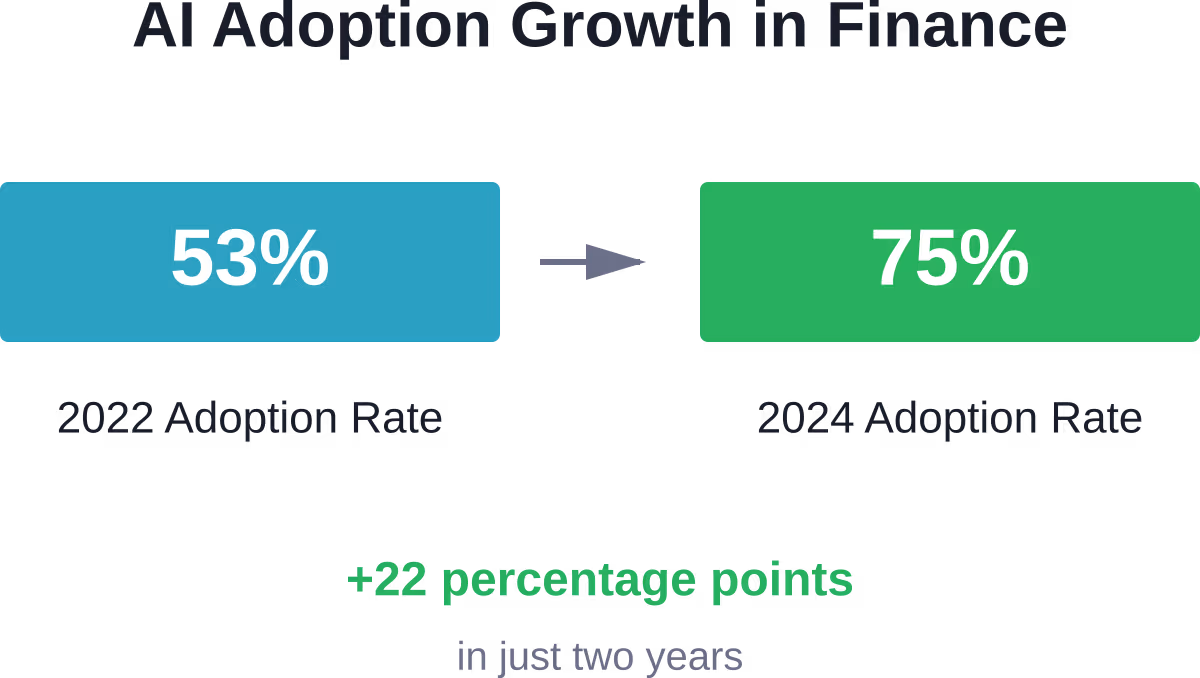

Quick Summary: Machine learning in fintech leverages advanced algorithms to transform financial services through fraud detection, risk management, algorithmic trading, and personalized customer experiences. Financial institutions are rapidly adopting ML technologies, with 75% of major UK and international banks already using some form of AI in their operations as of 2024, up from 53% in 2022.

The financial services industry sits on mountains of data. Transaction records, customer profiles, market movements, credit histories—all creating an environment where machine learning doesn’t just help, it fundamentally changes how finance works.

And the numbers back this up. According to Federal Reserve data cited in a 2026 speech by Vice Chair for Supervision Michelle W. Bowman, the total loss from non-credit card fraud across the financial system was $84 billion in 2024, with only $21 billion recovered, while one in five American adults experienced financial fraud or scams. That’s not a small improvement—that’s a complete transformation of how financial institutions protect themselves and their customers.

But machine learning in fintech extends far beyond fraud prevention. Financial institutions now use ML algorithms for everything from credit scoring to portfolio optimization, from chatbot customer service to detecting money laundering patterns that human analysts would never spot.

The Current State of ML Adoption in Financial Services

The adoption curve tells a clear story. According to the 2026 Global AI in Financial Services Report, 81% of surveyed financial services firms are adopting AI at some level, with 75% of UK financial services firms specifically utilizing the technology as of early 2026.

