Quick Summary: Machine learning transforms auditing by enabling continuous monitoring, complete population testing, and automated pattern recognition. Auditors leverage ML algorithms for risk assessment, fraud detection, and predictive analytics—shifting from retrospective sampling to real-time assurance while facing governance challenges around transparency and data quality.

Auditing hasn’t just evolved—it’s undergone a fundamental transformation. Machine learning algorithms now analyze entire transaction populations, detect anomalies in milliseconds, and predict risk patterns human auditors would never spot manually.

According to the PCAOB, the Big Four firms audit approximately 80% of U.S. public company market capitalization, and these firms are racing to deploy ML systems that promise 100% testing versus traditional sampling approaches. But what does this technological shift actually mean for audit quality, professional judgment, and the auditor’s evolving role?

The answer isn’t straightforward. Yes, ML delivers speed and scale. But it also introduces governance gaps, transparency challenges, and new skill requirements.

Understanding Machine Learning Fundamentals for Auditors

Machine learning isn’t magic—it’s pattern recognition at scale. The International Auditing and Assurance Standards Board (IAASB) outlines a five-step process that forms the backbone of any ML audit application:

- Get and organize the data

- Choose a model (one or more algorithms)

- Train the model

- Evaluate performance

- Fine-tune parameters

Data quality determines everything. Audit teams face significant challenges in preparing datasets for analysis before any algorithms can effectively process them.

The training-to-testing ratio typically follows a 70/30 split: 70% of available data trains the algorithm to recognize patterns, while the remaining 30% validates whether those patterns hold in unseen scenarios.

Develop AI Tools for Audit Workflows With AI Superior

AI Superior builds AI and machine learning solutions for data analysis, predictive analytics, BI, big data analytics, NLP, and custom software development. Their work can help turn raw, scattered, or complex data into tools that support faster review and clearer decision-making.

For auditing teams, this can support risk scoring, document review, anomaly detection, transaction checks, or other data-heavy audit tasks.

Need AI Connected to Audit Data?

AI Superior can help with:

- creating machine learning models

- building data analysis and BI tools

- testing automation ideas with PoC or MVP work

- connecting AI tools with existing platforms

👉 Contact AI Superior to discuss your project.

Three Core ML Algorithm Types Reshaping Audits

Not all machine learning algorithms serve the same purpose. Audit applications typically leverage three distinct approaches:

| Algorithm Type | Audit Application | Primary Benefit |

|---|---|---|

| Classification | Categorizing transactions as risky or non-risky | Prioritizes audit attention on high-risk items |

| Clustering | Identifying transactions with similar characteristics | Reveals unusual patterns and outliers automatically |

| Association | Detecting correlations between variables | Uncovers hidden relationships in complex datasets |

Classification algorithms answer binary questions: Does this journal entry exhibit fraud indicators? Is this vendor payment within expected parameters? These models learn from historical examples where outcomes are known—flagged frauds, confirmed errors, validated transactions—and apply that learning to new data.

Clustering takes a different approach. Without pre-labeled examples, clustering algorithms group similar transactions together based on shared attributes. A cluster containing just three transactions when all others have hundreds? That’s worth investigating.

