Quick Summary: Machine learning is transforming insurance underwriting by automating risk assessment, reducing processing time, and improving accuracy. Advanced algorithms analyze vast datasets to predict claims likelihood, detect fraud, and personalize premiums—shifting the industry from traditional rule-based underwriting to intelligent, data-driven decision-making that benefits both insurers and policyholders.

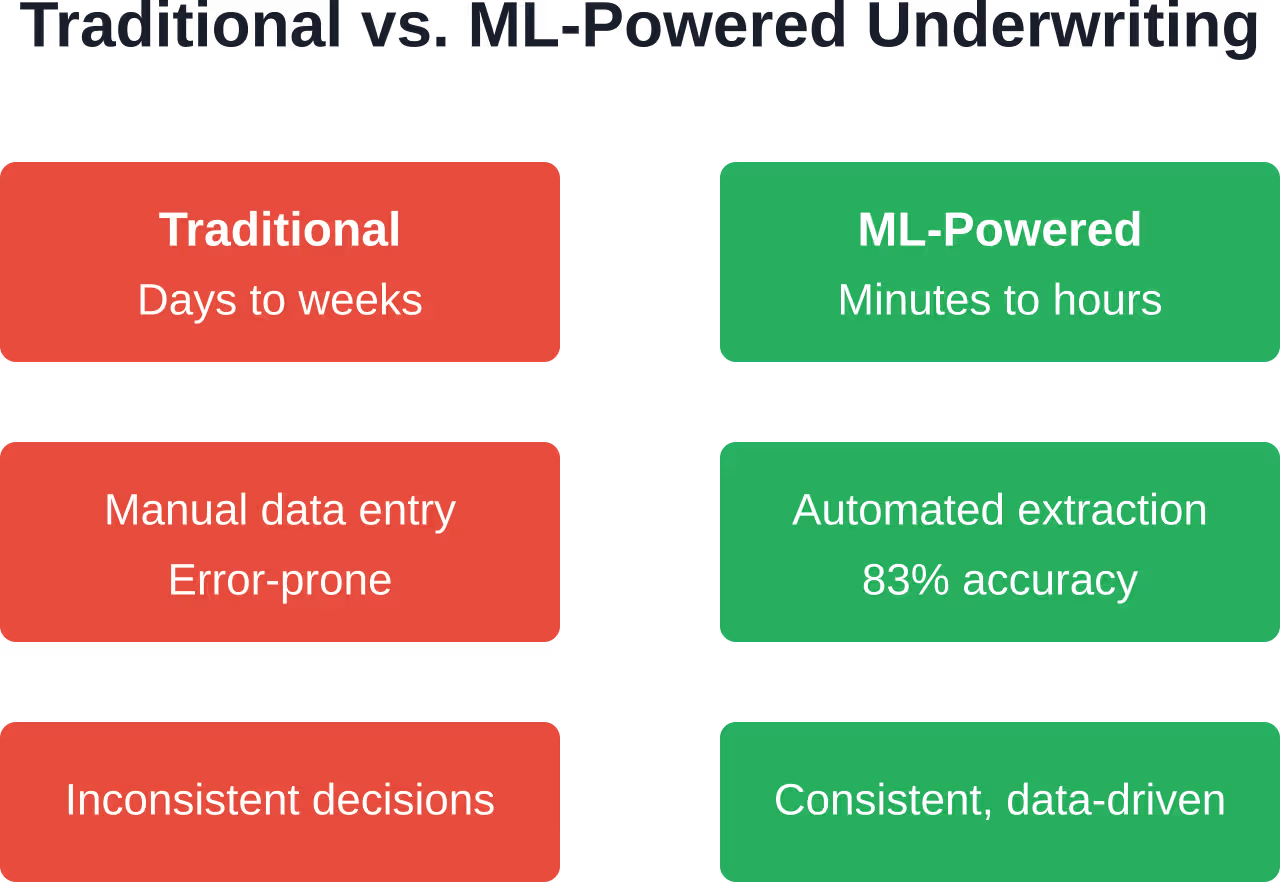

The insurance industry has historically resisted change. For decades, underwriters relied on manual processes, paper-based applications, and rigid rule-based systems to assess risk and price policies.

But that’s changing fast.

Machine learning is reshaping how insurers evaluate risk, process applications, and make underwriting decisions. The technology analyzes massive datasets in seconds, identifying patterns that human underwriters might miss and automating tasks that once consumed hours of manual work.