The job market reflects this shift too. Federal Reserve data shows that approximately 10% of job postings in the financial sector now mention AI-related skills—double the 5% average across all industries.

This isn’t just big banks experimenting with new tech. Machine learning has become infrastructure, the foundation upon which modern financial services operate.

Build Machine Learning Software With AI Superior

AI Superior develops custom AI software, including machine learning models, predictive analytics tools, and AI-based web and mobile applications. Their team supports projects from discovery and data review to MVP development, integration, and result evaluation.

For fintech teams, this can support fraud detection, risk scoring, customer behavior analysis, forecasting, or other data-heavy workflows.

Need Machine Learning Built Around Your Data?

AI Superior can help with:

- building custom machine learning solutions

- developing predictive analytics tools

- testing ideas through PoC or MVP development

- integrating AI into existing systems

👉 Contact AI Superior to discuss your project.

Fraud Detection and Prevention

Financial fraud keeps getting more sophisticated. Check fraud alone saw over 15,000 reports filed between February and August 2023, representing $688 million in transaction value, according to the Financial Crimes Enforcement Network.

Here’s where machine learning shines. Traditional rule-based systems flag transactions based on predetermined criteria—amount thresholds, geographic anomalies, time patterns. But fraudsters learn these rules and work around them.

Machine learning systems don’t work that way. They analyze thousands of variables simultaneously, identifying patterns invisible to human analysts or rigid rule sets. Transaction amount, merchant category, device fingerprint, typing speed, cursor movement—all feeding into models that adapt as fraud tactics evolve.

According to Federal Reserve data cited in a 2026 speech by Vice Chair for Supervision Michelle W. Bowman, the total loss from non-credit card fraud across the financial system was $84 billion in 2024, with only $21 billion recovered, while one in five American adults experienced financial fraud or scams.That’s money that would have disappeared using older detection methods.

Real-Time Fraud Prevention

Speed matters in fraud detection. A fraudulent transaction flagged three days later still means money lost.

Modern ML systems operate in milliseconds, analyzing transactions as they occur. Real-time ML fraud detection systems aim to balance false positive reduction with fraud detection effectiveness.

That balance matters. Flag too many legitimate transactions and customers get frustrated. Miss fraud and everyone loses.

Algorithmic Trading and Investment Management

Financial markets generate massive amounts of data every second. Price movements, trading volumes, news sentiment, economic indicators, social media trends—far more information than human traders can process.

Machine learning algorithms excel at exactly this challenge. They identify correlations across disparate data sources, execute trades based on complex multi-factor models, and adjust strategies as market conditions shift.

Recent research from ArXiv examining Bitcoin trading strategies found that LSTM (Long Short-Term Memory) neural networks achieved a 65.23% cumulative return in 2024, compared to 53.38% for LightGBM models. Even after accounting for a 0.1% trading fee, the LSTM strategy maintained a 53.23% return.

But algorithmic trading isn’t just about cryptocurrency. Equity markets, foreign exchange, commodities—ML algorithms now operate across all asset classes.

Portfolio Optimization

Portfolio construction traditionally relied on Modern Portfolio Theory—balancing expected returns against risk based on historical correlations.

Machine learning approaches incorporate far more variables. Sector rotation patterns, macroeconomic indicators, volatility regimes, liquidity constraints. Deep learning models can identify non-linear relationships that traditional optimization misses.

Stanford’s Advanced Financial Technologies Laboratory highlights how deep recurrent networks capture path dependence in risk predictions—understanding that the sequence of market events matters, not just the events themselves.

Risk Management and Credit Scoring

Determining creditworthiness used to mean checking credit scores, income verification, and employment history. Limited variables, rigid formulas.

Machine learning credit models evaluate hundreds of data points. Payment patterns across multiple accounts, social media activity, browsing behavior, smartphone usage patterns. Controversial? Sometimes. Effective? The data suggests yes.