Real-World Application: Journal Entry Testing

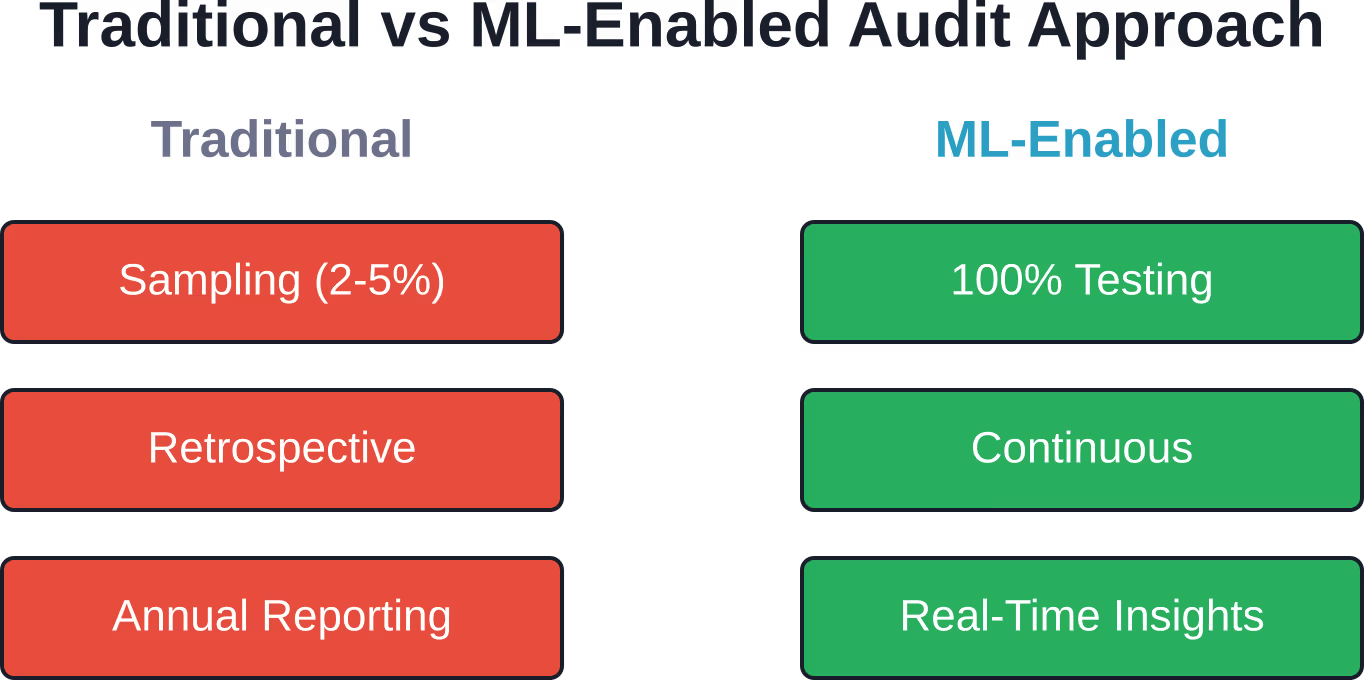

The PCAOB highlights AI-based journal entry testing as a transformative use case. Traditional approaches sample a small fraction of entries—perhaps 25 or 50 from a population of thousands. ML enables 100% testing: every journal entry flows through the algorithm, receives a risk score, and gets flagged for review if it matches learned fraud patterns.

Does that mean zero human judgment? Not remotely. It means auditors spend time investigating genuinely suspicious items rather than randomly selected entries that often reveal nothing.

From Transactional Focus to Interconnected Intelligence

Historical audits operated in discrete phases: plan, test, conclude, report. Machine learning collapses these boundaries.

Continuous auditing becomes viable when algorithms monitor transaction streams in real time. Control testing shifts from annual snapshots to perpetual validation. Risk assessment updates dynamically as new data arrives.

The audit timeline itself morphs. Instead of year-end sprints examining twelve months of activity, auditors conduct ongoing reviews throughout the reporting period. Problems surface when they’re fresh, not months later when remediation options have narrowed.

The Governance Challenge Nobody Talks About

Here’s what the industry white papers won’t emphasize: ML models are black boxes. An algorithm flags a transaction as high-risk—but can the auditor explain why to management, regulators, or courts?

Deloitte reports that two-thirds of banks and insurers now use AI or ML techniques in their operations. Yet governance gaps persist, particularly around model explainability and bias detection.

The IAASB has been developing non-authoritative guidance material addressing technology in audit engagements. The IAASB launched its Technology Quality Management initiative in June 2025, engaging more than 240 stakeholders across six continents. The central question: how do audit standards evolve when algorithms perform substantive testing?

Current standards assume human auditors execute procedures and document their reasoning. Machine learning inverts that model. The algorithm executes procedures automatically; auditors must instead validate the algorithm’s design, training data, and decision logic.

Data Quality: The Foundation That Often Crumbles

ML models inherit the flaws in their training data. Incomplete records, inconsistent formats, historical biases—all become embedded in the algorithm’s learned patterns.

Data quality failures can have significant consequences. Machine learning can accelerate detection of payment anomalies and improper transactions, but only when the underlying data meets minimum integrity thresholds.

Real talk: auditors need data engineering skills now. That wasn’t in the job description five years ago.

Fraud Detection Gets Predictive

Traditional fraud detection waits for red flags—duplicate payments, missing approvals, unusual vendor relationships. By then, money has already moved.

