Quick Summary: Predictive analytics in fraud detection uses machine learning algorithms and statistical models to analyze patterns in historical data, identify anomalies, and forecast fraudulent activities before they occur. By processing vast datasets in real-time, these systems detect suspicious behavior that traditional rule-based methods miss, reducing false positives while catching sophisticated fraud schemes. Organizations implementing predictive analytics can cut fraud losses significantly while improving operational efficiency and customer experience.

Fraud costs organizations billions annually, and the methods criminals use grow more sophisticated every day. According to the Association of Certified Fraud Examiners (ACFE), an average fraud costs an organisation over $1.9 million. That figure doesn’t capture the full damage—reputational harm, customer trust erosion, and regulatory penalties compound the financial hit.

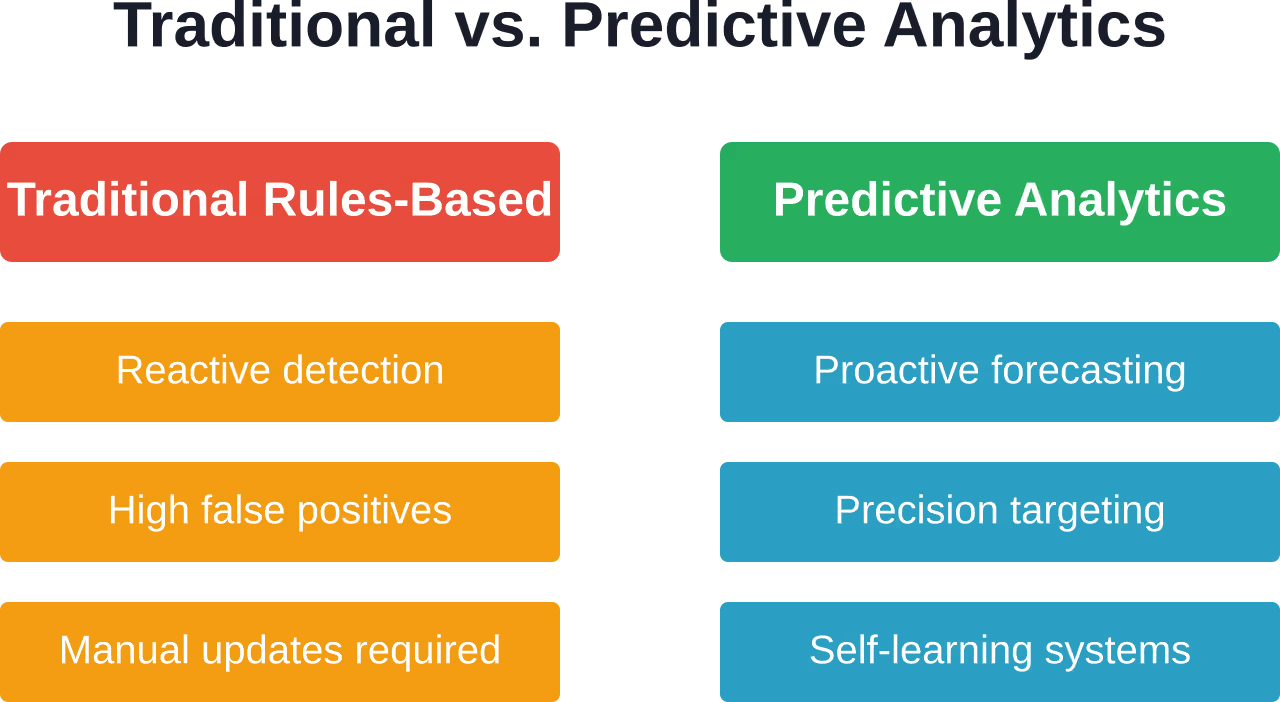

Traditional rule-based fraud detection systems can’t keep pace. They’re reactive, brittle, and generate overwhelming false positives that bury fraud teams in busywork. Predictive analytics changes this dynamic entirely.

What Is Predictive Analytics for Fraud Detection?

Predictive analytics applies statistical algorithms and machine learning techniques to historical data, identifying patterns that signal fraudulent behavior. Instead of waiting for known fraud signatures to appear, these systems forecast which transactions, accounts, or activities will likely turn fraudulent.

The process starts with data integration. Organizations pull information from transaction logs, user behavior databases, device fingerprints, geolocation data, and external threat intelligence feeds. Machine learning models then analyze this information, spotting correlations humans would never catch.