According to IBM, 90% of the world’s data was generated in just the past two years (as of the time of that statement). That explosion of available information—medical records, driving behavior, property data, social media activity—creates both opportunity and challenge for insurers.

Machine learning thrives on data. And the insurance industry is drowning in it.

Why Traditional Underwriting Is Breaking Down

Traditional insurance underwriting involves human experts reviewing applications, checking databases, requesting additional documentation, and manually calculating risk scores based on established rules and actuarial tables.

It’s thorough. It’s proven. And it’s painfully slow.

McKinsey surveyed insurers about how underwriters spend their time, finding that a substantial portion of underwriter time is devoted to mundane administrative tasks.

That’s not just inefficient—it’s expensive. Every hour an experienced underwriter spends copying data from PDFs or chasing missing documents is an hour not spent on complex risk assessment or relationship building with brokers.

Traditional approaches also struggle with consistency. Different underwriters might assess identical risks differently based on their experience, training, or even their mood that day. Rule-based systems enforce consistency but can’t adapt to nuanced situations or incorporate new data sources without extensive reprogramming.

And here’s the real problem: customer expectations have changed. In an era when people can order products with one click and receive them the same day, waiting weeks for an insurance quote feels absurd.

The Shift to Intelligent Underwriting

Machine learning doesn’t replace underwriters—it amplifies them.

Instead of manually reviewing every application from scratch, underwriters now focus on edge cases, complex risks, and relationship management while algorithms handle the routine assessments.

This transition—often called Underwriting 2.0 or intelligent underwriting—combines human expertise with machine intelligence. The algorithms process structured and unstructured data at scale, flag anomalies, predict outcomes, and recommend decisions. Human underwriters review those recommendations, override when necessary, and continuously improve the models through their feedback.

According to industry surveys, a significant majority of insurers are already implementing or planning to implement machine learning in their underwriting processes.

The technology handles multiple functions simultaneously. It can extract information from uploaded documents, cross-reference external databases, calculate risk scores based on dozens of variables, identify potential fraud indicators, and generate preliminary quotes—all while the applicant waits.

Insurers implementing machine learning report significant improvements in underwriting accuracy, substantial reductions in processing time, and increases in case acceptance rates.

Those aren’t marginal improvements. That’s transformation.

Build Machine Learning Software With AI Superior

AI Superior develops custom AI software, including machine learning models, predictive analytics tools, and AI-based web and mobile applications. Their team supports projects from discovery and data review to MVP development, integration, and result evaluation.

For insurance underwriting teams, this can support risk scoring, applicant data analysis, pricing models, document review, or decision-support tools built around existing insurance data.

Need Machine Learning Built Around Your Data?

AI Superior can help with:

- building custom machine learning solutions

- developing predictive analytics tools

- testing ideas through PoC or MVP development

- integrating AI into existing systems

👉 Contact AI Superior to discuss your project.

Core Machine Learning Use Cases in Underwriting

Machine learning applications in insurance underwriting cluster around several key areas, each addressing specific pain points in the traditional process.

Automated Risk Assessment

Risk assessment forms the heart of underwriting. Machine learning models analyze applicant data alongside historical claims data to predict the likelihood and potential severity of future claims.

These models consider hundreds of variables simultaneously—far more than human underwriters can process manually. For auto insurance, algorithms might evaluate driving records, vehicle safety ratings, geographic risk factors, credit scores, and telematics data showing actual driving behavior.

For life insurance, models incorporate medical history, family health patterns, lifestyle factors, occupation risks, and data from wearable devices. Property insurance algorithms analyze construction materials, roof age, proximity to fire stations, local crime rates, flood zone designations, and satellite imagery showing property conditions.

The algorithms don’t just replicate traditional actuarial tables—they discover new risk correlations that weren’t previously obvious. Some patterns only emerge when analyzing millions of records together.

Document Processing and Data Extraction

Insurance applications generate mountains of paperwork: application forms, medical records, inspection reports, financial statements, driving records, property appraisals.

Machine learning models—particularly natural language processing and computer vision algorithms—can extract relevant information from these documents automatically. They read handwritten forms, interpret medical terminology, extract key figures from financial statements, and populate underwriting systems without manual data entry.

