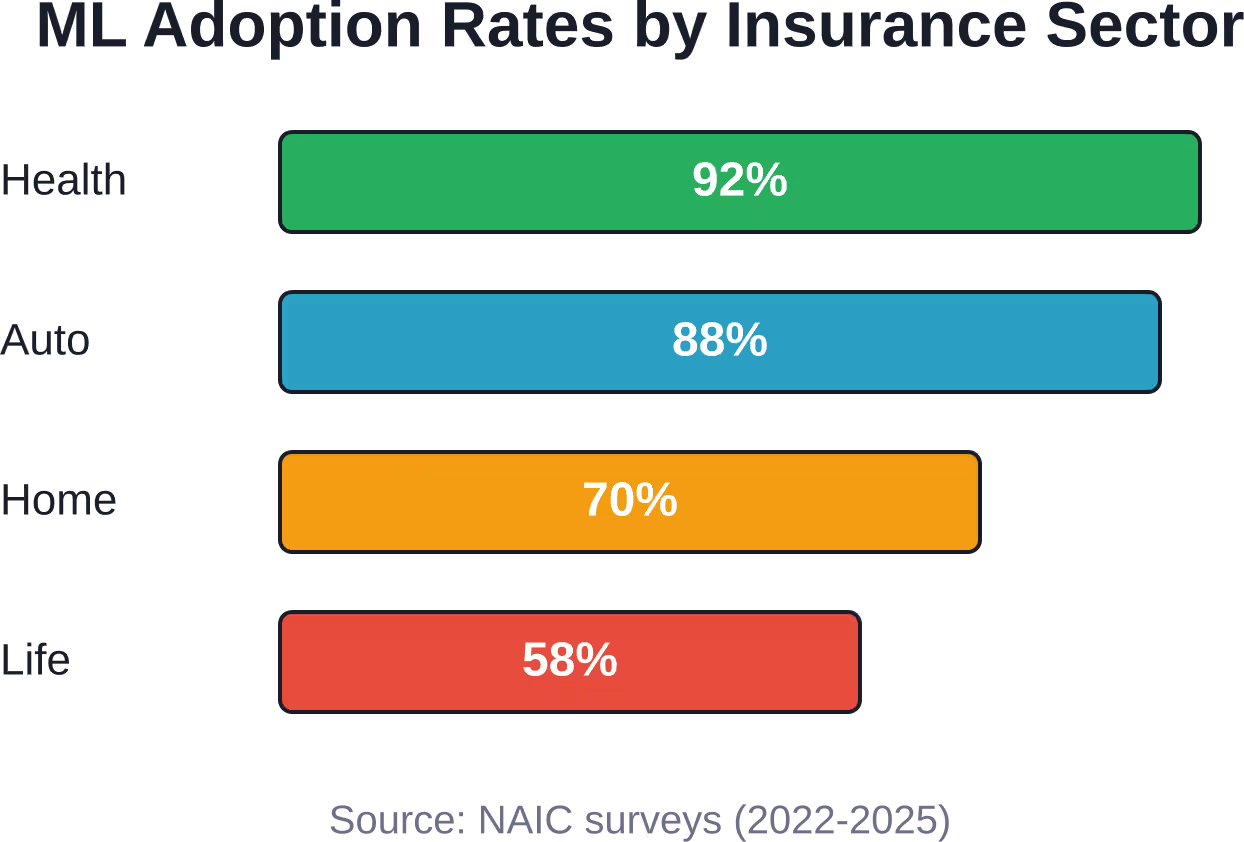

Quick Summary: Machine learning is revolutionizing the insurance industry by automating risk assessment, detecting fraud, personalizing pricing, and streamlining claims processing. According to NAIC surveys, health insurers reported high adoption rates of AI and ML models, with auto insurers at 88% and homeowners insurance adoption reports varying by survey period. These technologies analyze vast datasets to predict claims, identify patterns, and improve operational efficiency across underwriting, customer service, and portfolio management.

The insurance sector has spent decades relying on actuarial tables and manual underwriting. That’s changing fast.

Machine learning algorithms now analyze millions of data points in seconds, uncovering risk patterns that humans would miss. Insurers are adopting these technologies at an unprecedented pace, fundamentally reshaping how policies are priced, claims are processed, and fraud is detected.

According to the National Association of Insurance Commissioners (NAIC), adoption rates vary by sector but the trend is clear: According to NAIC surveys, health insurers reported high adoption rates of AI and ML models. Auto insurance shows high adoption rates, with 88% of auto insurers reporting they use, plan to use, or plan to explore AI/ML models, while homeowners insurance adoption reports vary by survey period, and life insurance adoption continues to develop.

These aren’t just experimental projects anymore. Machine learning has become operational infrastructure.