But effectiveness isn’t the only consideration. The Federal Reserve has emphasized the importance of ensuring AI-based lending doesn’t perpetuate discriminatory practices. Governor Lael Brainard noted concerns about equitable outcomes in financial services, highlighting that ML models must be monitored for bias.

Default Prediction

Predicting loan defaults matters enormously. Lend to someone who won’t repay and the institution loses money. Deny credit to someone creditworthy and both parties miss opportunities.

ML models improve prediction accuracy by identifying subtle patterns in repayment behavior. They spot early warning signs—small changes in transaction patterns that precede financial distress.

This benefits both lenders and borrowers. Better risk assessment means more appropriate pricing and expanded access to credit for those who previously fell into gray areas of traditional scoring models.

Customer Service and Personalization

According to 2026 industry data, 74% of financial services firms have implemented AI-powered customer support, with fintechs leading at 82% compared to 67% among incumbents.

Chatbots represent the most visible customer-facing ML application. But modern financial chatbots go far beyond scripted responses to frequently asked questions.

Natural language processing enables understanding context, sentiment, and intent. A customer asking about “my last payment” gets different responses depending on whether they’re inquiring about a credit card payment they made or a loan payment due.

Personalized Financial Advice

Robo-advisors use machine learning to provide investment guidance previously available only through human financial advisors charging significant fees.

These systems analyze risk tolerance, financial goals, time horizons, and tax situations to recommend portfolio allocations. As circumstances change—a new job, approaching retirement, a market shift—the algorithms adjust recommendations accordingly.

The democratization matters. Personalized financial advice becomes accessible to people with modest account balances who traditional advisory services wouldn’t profitably serve.

Regulatory Compliance and AML

Compliance costs keep rising. Banks have spent over $173 billion since 2007 on staff and systems to maintain compliance with Know Your Customer (KYC), Anti-Money Laundering (AML), and Bank Secrecy Act requirements.

Machine learning helps manage these costs while improving effectiveness. AML systems analyze transaction patterns to identify suspicious activity that might indicate money laundering. They track complex networks of transfers, shell companies, and related accounts—connections that would take human analysts weeks to map.

Real talk: regulation represents one area where ML improvements directly impact profitability. More efficient compliance means lower costs and reduced regulatory risk.

Transaction Monitoring

Traditional transaction monitoring generates enormous numbers of false positives. Legitimate transactions get flagged, requiring manual review that wastes compliance staff time.

ML systems learn what normal looks like for each customer. Large transactions might be routine for a business account but suspicious for a personal account. International transfers might be standard for an import/export company but unusual for a local retailer.

This contextual understanding reduces false positives while catching genuinely suspicious activity more reliably.

Technical Implementation Considerations

Building ML systems for financial applications presents unique challenges. Accuracy matters enormously—errors can mean millions lost or regulatory violations.

Data quality determines model performance. Financial data often comes from disparate systems with inconsistent formats, missing values, and varying update frequencies. Cleaning and standardizing this data represents a major implementation hurdle.

Model Explainability

Regulators increasingly demand transparency. A model that denies credit needs to provide reasons, not just a score. A fraud detection system that blocks transactions must justify its decisions.

Stanford’s Advanced Financial Technologies Laboratory emphasizes variable significance tests for deep nets—understanding which factors drive model predictions. This matters for both regulatory compliance and internal risk management.

Black box models that work brilliantly but can’t explain themselves create regulatory and reputational risks financial institutions can’t afford.

| ML Application | Primary Benefit | Key Challenge |

|---|---|---|

| Fraud Detection | Real-time threat identification | Balancing false positives |

| Credit Scoring | Expanded credit access | Bias prevention |

| Algorithmic Trading | Processing market data at scale | Market volatility adaptation |

| AML Monitoring | Complex pattern detection | Regulatory explainability |

| Customer Service | 24/7 availability | Natural language understanding |

Data Infrastructure Requirements

The scale of data in financial services keeps accelerating. The Federal Reserve noted that in 2013, an estimated 90% of the world’s data had been created in the prior two years. By 2016, that same 90% had been created in the prior year.