This automation eliminates transcription errors and dramatically speeds up processing. What once required multiple staff members reviewing documents for hours now happens in minutes.

Fraud Detection

Insurance fraud costs the industry billions annually. Machine learning excels at pattern recognition, making it particularly effective at spotting suspicious applications.

Fraud detection models analyze application data for inconsistencies, cross-reference information against external databases and known fraud patterns, and flag anomalies for human review. They might notice that an applicant’s stated income doesn’t match property tax records, that multiple applications share suspicious similarities, or that medical claims don’t align with reported health history.

These systems learn continuously. Each confirmed fraud case trains the model to recognize similar patterns in future applications.

Straight-Through Processing

For straightforward, low-risk applications, machine learning enables complete automation—straight-through processing where applications move from submission to approval without human intervention.

The algorithms assess whether an application falls within pre-defined risk parameters. If it does, the system automatically approves coverage and generates policy documents. If it doesn’t, the application routes to human underwriters for review.

This tiered approach lets insurers process simple cases instantly while focusing expert attention on complex situations that truly require human judgment.

Advanced Applications Pushing the Boundaries

Beyond the core use cases, insurers are experimenting with more sophisticated machine learning applications that push the boundaries of what’s possible in underwriting.

Dynamic Pricing and Personalization

Traditional insurance pricing relies on broad risk categories. Everyone in the same age bracket, geographic area, and risk class pays roughly the same premium.

Machine learning enables true personalization. Algorithms can calculate individualized premiums based on each applicant’s unique risk profile, incorporating hundreds of data points to arrive at a precise price that reflects their actual risk.

This approach benefits low-risk customers who previously subsidized high-risk peers within their risk category. It also helps insurers compete more effectively for desirable customers while maintaining profitability on riskier policies.

Usage-based insurance takes this further. Telematics devices in vehicles or wearable health monitors provide continuous data streams that let insurers adjust premiums based on actual behavior, not just demographic proxies.

Predictive Analytics for Portfolio Management

Machine learning doesn’t just assess individual risks—it helps insurers manage their entire portfolio.

Predictive models analyze portfolio composition, identify concentration risks, forecast future claims patterns, and recommend adjustments to underwriting guidelines to maintain balanced risk exposure.

These insights help insurers avoid overexposure to correlated risks that might all generate claims simultaneously—like properties in hurricane-prone regions or businesses vulnerable to the same economic shifts.

Natural Language Processing for Unstructured Data

Much of the information relevant to underwriting exists in unstructured formats: doctor’s notes, inspection reports, broker communications, social media posts.

Natural language processing models extract insights from these sources. They can read through hundreds of pages of medical records to identify relevant conditions, analyze inspection reports to flag property concerns, or even scan social media activity for risk indicators.

This capability expands the information available to underwriters far beyond structured databases and standard forms.

Real-World Benefits Insurers Are Seeing

The theoretical advantages of machine learning sound compelling. But what are insurers actually experiencing when they implement these technologies?

| Benefit Category | Specific Improvements | Business Impact |

|---|---|---|

| Processing Speed | 10-fold reduction in throughput time | Better customer experience, competitive advantage |

| Accuracy | 95% underwriting accuracy achieved | Fewer claims surprises, better loss ratios |

| Case Acceptance | 25% increase in case acceptance | Revenue growth, market share gains |

| Operational Efficiency | Automation of 35%+ of admin tasks | Cost reduction, capacity for growth |

| Risk Selection | Improved fraud detection and risk segmentation | Portfolio quality improvement, profitability |

These improvements compound. Faster processing leads to happier customers and reduced operational costs. Better accuracy reduces claims losses. Increased case acceptance grows revenue. More efficient operations free up resources for strategic initiatives.

Many industry sources suggest that insurers implementing machine learning in underwriting may see return on investment within a reasonable timeframe,, with benefits continuing to grow as models improve through continuous learning.

Implementation Challenges and Considerations

Machine learning isn’t a magic solution that solves every underwriting challenge instantly. Implementation comes with significant hurdles.

Data Quality and Availability

Machine learning models are only as good as the data they train on. Many insurers struggle with fragmented data across legacy systems, inconsistent data formats, incomplete historical records, and limited access to external data sources.

Cleaning and organizing data for machine learning often requires more time and resources than building the actual models.

Model Explainability and Regulatory Compliance

Insurance is a heavily regulated industry. Regulators require that underwriting decisions be explainable and non-discriminatory.