Why Insurance Companies Are Investing in Machine Learning

Traditional insurance models face fundamental limitations. Actuaries manually segment risk pools, pricing relies on broad demographic categories, and fraud detection happens after claims are paid.

Machine learning solves several critical problems simultaneously:

- Processing massive datasets that exceed human analytical capacity

- Identifying non-obvious correlations between risk factors

- Updating risk models continuously as new data arrives

- Automating repetitive tasks that consume staff time

- Detecting anomalies and patterns associated with fraudulent behavior

The business case is straightforward. Research has found that machine learning can significantly reduce the time spent on fraud detection. When you’re processing thousands of claims daily, that efficiency gain translates directly to cost savings.

But here’s the thing—speed isn’t the only advantage. ML models spot subtle fraud patterns that rule-based systems miss entirely. If an individual holds similar policies with different insurers, algorithms can flag that relationship for investigation even when the applications look legitimate on paper.

Core Applications Transforming the Industry

Machine learning has infiltrated virtually every operational area of insurance. Some applications are more mature than others.

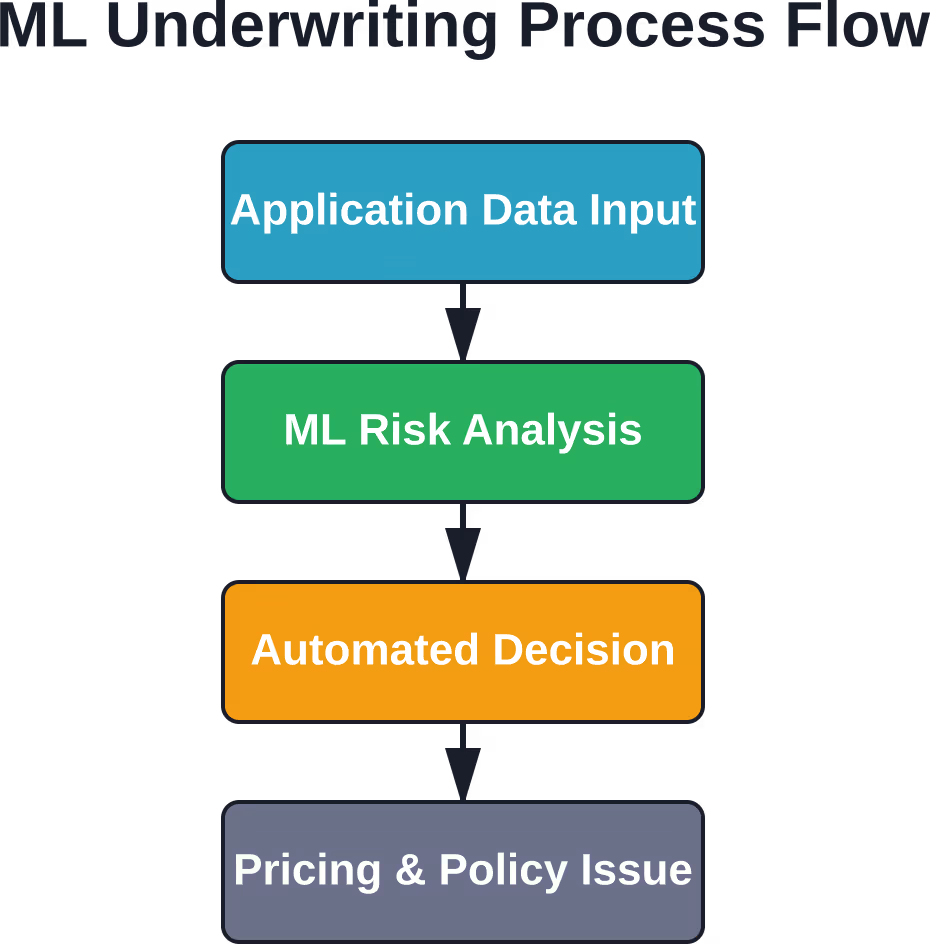

Risk Assessment and Underwriting

Underwriting has historically been a manual, time-intensive process. Underwriters review applications, check documentation, and make judgment calls about risk levels.

ML algorithms automate much of this workflow. They analyze applicant data against historical claim patterns, instantly calculating risk scores. Instead of taking days or weeks, underwriting decisions can happen in minutes.

The models consider hundreds of variables simultaneously—far more than traditional actuarial tables. For auto insurance, this might include driving history, vehicle type, geographic location, credit scores, and even behavioral data from telematics devices.

For health insurance, algorithms predict which applicants are likely to generate high-cost claims based on medical history, prescription records, lifestyle factors, and demographic information.

Fraud Detection and Prevention

Insurance fraud costs the industry billions annually. Traditional detection methods rely on rules engines—if a claim meets certain criteria, it gets flagged for review.

