Quick Summary: Predictive analytics in financial services uses historical data, machine learning, and statistical models to forecast future trends, detect fraud, assess credit risk, and optimize customer experiences. According to the Federal Reserve, AI-based predictive tools helped the U.S. Treasury prevent and recover $4 billion in fraud during fiscal year 2024 alone. Financial institutions leverage these capabilities to make data-driven decisions, enhance compliance, and gain competitive advantages in an increasingly complex market.

Financial institutions face an avalanche of data every single day. Transaction records, customer interactions, market movements, regulatory filings—it’s overwhelming. But here’s the thing: buried in that chaos are patterns that can predict the future.

Predictive analytics turns raw data into foresight. It’s not about having a crystal ball. It’s about building models that spot trends before they become obvious, flag risks before they materialize, and identify opportunities while competitors are still guessing.

The stakes couldn’t be higher. Check fraud alone generated over 15,000 reports between February and August 2023, representing $688 million in suspicious activity, according to data from the Financial Crimes Enforcement Network cited by the Federal Trade Commission (FTC). Meanwhile, the U.S. Treasury Department used machine learning AI tools to prevent and recover $4 billion in fraud during fiscal year 2024.

But predictive analytics goes far beyond fraud detection. Banks use it to assess creditworthiness, insurers to price policies, investment firms to forecast market movements, and retail banks to personalize customer experiences. The technology reshapes how financial services operate.

What Predictive Analytics Actually Means in Finance

Predictive analytics applies statistical techniques, machine learning algorithms, and data mining to historical data to forecast future outcomes. In financial services, this translates to answering questions like: Will this borrower default? Is this transaction fraudulent? What will cash flow look like next quarter?

The process starts with data collection—transaction histories, customer demographics, market indicators, economic trends. Then algorithms identify patterns and relationships that humans would miss. These patterns become models that score new data and generate predictions.