But many powerful machine learning models—particularly deep neural networks—operate as “black boxes” where even their creators can’t fully explain why they made a specific decision. This creates regulatory and legal risk.

Research from institutions like the Brookings Institution emphasizes the importance of reducing bias in AI-based financial services. Insurers must ensure their models don’t inadvertently discriminate based on protected characteristics, even when those characteristics aren’t explicitly included in the model inputs.

Explainable AI techniques—methods that make model decisions interpretable—are becoming essential for insurance applications. These approaches let underwriters understand why a model made a specific recommendation and verify that it aligns with regulatory requirements and business logic.

Integration with Legacy Systems

Most established insurers run on legacy technology platforms built decades ago. Integrating modern machine learning capabilities with these systems presents significant technical challenges.

Many insurers adopt a hybrid approach, building new machine learning layers that interface with existing systems through APIs rather than attempting complete platform replacements.

Change Management and Skills Gap

Implementing machine learning requires new skills that traditional insurance organizations often lack. Data scientists, machine learning engineers, and AI specialists don’t typically populate insurance companies.

Insurers must either build these capabilities internally through hiring and training or partner with technology vendors and consultants. Either approach requires significant investment and organizational change.

Underwriters themselves need training to work effectively with machine learning tools, understanding their capabilities and limitations and knowing when to trust model recommendations versus overriding them based on expert judgment.

Ethical Considerations and Fairness

Machine learning in insurance raises important ethical questions about fairness, privacy, and discrimination.

Algorithmic Bias

Models trained on historical data can perpetuate or even amplify existing biases in that data. If past underwriting decisions discriminated against certain groups—even unintentionally—models might learn and replicate those patterns.

Research institutions emphasize that diverse development teams and robust bias testing are essential. Models must be continuously audited to ensure they don’t produce discriminatory outcomes based on race, gender, religion, or other protected characteristics.

Privacy Concerns

Machine learning’s power comes partly from incorporating more data sources. But this raises privacy questions. Should insurers use social media activity in underwriting decisions? What about genetic data? Purchase history? Location tracking?

Different jurisdictions answer these questions differently, creating a complex regulatory landscape that insurers must navigate carefully.

Transparency and Consumer Rights

When an algorithm denies coverage or charges a high premium, applicants deserve to understand why. Opacity in algorithmic decision-making can feel unfair and may violate regulatory requirements for explainability.

Insurers implementing machine learning must balance model performance with interpretability, ensuring they can explain decisions to customers and regulators.

The Future of Machine Learning in Underwriting

Machine learning in insurance underwriting is still evolving. Several trends point toward where the technology is heading.

Automated Machine Learning

Building and tuning machine learning models currently requires specialized expertise. Automated machine learning platforms are emerging that let insurance professionals without deep technical backgrounds develop and deploy models.

Research from actuarial scientists explores how automated machine learning can democratize AI adoption in insurance, making these capabilities accessible to smaller insurers who can’t afford large data science teams.

Federated Learning for Data Privacy

Federated learning lets multiple insurers collaborate on model development without sharing sensitive customer data. Models train on distributed datasets while keeping the actual data siloed within each organization.

This approach could enable industry-wide model improvements while addressing privacy and competitive concerns.

Real-Time Underwriting

As data sources become more real-time—IoT sensors in homes and vehicles, wearable health devices, continuous financial monitoring—underwriting could shift from point-in-time assessment to continuous evaluation.

Premiums might adjust in real-time based on changing risk profiles, creating more dynamic relationships between insurers and policyholders.

Integration with Large Language Models

Recent advances in large language models offer new possibilities for processing unstructured text in insurance documents, communicating with applicants through natural conversational interfaces, and synthesizing insights from vast bodies of industry research and regulations.

Organizations like the Society of Actuaries are exploring how these technologies can transform claims processing and underwriting workflows.

Practical Steps for Implementation

For insurers considering machine learning adoption in underwriting, several practical steps can increase the likelihood of success.

- Start with a clear business problem. Don’t implement machine learning for its own sake. Identify specific pain points—slow processing times, high error rates, poor risk selection—and target those with appropriate machine learning solutions.

- Assess data readiness. Before building models, evaluate whether the necessary data exists, is accessible, is sufficiently clean and complete, and can legally be used for the intended purpose.