Machine learning takes a different approach. Algorithms learn what normal claim patterns look like, then identify statistical outliers. The models adapt as fraud tactics evolve, unlike static rule sets.

According to NAIC data and research published by IEEE, ML-based fraud detection systems can handle class imbalance datasets with missing values—a common real-world scenario where fraudulent claims are rare compared to legitimate ones.

The algorithms analyze claim timing, documentation patterns, provider relationships, and historical behavior. They don’t just catch obvious fraud; they surface suspicious patterns that warrant human investigation.

Pricing Optimization and Personalization

Pricing strategy was previously carried out manually by actuaries, who relied on broad demographic segments and historical loss ratios. Everyone in the risk category paid roughly the same premium.

ML enables hyper-personalized pricing. Algorithms calculate risk at the individual level, considering unique combinations of factors. Two drivers of the same age in the same city might pay different premiums based on dozens of behavioral and circumstantial variables.

This precision benefits both insurers and customers. Low-risk individuals pay less, improving customer satisfaction and retention. Insurers price risk more accurately, reducing adverse selection and improving loss ratios.

| Pricing Approach | Traditional Actuarial | Machine Learning |

|---|---|---|

| Risk Factors Analyzed | 10-20 variables | 100+ variables |

| Update Frequency | Annual or quarterly | Continuous |

| Personalization Level | Broad segments | Individual-level |

| Processing Speed | Days to weeks | Real-time |

| Pattern Detection | Linear relationships | Non-linear correlations |

Claims Processing and Automation

Claims processing involves document review, damage assessment, fraud checks, and payment authorization. Much of this work is repetitive and rule-based, making it ideal for automation.

ML algorithms can process claims documents, extract relevant information, cross-reference policy terms, and approve straightforward claims without human intervention. Complex or unusual claims still go to adjusters, but routine cases flow through automatically.

Computer vision models assess vehicle damage from photos, estimating repair costs. Natural language processing extracts information from medical records and police reports. The entire claims lifecycle accelerates dramatically.

Insurers can now forecast the types of insurance, coverage plans new customers will buy, and the volume of fraudulent insurance claim filings. This predictive capability allows better resource allocation and staffing decisions.

Transform Insurance Workflows with Reliable ML Solutions

Insurance providers work with growing volumes of customer records, claims data, and operational information that often require faster and more accurate analysis. AI Superior builds machine learning systems that help companies improve internal processes, support data evaluation, and automate repetitive operational tasks.

Looking for Smarter AI Support for Insurance Operations?

AI Superior can assist with:

- Predictive models and behavioral data analysis

- AI tools for large-scale operational data processing

- Custom machine learning pilots and validation stages

👉Reach out to AI Superior to explore machine learning systems tailored to insurance analytics and operational processes.

Adoption Rates Across Insurance Sectors

Different insurance sectors are adopting machine learning at different rates, driven by regulatory environments, data availability, and competitive pressures.

Health insurance shows the highest adoption rate at 92% as of May 2025. This makes sense—health insurers deal with enormous datasets, complex risk factors, and high-value claims that benefit from predictive analytics.

Auto insurance shows high adoption rates, with 88% of auto insurers reporting they use, plan to use, or plan to explore AI/ML models, driven by telematics data availability and competitive pressure to offer usage-based insurance products.

Homeowners insurance adoption reports vary by survey period. Property risk assessment benefits from ML, but the sector has been slower to digitize compared to auto and health.

Life insurance adoption continues to develop. Longer policy lifecycles and more conservative regulatory frameworks may explain the slower uptake.

Common Machine Learning Algorithms in Insurance

Not all ML algorithms are equally suited to insurance applications. Certain model types have proven particularly effective:

- Gradient Boosting Machines (XGBoost, LightGBM): These ensemble methods excel at structured data prediction tasks like claim forecasting and risk scoring. They handle missing data well and capture non-linear relationships between variables.

- Random Forests: Another ensemble technique popular for classification problems like fraud detection. Random forests are interpretable and robust against overfitting.

- Neural Networks: Deep learning models process unstructured data—images for damage assessment, text for document processing, and time-series data for predictive maintenance.

- Generalized Linear Models (GLM) and GAMLSS: These statistical approaches remain relevant, especially in life and health insurance where regulatory requirements favor interpretable models. Research on motor bodily injury claims shows GLM and GAMLSS models remain valuable tools in the ML toolkit.

- Clustering Algorithms: K-means and hierarchical clustering segment customers and policies into meaningful groups, enabling targeted marketing and portfolio management.

Real-World Implementation Challenges

Adopting machine learning isn’t as simple as buying software and flipping a switch. Insurers face significant hurdles:

- Data quality and availability: ML models need large, clean datasets. Many insurers have decades of data trapped in legacy systems with inconsistent formats and missing values. Data integration projects can take years.