Here’s the thing though—predictive analytics doesn’t just flag suspicious activity. It assigns risk scores to transactions in milliseconds, allowing businesses to automate responses: approve low-risk transactions instantly, flag medium-risk ones for review, and block high-risk attempts outright.

Use Predictive Analytics for Fraud Detection with AI Superior

AI Superior builds predictive models that analyze transaction and behavioral data to identify patterns linked to fraud.

They focus on models that can operate within existing systems and support real-time or ongoing monitoring.

Looking to Apply Predictive Analytics for Fraud Detection?

AI Superior can help with:

- evaluating transaction and behavioral data

- building predictive models

- integrating models into existing systems

- improving detection based on results

👉 Contact AI Superior to discuss your project, data, and implementation approach

Core Techniques Powering Fraud Prevention

Several machine learning methods drive modern fraud detection systems. Each has strengths suited to different fraud scenarios.

Supervised Learning Models

Supervised learning trains on labeled historical data—transactions marked as legitimate or fraudulent. Algorithms like logistic regression, decision trees, and random forests learn to distinguish between the two categories.

Random forests perform particularly well because they handle imbalanced datasets (most transactions are legitimate) and identify complex, non-linear relationships. They’re also less prone to overfitting than single decision trees.

Anomaly Detection

Not all fraud follows known patterns. Anomaly detection algorithms flag transactions that deviate significantly from established baselines. If a cardholder normally withdraws $200 maximum in a specific geographic area, then suddenly attempts a $500 withdrawal in a different zip code, the system triggers an alert.

Clustering algorithms like k-means and isolation forests excel at spotting these outliers without requiring labeled fraud examples.

Neural Networks and Deep Learning

Deep learning models process enormous feature sets—hundreds or thousands of variables—and detect subtle patterns invisible to simpler algorithms. They’re especially effective for image-based fraud detection (fake ID verification) and natural language processing (phishing email detection).

The trade-off? They require massive datasets and significant computational resources.

Real-Time Analysis: The Speed Advantage

Speed separates predictive analytics from traditional methods. Real-time fraud detection systems evaluate transactions in milliseconds, before authorization completes.

According to the Association for Financial Professionals, 76% of organizations faced payment fraud attempts in 2024. Most of those attempts would succeed if systems waited hours or days to analyze transactions. Real-time scoring stops fraud at the point of attempt.

The technical challenge is brutal. Systems must query multiple data sources, run complex models, and return a decision in under 100 milliseconds—while processing thousands of concurrent transactions. Cloud infrastructure and optimized model architectures make this possible.

Benefits Beyond Loss Prevention

Fraud prevention is the obvious win, but predictive analytics delivers broader value.

- Reduced false positives: Traditional systems flag legitimate transactions as suspicious, frustrating customers and burning fraud analyst hours. Machine learning models achieve higher precision through improved algorithms and training methods.

- Improved customer experience: Fewer false declines mean fewer angry customers calling support. Low-risk customers sail through checkout; high-risk transactions get scrutinized. Everyone wins except the fraudsters.

- Operational efficiency: Automating low-risk approvals and high-risk blocks frees analysts to investigate the genuinely ambiguous cases. Organizations report significant reductions in manual review workload through automation.

- Regulatory compliance: Financial institutions face strict anti-money laundering and know-your-customer requirements. Predictive models help satisfy these obligations while documenting decision processes for auditors.

Implementation Challenges

Deploying predictive analytics isn’t trivial. Organizations hit several common roadblocks.

Data Quality and Integration

Machine learning models are only as good as their training data. Incomplete, inconsistent, or siloed data cripples model performance. Integrating transaction systems, CRM databases, fraud case management tools, and external data feeds requires serious engineering effort.

Class Imbalance

Fraud is rare—often less than 1% of transactions. This imbalance confuses many algorithms, which optimize for overall accuracy by predicting everything as legitimate. Specialized techniques like SMOTE (Synthetic Minority Over-sampling Technique) and ensemble methods address this, but require expertise to implement correctly.

Model Explainability

Regulators and compliance teams demand explanations: why did the system flag this transaction? Deep neural networks are notoriously opaque. Organizations increasingly favor interpretable models or use explainability frameworks like SHAP (SHapley Additive exPlanations) to satisfy transparency requirements.

Adversarial Adaptation

Fraudsters aren’t static targets. They test systems, learn what triggers flags, and adapt their techniques. Models must continuously retrain on fresh data to counter these evolving tactics. The feedback loop—incorporating confirmed fraud cases back into training data—is critical.