- Begin with pilot projects. Test machine learning on a limited scope before full deployment. Choose a specific product line or geographic region, measure results carefully, and learn from the experience before scaling.

- Invest in explainability. Build interpretability into models from the start. Understand how models make decisions and be prepared to explain those decisions to regulators, customers, and internal stakeholders.

- Focus on change management. Technology implementation succeeds or fails based on organizational adoption. Train underwriters on new tools, involve them in development processes, and address concerns about job security and changing roles.

- Monitor continuously. Model performance degrades over time as real-world conditions change. Establish processes to monitor accuracy, detect bias, and update models regularly.

Frequently Asked Questions

How does machine learning improve underwriting accuracy?

Machine learning analyzes hundreds of variables simultaneously to identify risk patterns that humans might miss. Models learn from millions of historical cases, recognizing subtle correlations between applicant characteristics and claims outcomes. This data-driven approach reduces both false positives (declining good risks) and false negatives (accepting poor risks), with some insurers reporting accuracy improvements up to 95%.

Will machine learning replace human underwriters?

No. Machine learning augments rather than replaces human underwriters. Algorithms handle routine assessments and data processing, freeing underwriters to focus on complex cases requiring expert judgment, relationship management, and strategic decision-making. The most effective approach combines machine intelligence for pattern recognition and data processing with human expertise for nuanced evaluation and exceptions.

What data do machine learning underwriting models use?

Models incorporate both traditional data sources (application forms, credit reports, medical records, claims history) and emerging ones (telematics data, IoT sensors, social media, satellite imagery, wearable devices). The specific data varies by insurance type—auto, life, property, liability—but generally includes any information legally permissible and predictive of claims likelihood or severity.

How do insurers address bias in machine learning models?

Insurers address bias through diverse development teams, regular model audits for discriminatory outcomes, explainable AI techniques that reveal decision factors, removing protected characteristics from training data, testing models across demographic groups, and continuous monitoring after deployment. Regulatory compliance requires demonstrating that underwriting decisions don’t discriminate based on race, gender, religion, or other protected attributes.

What are the main challenges in implementing machine learning for underwriting?

The primary challenges include data quality issues and fragmented legacy systems, model explainability requirements for regulatory compliance, integration with existing technology platforms, skills gap requiring data scientists and ML engineers, change management and underwriter training, and balancing innovation speed with risk management and regulatory requirements.

How long does it take to see ROI from machine learning underwriting investments?

Industry analyses suggest most insurers see positive return on investment within 18-24 months of implementation. Benefits accumulate over time as models improve through continuous learning, operational efficiencies compound, and organizations develop expertise in leveraging the technology effectively. Initial investments can be substantial, but processing speed improvements, accuracy gains, and operational cost reductions typically justify the expense.

Can small insurers afford machine learning implementation?

Yes, though the approach differs from large insurers. Smaller organizations typically partner with technology vendors offering cloud-based machine learning platforms rather than building in-house capabilities. Many insurtech companies provide accessible machine learning tools specifically designed for smaller insurers. Automated machine learning platforms are also reducing the technical expertise required, making the technology more democratized across the industry.

Conclusion

Machine learning is fundamentally reshaping insurance underwriting. The technology addresses long-standing industry pain points—slow processing, inconsistent decisions, limited data utilization, high operational costs—while creating new capabilities that weren’t previously possible.

Insurers implementing these technologies report dramatic improvements: 10-fold reductions in processing time, 95% accuracy rates, 25% increases in case acceptance, and automation of administrative tasks that previously consumed a third of underwriters’ time.

But implementation isn’t simple. Success requires clean data, regulatory compliance, explainable models, legacy system integration, new technical skills, and effective change management. Ethical considerations around bias, privacy, and fairness demand ongoing attention.

The future points toward even more sophisticated applications—automated machine learning, real-time risk assessment, federated learning, integration with large language models. The underwriting process will continue evolving from manual, rule-based assessment toward intelligent, data-driven decision-making.

For insurers still relying on traditional methods, the question isn’t whether to adopt machine learning but how quickly they can implement it effectively. The competitive advantage is shifting to organizations that can assess risk more accurately, process applications faster, and price policies more precisely through intelligent use of data and algorithms.

The transformation is already underway. The insurers that embrace it thoughtfully—addressing both opportunities and challenges—will define the industry’s next era.