- Regulatory compliance: Insurance is heavily regulated. Pricing algorithms must be explainable and non-discriminatory. In June 2022, California Insurance Commissioner Ricardo Lara issued a Bulletin reminding insurance companies that bias and discriminatory use of consumers’ data have no place in the California insurance marketplace, highlighting regulatory scrutiny around ML fairness.

- Model interpretability: Actuaries and regulators need to understand how models make decisions. Complex neural networks operate as black boxes, creating compliance and trust issues.

- Talent shortage: Building and maintaining ML systems requires specialized skills. Insurance companies compete with tech firms for data scientists and ML engineers, often at a disadvantage.

- Change management: Employees accustomed to traditional workflows resist automation. Successful implementations require training, communication, and organizational buy-in.

Future Directions and Emerging Trends

Machine learning in insurance continues evolving rapidly. Several trends are gaining momentum:

- Real-time risk assessment is becoming standard. Telematics devices in vehicles, wearables for health monitoring, and IoT sensors in homes feed continuous data streams to ML models. Policies can adjust dynamically based on actual behavior rather than static predictions.

- Natural language processing is improving customer service. Chatbots handle routine inquiries, sentiment analysis monitors customer satisfaction, and automated systems generate policy documents and explanations.

- Computer vision applications are expanding beyond claims. Satellite imagery and aerial photography assess property risk before issuing policies. Drones inspect roofs and structures, feeding visual data to assessment algorithms.

- Federated learning allows insurers to train models collaboratively without sharing sensitive customer data. This approach addresses privacy concerns while enabling industry-wide pattern recognition for fraud detection.

- Explainable AI (XAI) techniques are developing to meet regulatory requirements. SHAP values, LIME, and other interpretability methods help insurers explain algorithmic decisions to regulators and customers.

Frequently Asked Questions

How does machine learning detect insurance fraud?

ML algorithms analyze historical claims data to learn patterns of legitimate claims, then flag statistical outliers that deviate from normal behavior. Models consider claim timing, documentation consistency, provider relationships, and claimant history. Research shows ML can significantly reduce fraud detection time while catching patterns rule-based systems miss.

Will machine learning replace insurance underwriters?

ML automates routine underwriting tasks but doesn’t eliminate the need for human expertise. Complex cases, unusual risks, and judgment calls still require experienced underwriters. The technology shifts underwriters from data processing to exception handling and relationship management.

How accurate are machine learning pricing models?

ML pricing models typically outperform traditional actuarial methods because they analyze more variables and detect non-linear relationships. Accuracy varies by implementation quality and data availability. Models require continuous monitoring and updating to maintain performance as conditions change.

Can machine learning models be biased against certain groups?

Yes. ML models can perpetuate or amplify biases present in training data. If historical data reflects discriminatory practices, algorithms may learn those patterns. Regulators increasingly scrutinize ML fairness, and insurers must test models for disparate impact across protected classes. California took regulatory action in 2022 specifically addressing this concern.

What data do insurance companies use for machine learning?

Insurers combine internal data (policy history, claims records, customer interactions) with external sources (credit scores, public records, geographic data, weather patterns). Auto insurers add telematics data, health insurers use medical records and prescription histories, and property insurers incorporate satellite imagery and IoT sensor data.

How long does it take to implement machine learning in insurance operations?

Implementation timelines vary widely based on project scope and organizational readiness. Simple applications like chatbots can deploy in months. Comprehensive risk modeling and underwriting automation typically require 12-24 months for data preparation, model development, testing, and regulatory approval.

Do customers benefit from machine learning in insurance?

Low-risk customers benefit from more accurate, personalized pricing that reflects their actual risk profile rather than broad demographic averages. Claims processing becomes faster and more convenient. However, high-risk individuals may face higher premiums or difficulty obtaining coverage as ML enables more precise risk segmentation.

Moving Forward with Machine Learning

The insurance industry’s transformation through machine learning is no longer theoretical. With adoption rates reaching 92% in health insurance and 88% in auto insurance, these technologies have moved from experimental to operational.

The competitive advantage increasingly belongs to insurers who effectively leverage data and algorithms. Those still relying on traditional methods face growing pressure from more efficient, data-driven competitors.

For insurance professionals, the message is clear: ML literacy is becoming as fundamental as actuarial expertise. Understanding how algorithms assess risk, detect patterns, and make predictions is essential for modern insurance operations.

The technology will continue advancing. Real-time risk assessment, automated customer service, and predictive analytics will become standard capabilities rather than differentiators. The insurers that succeed will be those who balance technological capability with regulatory compliance, customer trust, and ethical data use.

Ready to explore how machine learning can transform your insurance operations? Start by auditing your data infrastructure, identifying high-value use cases, and building the internal expertise needed to implement these technologies effectively.