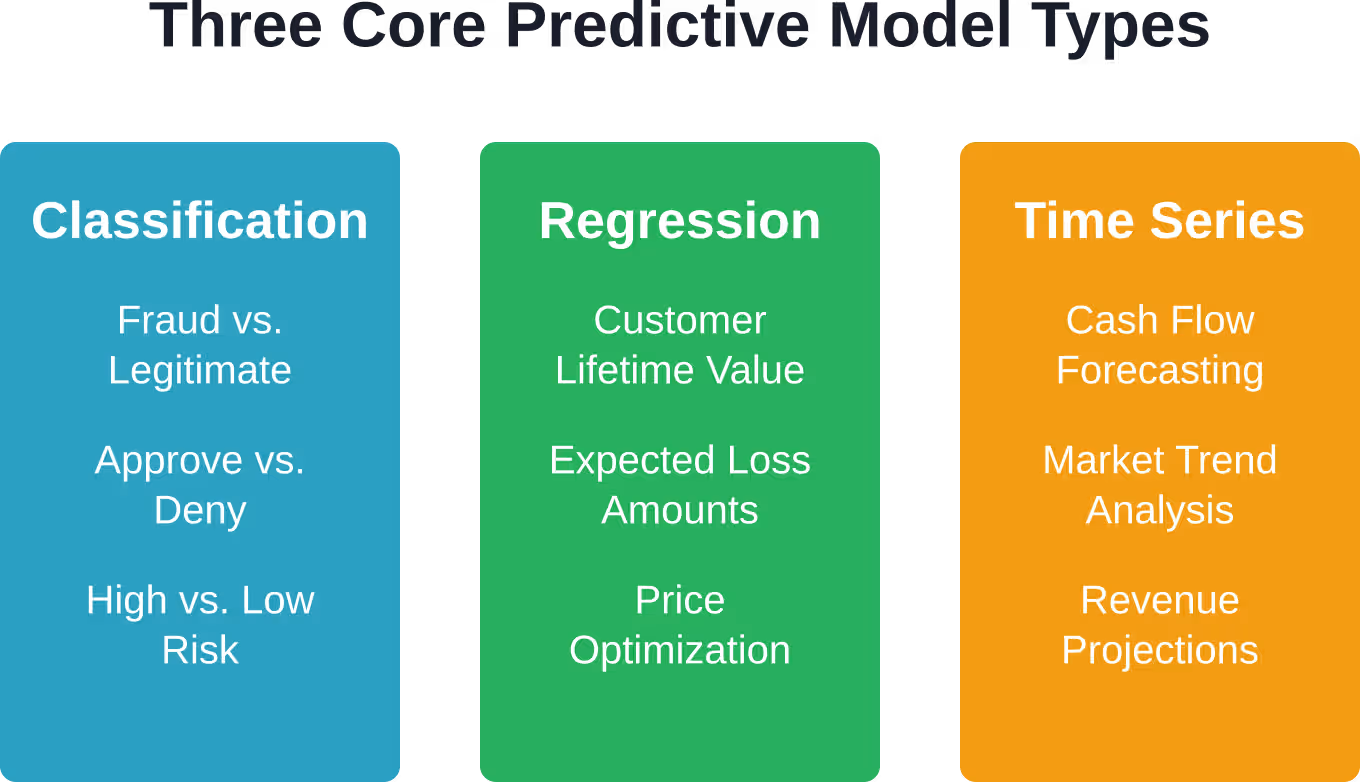

Three core model types dominate financial predictive analytics:

Classification Models

These models sort data into categories. Fraud or legitimate? Approve or deny? High risk or low risk? Banks use classification algorithms like logistic regression, decision trees, and random forests to make binary or multi-category decisions.

One of the largest banks in the United States implemented a fraud detection engine with predictive capabilities from DataVisor, according to implementation case studies. Classification models power these systems by scoring transactions in milliseconds and flagging anomalies.

Regression Models

Regression predicts continuous numeric values rather than categories. How much will this customer spend next month? What’s the expected loss if this loan defaults? What price should we set for this insurance policy?

Linear regression, polynomial regression, and more complex neural network approaches all fall under this umbrella. Financial institutions use regression for everything from pricing derivatives to forecasting revenue.

Time Series Models

Financial data moves through time, making temporal patterns crucial. Time series models like ARIMA, exponential smoothing, and recurrent neural networks analyze sequential data to forecast future values based on historical trends and seasonality.

Cash flow forecasting relies heavily on time series analysis. Organizations that implement advanced predictive models report extending forecast periods from three months to twelve months with improved accuracy.

Critical Use Cases Reshaping Financial Services

Predictive analytics doesn’t sit in research labs. It’s deployed across core business functions, generating measurable returns. Here’s where it matters most.