Industry Applications

Different sectors face distinct fraud challenges, and predictive analytics adapts to each.

| Industry | Primary Fraud Type | Predictive Analytics Application |

|---|---|---|

| Banking | Account takeover, wire fraud | Behavioral biometrics, transaction velocity analysis |

| E-commerce | Payment fraud, refund abuse | Device fingerprinting, purchase pattern analysis |

| Insurance | Claims fraud, application fraud | Anomaly detection in claim amounts, claimant network analysis |

| Healthcare | Billing fraud, identity theft | Procedure code pattern analysis, provider-patient relationship mapping |

| Telecommunications | Subscription fraud, SIM swap | Account activity monitoring, location anomaly detection |

The Automation Factor

Manual review creates bottlenecks. Did you know that 58% of North American businesses conduct manual reviews (12% of orders are reviewed manually)? That’s unsustainable as transaction volumes grow.

Predictive analytics enables tiered automation. Low-risk transactions (say, risk scores below 20) auto-approve. High-risk transactions (scores above 80) auto-decline or trigger multi-factor authentication. The middle tier—scores between 20 and 80—routes to human analysts.

This approach processes the bulk of transactions instantly while focusing human expertise where it matters most. The result? Faster customer experiences and better fraud detection outcomes.

Evolution and Future Trends

Predictive analytics continues advancing rapidly. Graph analytics now map fraud rings by analyzing relationships between accounts, devices, and transaction patterns. Federated learning allows organizations to train shared models without exposing sensitive customer data. Reinforcement learning adapts fraud detection strategies in real time based on fraudster responses.

The broader integration of AI and big data promises even more sophisticated capabilities. According to recent research, AI-driven unemployment insurance fraud detection systems are already demonstrating how these technologies scale to massive datasets while navigating complex regulatory environments.

Organizations that master predictive analytics now will build competitive moats. Those that don’t will hemorrhage money to increasingly sophisticated fraud operations.

Frequently Asked Questions

How accurate are predictive analytics fraud detection systems?

Accuracy varies by implementation quality, data availability, and fraud type. Well-designed systems can achieve high precision in identifying fraudulent transactions while maintaining manageable false positive rates. Continuous model retraining is essential to sustain strong performance levels as fraud patterns evolve.

What data sources do predictive models use?

Effective fraud detection models integrate transaction histories, user behavioral data, device fingerprints, IP geolocation, account age and activity, external threat intelligence feeds, and historical fraud case data. The richness and quality of these data sources directly impact model performance.

Can small businesses afford predictive analytics?

Cloud-based fraud detection platforms have democratized access to predictive analytics. Many vendors offer scalable pricing based on transaction volume, making sophisticated fraud prevention accessible even to smaller merchants. The cost of implementing predictive analytics typically pays for itself through reduced fraud losses and fewer false declines.

How quickly can organizations deploy these systems?

Deployment timelines range from weeks to months depending on existing infrastructure and data maturity. Organizations with clean, integrated data and modern tech stacks can implement cloud-based solutions in 4-8 weeks. Legacy systems requiring extensive data migration and integration may need 3-6 months.

Do predictive models replace human fraud analysts?

No—they augment human expertise. Predictive analytics automates routine decisions and prioritizes cases requiring investigation. Experienced analysts remain essential for investigating complex fraud schemes, tuning model parameters, and adapting strategies to emerging threats. The technology shifts analysts from tedious manual reviews to higher-value strategic work.

How do organizations measure ROI on fraud analytics investments?

ROI calculations typically compare fraud losses before and after implementation, factor in operational cost reductions from automation, and account for revenue recovered through reduced false declines. Most organizations see positive ROI within 12-18 months, with continued benefits compounding as models improve.

What role does regulatory compliance play?

Financial institutions face strict requirements from regulators regarding fraud prevention, anti-money laundering, and customer due diligence. Predictive analytics helps satisfy these obligations while providing audit trails documenting decision processes. Model explainability features address regulators’ concerns about opaque AI decision-making.

Conclusion

Predictive analytics has fundamentally transformed fraud detection from a reactive cleanup operation to a proactive defense strategy. Organizations leveraging machine learning, real-time analysis, and continuous model improvement stay ahead of fraudsters while delivering better customer experiences and operational efficiency.

The technology continues maturing, with graph analytics, federated learning, and reinforcement learning pushing capabilities forward. But the core principle remains constant: analyzing patterns in data reveals fraud that traditional methods miss.

For organizations still relying on rule-based systems, the message is clear—adapt or pay the price in fraud losses and customer friction. The tools exist, the cloud infrastructure is accessible, and the ROI is proven. The question isn’t whether to implement predictive analytics for fraud detection, but how quickly your organization can deploy it effectively.