This explosion demands serious infrastructure. Storage, processing power, network bandwidth—all require substantial investment. Cloud platforms provide access to pre-trained models and developer-friendly tools that make ML implementation more accessible. Financial institutions can leverage these resources without building everything from scratch.

Privacy and Security

Financial data represents one of the most sensitive categories of personal information. ML systems must protect this data while using it for training and inference.

Techniques like federated learning enable training models on distributed data without centralizing sensitive information. Differential privacy adds mathematical guarantees that individual records remain protected even when models trained on them are deployed.

But security threats evolve too. Machine learning systems can both defend against and enable sophisticated attacks, including phishing campaigns and social engineering.

Performance Benchmarks and Accuracy Gains

The Federal Reserve provides compelling benchmarks for ML performance improvements. Image recognition error rates dropped from 26% baseline to 3.5% after four years of development—better than the 5% human error rate.

Even more impressive: combining AI with human review reduced error rates to just 0.5%. This hybrid approach leverages machine speed and consistency with human judgment and context understanding.

Financial applications see similar patterns. ML models identify patterns humans miss, while humans provide oversight and handle edge cases where models struggle.

Emerging Trends and Future Directions

Foundation models—large language models and other pre-trained systems—represent the cutting edge. According to Bank for International Settlements research, 17% of AI use cases in finance now employ foundation models.

These models bring capabilities that earlier ML approaches couldn’t match. Natural language understanding, zero-shot learning, multi-modal reasoning. They can analyze financial documents, generate reports, answer complex queries, and perform tasks they weren’t explicitly trained for.

But they also introduce new risks. Hallucinations where models confidently state incorrect information. Bias encoded in training data. Concentration risk as many institutions rely on the same handful of foundation model providers.

Financial services will likely see outsized impact given the industry’s information-intensive nature. Processing loan applications, analyzing investment opportunities, detecting fraud—all tasks where ML excels.

Implementation Challenges and Risk Management

Despite the benefits, ML implementation in finance faces real obstacles. Legacy systems that don’t integrate easily with modern ML platforms. Data siloed across departments and subsidiaries. Shortage of talent with both financial domain expertise and ML engineering skills.

Regulatory uncertainty complicates planning. Rules designed for traditional systems don’t map neatly onto ML models that continuously learn and adapt. Supervisors want explainability and stability, while ML systems work best when allowed to evolve.

Model Risk Management

Financial regulators require robust model risk management frameworks. This means documentation, validation, monitoring, and governance processes for ML systems.

Models must be tested on out-of-sample data. Performance metrics tracked over time. Decisions auditable. Override procedures established when human judgment should supersede model outputs.

These requirements add implementation complexity but serve important purposes. Financial institutions can’t afford ML systems that work great in development but fail in production when real money’s at stake.

Skills and Talent Requirements

The Federal Reserve data showing 10% of financial sector job postings mentioning AI skills signals a significant talent demand. That’s double the overall market average.

Financial institutions need data scientists, ML engineers, and AI researchers. But they also need domain experts who understand finance well enough to guide model development and interpret results.

The best ML systems come from collaboration between technical experts and financial professionals. Engineers who understand the math behind neural networks working with traders who understand market microstructure. Data scientists partnering with compliance officers to build AML systems that actually work in practice.

| Role | Key Responsibilities | Required Skills |

|---|---|---|

| ML Engineer | Model development and deployment | Python, TensorFlow, PyTorch, cloud platforms |

| Data Scientist | Analysis and feature engineering | Statistics, SQL, domain knowledge |

| ML Ops Engineer | Production systems and monitoring | DevOps, containers, orchestration |

| Model Validator | Independent model review | Finance, statistics, regulatory knowledge |

Competitive Advantages and Business Value

Financial institutions deploying ML effectively gain measurable competitive advantages. Faster loan approvals attract customers. Better fraud detection reduces losses. More accurate risk models enable better pricing.