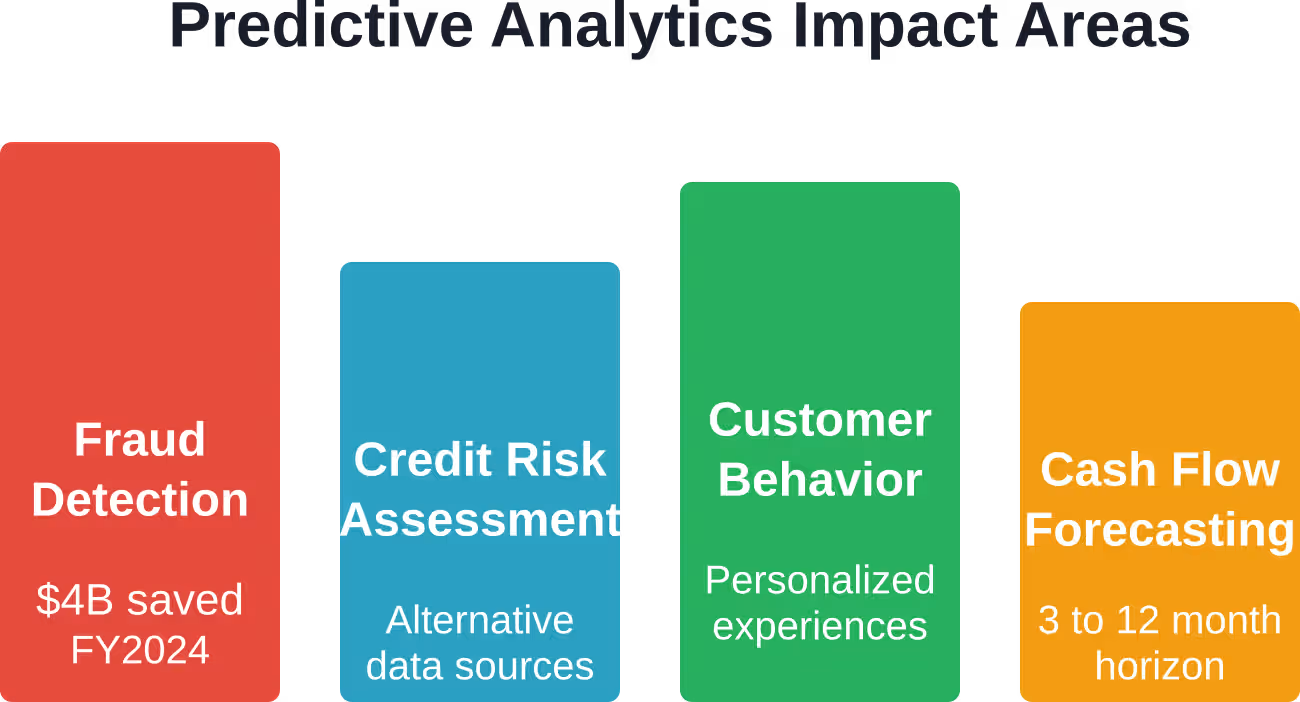

Fraud Detection and Prevention

Fraud costs financial institutions billions annually. Traditional rule-based systems catch obvious patterns but miss sophisticated schemes. Predictive models trained on millions of transactions learn subtle anomalies that signal fraud.

According to Federal Trade Commission (FTC) data, consumers reported losing more than $1.9 billion to fraud in 2019 alone—representing just a fraction of total fraudulent activity banks encounter. Machine learning systems now analyze transaction velocity, geographic patterns, device fingerprints, and behavioral anomalies in real-time.

The Treasury Department’s success—$4 billion in fraud prevention and recovery during fiscal year 2024—demonstrates the power of AI-based predictive analytics at scale. These systems don’t just flag suspicious activity; they adapt as fraudsters change tactics.

Credit Risk Assessment

Banks have always assessed credit risk, but predictive analytics expands beyond traditional credit scores. Models now incorporate alternative data—rental payment history, utility bills, employment patterns, even social media activity—to evaluate creditworthiness.

Machine learning algorithms can identify applicants who traditional scoring would reject but who actually represent good credit risks. The Federal Reserve examined how credit card companies use machine learning to automatically raise credit limits for qualified borrowers, demonstrating how predictive models reshape lending decisions.

But there’s tension here. The SEC proposed new requirements in July 2023 to address conflicts of interest associated with predictive data analytics used by broker-dealers and investment advisers. Regulators worry that optimization for firm profits might not align with customer interests.

Customer Behavior Prediction

Which customers are likely to churn? Who’s ready for a mortgage? What products match individual needs? Predictive models answer these questions by analyzing transaction histories, life events, and engagement patterns.

Financial institutions use these insights to personalize offers, optimize marketing spend, and improve customer retention. Instead of broadcasting generic promotions, banks can target customers at the exact moment they’re most receptive.

The challenge is doing this ethically. Predictive personalization can enhance customer experience or feel invasive depending on implementation. Transparency matters.

Cash Flow Forecasting and Working Capital Management

Corporate finance teams need accurate cash flow predictions to manage working capital, plan investments, and meet obligations. Predictive analytics in accounts receivable provides insights into which invoices might pay late and which customers represent collection risks.

Organizations implementing advanced forecasting models report extending their forecast horizon from three months to twelve months. That visibility transforms strategic planning and capital allocation decisions.

Risk Management and Compliance

Financial institutions operate under intense regulatory scrutiny. Predictive analytics helps identify compliance risks before they trigger violations, monitor for market manipulation, and stress-test portfolios against hypothetical scenarios.

The SEC’s 2020 Staff Report on Algorithmic Trading examined how automated systems impact market stability. As algorithmic and high-frequency trading dominate volume, predictive models become essential for understanding systemic risk.

The Regulatory Landscape

Financial services sit at the intersection of innovation and regulation. Predictive analytics amplifies both opportunities and compliance challenges.

The SEC’s July 2023 proposed rules specifically target conflicts of interest created by predictive data analytics. When algorithms optimize for firm profitability rather than customer outcomes, regulators see problems. Broker-dealers and investment advisers face requirements to demonstrate their predictive systems serve client interests.

Federal Reserve Governor Michelle Bowman addressed AI in financial systems at the November 2024 Building the Financial System of the 21st Century symposium. She emphasized balancing innovation benefits against risks like algorithmic bias, data privacy concerns, and systemic stability.

Governor Lael Brainard highlighted similar themes in a January 2021 speech on responsible AI use. She stressed the importance of equitable outcomes, noting that predictive models trained on biased historical data can perpetuate discrimination in lending, insurance, and other financial services.

The regulatory message is clear: predictive analytics isn’t inherently good or bad. Implementation determines whether it serves customers fairly or creates new risks.

Building a Predictive Analytics Capability

Financial institutions don’t flip a switch and gain predictive powers. Building this capability requires strategic planning, infrastructure investment, and cultural change.

