées utilisent l'apprentissage par transfert, appliquant les connaissances acquises sur des schémas de fraude similaires à de nouveaux scénarios. L'intervention humaine reste essentielle pour examiner les transactions signalées comme inhabituelles et fournir un retour d'information permettant d'entraîner les modèles face aux menaces émergentes. La combinaison de la détection d'anomalies, de l'apprentissage continu et de la supervision humaine permet une adaptation aux tactiques de fraude en constante évolution.

Quels sont les problèmes de confidentialité des données liés à la détection de la fraude par apprentissage automatique ?

La détection de la fraude par apprentissage automatique exige l'analyse détaillée des informations clients, des comportements et de l'historique des transactions, ce qui soulève d'importantes questions de confidentialité. Les organisations doivent se conformer à des réglementations telles que le RGPD, le CCPA et les exigences sectorielles qui limitent la collecte, le stockage et le traitement des données. Parmi les principaux défis figurent l'obtention d'un consentement éclairé, la minimisation de la durée de conservation des données, l'anonymisation des ensembles de données d'entraînement et la justification des décisions automatisées ayant un impact sur les clients. L'apprentissage fédéré offre une solution en permettant d'entraîner les modèles sans centraliser les données sensibles. Les organisations doivent mettre en œuvre les principes de protection des données dès la conception, réaliser des audits réguliers et veiller à ce que leurs mesures de prévention de la fraude soient conformes à leurs obligations en matière de protection des données.

Combien de temps faut-il pour mettre en œuvre un système de détection de fraude basé sur l'apprentissage automatique ?

Les délais de mise en œuvre varient considérablement selon l'approche et le niveau de préparation de l'organisation. Les solutions des fournisseurs, avec leurs modèles préconfigurés, peuvent être déployées en 3 à 6 mois, l'accent étant mis principalement sur l'intégration et l'ajustement des seuils. Un développement interne sur mesure nécessite généralement 12 à 24 mois, incluant le développement de l'infrastructure de données, l'expérimentation des modèles, le déploiement en production et la validation. Les principaux facteurs influençant les délais sont la disponibilité et la qualité des données, la maturité de l'infrastructure existante, les exigences réglementaires, l'expertise de l'équipe et la complexité organisationnelle. Démarrer par un programme pilote axé sur un type de fraude ou un canal spécifique permet un déploiement initial plus rapide, les enseignements tirés étant ensuite appliqués à un déploiement plus large.

Les petites entreprises peuvent-elles tirer profit de la détection de la fraude par apprentissage automatique ou est-ce réservé aux grandes entreprises ?

La détection de la fraude par apprentissage automatique est de plus en plus utilisée par les entreprises de toutes tailles grâce aux plateformes cloud et aux offres de prévention de la fraude en tant que service (PaaS). Si le développement sur mesure reste onéreux et réservé aux grandes institutions, les solutions des fournisseurs proposent des fonctionnalités d'apprentissage automatique sophistiquées à des prix abordables, souvent avec une tarification à la transaction évolutive en fonction du volume d'activité. Les petits commerçants en ligne peuvent intégrer la détection de la fraude par apprentissage automatique via les processeurs de paiement et les plateformes de commerce qui intègrent ces fonctionnalités. Le critère principal n'est pas la taille de l'entreprise, mais le volume de transactions et l'exposition à la fraude : les entreprises qui traitent suffisamment de transactions pour justifier le coût et générer suffisamment de données pour un entraînement efficace du modèle en tirent le plus grand bénéfice.

À quelle fréquence les modèles de détection de fraude nécessitent-ils un réentraînement ?

La fréquence de réentraînement des modèles dépend du rythme d'évolution de la fraude et du contexte métier. Les secteurs à haut risque, confrontés à des tactiques de fraude en constante évolution, peuvent procéder à un réentraînement hebdomadaire, voire quotidien, en intégrant les dernières tendances en matière de fraude et les données transactionnelles. Dans des environnements de fraude plus stables, un réentraînement mensuel ou trimestriel peut être envisagé. La surveillance continue des indicateurs de performance des modèles permet de déterminer les calendriers de réentraînement optimaux : lorsque la précision chute en dessous des seuils critiques ou que des indicateurs de dérive des données déclenchent des alertes, un réentraînement s'impose, indépendamment du calendrier établi. Certaines organisations mettent en œuvre des processus de réentraînement automatisés qui mettent à jour les modèles en continu, tandis que d'autres effectuent des vérifications manuelles avant le déploiement des versions mises à jour en production.

Conclusion

L'apprentissage automatique a fondamentalement transformé la détection des fraudes, faisant passer les systèmes rigides basés sur des règles à des algorithmes adaptatifs qui apprennent en continu des nouveaux schémas. La combinaison de l'apprentissage supervisé pour les types de fraudes connus et des méthodes non supervisées pour les nouvelles menaces offre une couverture exhaustive que les approches traditionnelles ne peuvent égaler.

La mise en œuvre exige bien plus que de simples algorithmes. Le succès repose sur des flux de données fiables, des indicateurs de performance pertinents, des processus hybrides homme-machine et une surveillance continue. Les organisations doivent trouver un équilibre entre la prévention de la fraude, l'expérience client, la conformité réglementaire et l'efficacité opérationnelle.

Le paysage de la détection de la fraude est en constante évolution. Les réseaux neuronaux graphiques, l'apprentissage fédéré et le traitement de flux en temps réel représentent la prochaine génération de capacités. Mais le principe fondamental demeure inchangé : analyser les transactions à grande échelle, identifier les schémas suspects et s'adapter aux nouvelles menaces plus rapidement que les fraudeurs ne peuvent innover.

Pour les institutions financières, les commerçants et les prestataires de services de paiement, la détection de la fraude par apprentissage automatique est passée d'un avantage concurrentiel à une nécessité opérationnelle. La question n'est plus de savoir s'il faut implémenter l'apprentissage automatique, mais comment le déployer le plus efficacement possible face à des problématiques de fraude spécifiques et dans des contextes commerciaux particuliers.

Prêt à moderniser vos capacités de détection des fraudes ? Commencez par auditer vos systèmes actuels, définir des indicateurs de performance clairs et évaluer si les solutions des fournisseurs ou un développement sur mesure correspondent le mieux aux besoins et aux ressources de votre organisation.