According to Federal Reserve data cited in a 2026 speech by Vice Chair for Supervision Michelle W. Bowman, the total loss from non-credit card fraud across the financial system was $84 billion in 2024, with only $21 billion recovered, while one in five American adults experienced financial fraud or scams. That’s money that would have been lost using traditional approaches.

But the value extends beyond cost savings. ML enables entirely new products and services. Micro-loans profitable only because ML automates underwriting. Real-time financial advice at scale. Predictive insights about customer needs before they’re articulated.

Process Optimization Benefits

With 41% of firms using AI to optimize internal processes according to Bank for International Settlements data, operational efficiency represents a major value driver.

Back-office operations—reconciliation, reporting, compliance monitoring—consume enormous resources. ML automation reduces manual work while improving accuracy and speed.

This frees human staff for higher-value activities. Relationship management. Complex problem solving. Strategic planning. Work that requires judgment, empathy, and creativity rather than repetitive data processing.

Frequently Asked Questions

How is machine learning currently used in fintech?

Machine learning powers fraud detection systems, credit scoring models, algorithmic trading platforms, customer service chatbots, and regulatory compliance monitoring. According to Bank of England research, 75% of major financial institutions were using some form of AI by 2024, with applications spanning risk management, process optimization, and customer support.

What’s the difference between AI and machine learning in financial services?

Artificial intelligence is the broader concept of machines performing tasks that typically require human intelligence. Machine learning is a specific subset of AI where systems learn from data without being explicitly programmed. In fintech, most AI applications actually use machine learning techniques like neural networks, decision trees, or deep learning models.

What are the main challenges of implementing ML in financial institutions?

Key challenges include integrating with legacy systems, ensuring data quality across siloed sources, maintaining regulatory compliance, achieving model explainability, managing bias risks, and hiring talent with both financial expertise and ML engineering skills. Financial institutions also face concentration risks as many rely on the same foundation model providers.

Can machine learning models be trusted for critical financial decisions?

With proper governance, yes. Financial regulators require robust model risk management frameworks including validation, monitoring, and documentation. Research shows that combining AI with human oversight achieves the best results—hybrid approaches reduce error rates to 0.5% compared to 3.5% for advanced ML alone or 5% for humans alone, according to Federal Reserve benchmarks.

How does machine learning improve customer service in banking?

ML-powered chatbots provide 24/7 customer support with natural language understanding that goes beyond scripted responses. Robo-advisors deliver personalized investment guidance at scale. Recommendation engines suggest relevant products based on transaction patterns and life events. About 74% of financial firms use AI specifically to enhance customer support, per Bank for International Settlements data.

What’s the future outlook for ML in fintech?

Adoption will continue accelerating. The OECD projects AI will contribute 0.4 to 1.3 percentage points to annual labor productivity growth in G7 economies over the next decade. Foundation models are expanding capabilities in document analysis, multi-modal reasoning, and zero-shot learning. However, institutions must balance innovation with risk management, explainability requirements, and bias prevention.

Conclusion

Machine learning has moved from experimental technology to core infrastructure in financial services. The evidence is clear in adoption rates, fraud prevention results, and productivity gains.

But this isn’t the end of the transformation—it’s the beginning. Foundation models, federated learning, quantum computing integration, and techniques not yet developed will continue reshaping how financial institutions operate.

The institutions that thrive will be those that implement ML thoughtfully. Not chasing hype, but solving real problems. Not replacing human judgment, but augmenting it. Not ignoring risks, but managing them systematically.

Financial services generate the data, face the complexity, and operate under the regulatory scrutiny that make them ideal for ML applications. The question isn’t whether to adopt machine learning—it’s how to do it effectively, responsibly, and competitively.

Start evaluating where ML can deliver the most value in operations. Build the talent pipelines and infrastructure needed. Establish governance frameworks that enable innovation while managing risk. The financial institutions leading the next decade are making those investments today.