Data Infrastructure Comes First

Predictive models are only as good as their data. That means consolidating siloed databases, establishing data governance, ensuring quality, and creating pipelines that feed models with clean, current information.

Many institutions discover their biggest challenge isn’t algorithms—it’s getting data in usable form. Legacy systems, inconsistent formats, and organizational silos create friction.

Talent and Skills

The job market reflects growing demand for AI skills in finance. Federal Reserve data shows approximately 10% of financial sector job postings now mention AI-related skills, compared to about 5% overall and 20% in the information sector.

Financial institutions need data scientists who understand both machine learning and finance, engineers who can deploy models at scale, and business leaders who can translate predictions into decisions. That’s a rare combination.

Model Development and Validation

Building predictive models involves selecting appropriate algorithms, training on historical data, validating performance, and testing for bias. Models that work in development can fail in production if market conditions shift or data patterns change.

Financial institutions must establish model governance frameworks that document assumptions, monitor performance, and trigger reviews when accuracy degrades. Regulators increasingly scrutinize model risk management.

Integration with Decision Processes

Predictive analytics delivers value when insights drive action. That requires integrating model outputs into workflows, training staff to interpret predictions, and establishing feedback loops that improve models over time.

Some organizations start with pilot projects—applying predictive analytics to a specific problem like invoice collection or credit card fraud. Early wins build momentum for broader deployment.

| Implementation Phase | Key Activities | Common Challenges |

|---|---|---|

| Data Foundation | Consolidate sources, establish governance, ensure quality | Legacy systems, data siloes, inconsistent formats |

| Talent Acquisition | Hire data scientists, train existing staff, build cross-functional teams | Competitive market, skill gaps, cultural resistance |

| Model Development | Select algorithms, train models, validate accuracy, test for bias | Overfitting, concept drift, bias detection |

| Production Deployment | Integrate into workflows, monitor performance, establish governance | System integration, change management, ongoing validation |

The AI Investment Wave

Financial services aren’t adopting predictive analytics in isolation. The broader AI boom drives massive infrastructure investment. According to Federal Reserve Governor Michael Barr’s November 2025 speech, significant infrastructure investment is projected for new data center capacity.

That infrastructure enables more sophisticated models, faster processing, and real-time predictions at scale. Financial institutions that lack access to advanced computing resources face competitive disadvantages.

Cloud providers offer machine learning platforms that democratize access to predictive capabilities. Organizations can now deploy models without building data centers, though questions about data security and regulatory compliance remain.

What’s Next for Predictive Analytics

Technology keeps evolving. Several trends are reshaping what’s possible.

Explainable AI

Early machine learning models operated as black boxes—they made predictions but couldn’t explain why. Regulators and risk managers demanded transparency. Explainable AI techniques now help practitioners understand which factors drive predictions.

This matters for compliance, customer trust, and model validation. When a loan application gets denied, applicants deserve clear explanations, not “the algorithm said no.”

Real-Time Decisioning

Batch processing gave way to real-time predictions. Fraud detection systems now score transactions in milliseconds. Credit decisions happen instantly. Customer offers appear at precisely the right moment.

This speed creates competitive advantages but also raises stakes. Errors propagate faster. Biased models impact thousands of decisions before anyone notices.

Alternative Data Integration

Traditional financial data—credit scores, income, transaction histories—increasingly combines with alternative sources. Satellite imagery predicts agricultural yields. Social media sentiment forecasts brand value. Employment data flows from payroll processors.

Research on financial inclusion using machine learning demonstrates how alternative data helps predict formal financial account ownership in developing markets. Variables like distance to financial service points, trust in providers, and consistent income sources outperform traditional demographic indicators.

Regulatory Technology

Compliance itself becomes a predictive analytics use case. RegTech solutions use machine learning to monitor transactions for anti-money laundering violations, identify insider trading patterns, and ensure algorithmic trading systems operate within rules.

As regulatory complexity grows, manual compliance becomes impossible. Predictive systems that flag risks before they become violations deliver enormous value.

Challenges That Won’t Go Away

Predictive analytics solves problems but creates new ones. Several challenges persist.

Data Privacy and Security

Predictive models require vast amounts of customer data. Breaches expose sensitive financial information. Privacy regulations like GDPR restrict how institutions collect, store, and use data.

Balancing predictive power with privacy protection remains an ongoing tension. Techniques like federated learning and differential privacy offer partial solutions but add complexity.

Algorithmic Bias

Models trained on historical data inherit historical biases. If past lending decisions discriminated against certain groups, predictive models learn and perpetuate that discrimination.

Detecting and mitigating bias requires intentional effort. Diverse teams, fairness metrics, and adversarial testing all help, but the problem doesn’t have easy technical fixes.

Model Risk and Validation

Predictive models fail when underlying patterns change. The 2008 financial crisis revealed how models calibrated on benign market conditions broke down under stress. COVID-19 similarly disrupted models that assumed stable economic patterns.

Continuous monitoring, stress testing, and human oversight remain essential. Automation doesn’t eliminate judgment.

Competitive and Strategic Risk

As predictive analytics becomes table stakes, competitive advantages compress. Institutions that fall behind lack the insights needed to compete. But rushing deployment without proper governance creates different risks.

Strategic planning must balance speed against prudence. SEC Director Brian Daly addressed artificial intelligence and investment management in a February 3, 2026 speech on artificial intelligence and the future of investment management, noting that innovation benefits must be weighed against new vulnerabilities.

Practical Implementation Advice

For organizations starting their predictive analytics journey, several principles increase odds of success:

- Start with clear business problems: Don’t implement predictive analytics because it’s trendy. Identify specific pain points—fraud losses, collection inefficiencies, customer churn—and target those.

- Invest in data infrastructure early: Fancy algorithms can’t compensate for poor data quality. Building solid foundations takes time but pays dividends across every subsequent project.

- Build cross-functional teams: Data scientists alone can’t deliver business value. Teams need domain experts who understand finance, engineers who can scale systems, and business leaders who can drive adoption.

- Establish governance frameworks: Document model assumptions, validation procedures, monitoring protocols, and escalation paths. Regulators will ask for this. More importantly, it prevents disasters.

- Plan for explainability: Black box models create regulatory and reputational risks. Invest in tools and techniques that make predictions interpretable.

- Monitor continuously: Model performance degrades over time as patterns shift. Automated monitoring should trigger alerts when accuracy drops or predictions diverge from expectations.

- Test for bias systematically: Evaluate model outcomes across demographic groups. Look for disparate impact. Include diverse perspectives in design and validation.

| Success Factor | Why It Matters |

|---|---|

| Clear business objectives | Focuses effort on value creation rather than technology for its own sake |

| Data quality and governance | Models cannot overcome poor input data—garbage in, garbage out |

| Cross-functional collaboration | Bridges gap between technical capability and business application |

| Robust model governance | Manages risk, ensures compliance, maintains performance over time |

| Explainability and transparency | Builds trust, enables debugging, satisfies regulatory requirements |

| Continuous monitoring | Detects degradation, identifies bias, triggers timely interventions |

Reduce Fraud And Improve Risk Accuracy With Predictive AI

Fraud, credit risk, and decision delays cost financial institutions real money every day. AI Superior helps turn financial data into working predictive models that identify risks earlier and support faster, more accurate decisions across operations.

Get Predictive Models That Work Inside Your Financial Systems

AI Superior focuses on building AI solutions that fit real financial workflows, not separate analytics layers:

- Custom models for fraud detection, scoring, and risk analysis

- Identification of anomalies and hidden patterns in large datasets

- Support for faster, data-driven decision processes

- Integration into existing systems and internal tools

- Step-by-step rollout starting with small, testable models

Talk to AI Superior and see how your financial data can be used to reduce risk and improve decision accuracy.

Frequently Asked Questions

How much does implementing predictive analytics cost for financial institutions?

Implementation costs vary dramatically based on scope, existing infrastructure, and whether organizations build in-house or buy solutions. Small pilot projects might cost tens of thousands of dollars, while enterprise-wide deployments can run into millions. Cloud-based platforms reduce upfront capital requirements but create ongoing subscription costs. The key cost drivers include data infrastructure modernization, talent acquisition, technology platforms, and ongoing model maintenance. Return on investment typically comes from fraud reduction, improved decision accuracy, and operational efficiency gains.

What skills do teams need to build predictive analytics capabilities?

Successful predictive analytics teams combine several skill sets. Data scientists bring expertise in statistics, machine learning, and programming languages like Python or R. Data engineers build pipelines that collect, clean, and prepare data at scale. Domain experts understand financial services business problems and regulatory requirements. Business analysts translate model outputs into actionable insights. Project managers coordinate cross-functional work. According to Federal Reserve data, about 10% of financial sector job postings now mention AI-related skills, reflecting strong demand for these capabilities.

How do financial institutions address bias in predictive models?

Addressing algorithmic bias requires systematic approaches throughout the model lifecycle. During development, teams use diverse training data and test for disparate impact across demographic groups. Fairness metrics quantify whether model outcomes differ by protected characteristics like race or gender. Techniques like adversarial debiasing and fairness constraints can reduce bias mathematically. Human oversight reviews high-stakes decisions. Regular audits check for emerging bias as populations and patterns shift. Regulators increasingly expect documented bias testing and mitigation procedures as part of model governance frameworks.

Can small financial institutions compete with large banks in predictive analytics?

Size creates advantages—more data, bigger budgets, specialized teams—but doesn’t guarantee success. Small institutions can leverage cloud-based machine learning platforms that democratize access to advanced capabilities without massive infrastructure investment. Focused strategies that apply predictive analytics to specific high-value problems can deliver strong returns even with limited resources. Partnerships with fintech vendors offer another path, though they raise questions about data sharing and vendor dependency. The key is matching ambition to capability and focusing on areas where insights translate directly to business value.

What regulatory requirements apply to predictive analytics in finance?

Regulatory frameworks continue evolving but several requirements already apply. The SEC proposed rules in July 2023 addressing conflicts of interest in predictive data analytics used by broker-dealers and investment advisers. Model risk management guidance from banking regulators requires documentation, validation, and ongoing monitoring of quantitative models. Fair lending laws prohibit discrimination, which extends to algorithmic decisions. Data privacy regulations govern how institutions collect and use customer information. Anti-money laundering rules apply regardless of whether detection systems use rules or machine learning. Specific requirements vary by institution type and jurisdiction, making legal and compliance expertise essential.

How long does it take to see results from predictive analytics investments?

Timeline depends on starting point and objectives. Organizations with clean data and clear business problems can deploy initial models within months. Others spend a year or more building data infrastructure before model development begins. Pilot projects targeting specific use cases—like predicting invoice payment timing or flagging suspicious transactions—often show results in six to twelve months. Enterprise-wide transformations take years. Early wins build momentum and justify continued investment, making phased approaches common. The key is setting realistic expectations and measuring progress with concrete metrics like fraud reduction, forecast accuracy improvement, or operational cost savings.

What happens when predictive models fail or become inaccurate?

Model failures range from gradual accuracy erosion to catastrophic breakdowns during market stress. Continuous monitoring should detect degradation before it causes major problems. When issues emerge, incident response procedures determine whether to disable the model, revert to previous versions, or implement manual overrides. Post-incident analysis identifies root causes—data quality problems, concept drift, implementation bugs, or changed market conditions. Model updates address identified issues through retraining on recent data, algorithm adjustments, or feature engineering. Regulatory expectations include documenting failures, conducting root cause analysis, and implementing corrective actions. Organizations with strong governance frameworks recover faster and avoid repeated mistakes.

The Bottom Line

Predictive analytics fundamentally changes how financial services operate. The technology moves institutions from reactive to proactive, from intuition to evidence, from generic to personalized.

The business case is clear. The U.S. Treasury’s $4 billion in fraud prevention and recovery during fiscal year 2024 demonstrates measurable impact. Extended forecast horizons improve capital planning. Better credit models expand access while managing risk. Personalized customer experiences drive engagement and loyalty.

But implementation demands more than buying software. It requires data infrastructure, specialized talent, governance frameworks, and cultural shifts toward data-driven decision-making. Organizations that treat predictive analytics as a technology project rather than a business transformation typically struggle.

Regulatory scrutiny will intensify as predictive systems grow more powerful. The SEC’s focus on conflicts of interest, Federal Reserve concerns about bias and systemic risk, and evolving privacy regulations create compliance obligations that organizations ignore at their peril.

The competitive landscape doesn’t wait for perfect readiness. Financial institutions that build predictive capabilities gain advantages in fraud prevention, risk management, customer experience, and operational efficiency. Those that delay face growing disadvantages as competitors pull ahead.

The question isn’t whether to adopt predictive analytics. It’s how to implement responsibly, scale effectively, and create sustainable competitive advantages while managing risks and meeting regulatory expectations. Organizations that answer those questions well will define the future of financial services.

Start with clear business problems. Build solid data foundations. Invest in talent and governance. Monitor continuously. Test rigorously for bias. Stay transparent with customers and regulators. The path forward requires balancing innovation against prudence, speed against quality, automation against oversight.

Done right, predictive analytics transforms financial services from an industry drowning in data into one that turns information into insight, insight into action, and action into value.