ML fraud models analyze behavioral patterns that precede misconduct. Sudden changes in transaction timing, approval routing, or amount distributions can signal emerging schemes before losses accumulate.

Association algorithms excel here. They identify that certain approvers always sign off on payments to specific vendors, or that journal entries typically occur within certain time windows. Deviations trigger alerts.

But wait. Deviations aren’t automatically fraud. Legitimate business changes produce the same statistical signals. The algorithm can’t distinguish intent—that’s still the auditor’s job.

Skill Transformation: From Vouching to Data Science

According to a Deloitte survey cited in ISACA guidance, 86% of financial services AI adopters say AI will be very or critically important to business success in the next two years. Audit firms recognize this and are restructuring hiring priorities accordingly.

Today’s audit teams increasingly include data scientists, IT specialists, and algorithm validation experts alongside traditional accountants. The auditor’s skill set expands to encompass:

- Python or R programming for data manipulation

- Statistical modeling to understand algorithm behavior

- Data visualization to communicate findings effectively

- Cloud infrastructure knowledge as audit tools migrate to platforms

- Regulatory compliance for automated decision systems

Does every auditor need a computer science degree? No. But every auditor needs enough technical literacy to question an algorithm’s outputs, challenge its assumptions, and recognize when results don’t make business sense.

Regulatory Standards Playing Catch-Up

Standards-setters recognize the gap. The IAASB has been developing non-authoritative guidance material addressing technology in audit engagements.

The challenge? Standards codify professional consensus, but ML practices evolve faster than the standards development process. Guidance published today may describe techniques that firms abandoned six months ago or ignore innovations deployed last quarter.

The PCAOB faces similar pressure. With non-Big Four firms auditing less than 2% of U.S. public company market capitalization combined, resource concentration creates a two-tier profession: large firms deploying cutting-edge ML, smaller firms relying on conventional approaches.

That disparity raises uncomfortable questions about audit quality consistency across the market.

What Happens When Trust Erodes

The Edelman Trust Barometer reported declining trust levels in recent years. Trust in institutions continues declining, with the firm noting a trust crisis beginning in 2017 when trust declined below 50% and slightly recovered in recent years.

Auditors serve as trust intermediaries—assuring stakeholders that financial statements fairly represent economic reality. When algorithms perform that assurance work, stakeholders trust not just the auditor’s judgment but also the algorithm’s design, the data’s integrity, and the firm’s governance over the technology stack.

That’s a much more complex trust chain. Breaking any link fractures confidence in the entire system.

Practical Implementation Steps

Organizations deploying ML in audit functions should follow a structured approach:

- Start narrow: Pilot ML on a single audit area—journal entries, expense reports, contract compliance—before expanding.

- Validate relentlessly: Compare ML outputs against human auditor findings for the first several cycles. Document discrepancies and refine the model.

- Document everything: Algorithm design choices, training data sources, performance metrics, override decisions—all require audit trail quality documentation.

- Invest in training: Audit staff need hands-on experience with ML tools, not just conceptual overviews.

- Establish governance: Define who approves algorithm changes, how model drift gets detected, and what triggers a full retrain.

ISACA’s guidance emphasizes balancing technological capabilities with sound governance and clear objectives. Technology alone doesn’t improve audit quality—thoughtful deployment within robust frameworks does.

Future Trajectory: Where This Goes Next

Machine learning in auditing isn’t approaching maturity—it’s entering adolescence. The foundational capabilities exist, but best practices remain contested and outcomes vary widely.

Expect these developments over the next 24 months:

- Mandatory ML governance disclosures in audit reports

- Specialized audit credentials focused on algorithm validation (ISACA launched the Advanced in AI Audit (AAIA) credential in 2025)

- Increased regulatory scrutiny of firms’ technology quality management systems

- Market pressure forcing smaller firms to adopt ML or exit public company audits

- Client demands for continuous assurance as the standard service model

The firms that thrive won’t necessarily be the ones with the most sophisticated algorithms. They’ll be the ones that integrate ML thoughtfully, govern it rigorously, and communicate its implications transparently.

Frequently Asked Questions

What’s the difference between AI and machine learning in auditing?

Machine learning is a subset of artificial intelligence focused on pattern recognition from data. In auditing, ML typically refers to specific techniques—classification, clustering, association—that analyze transactions and identify anomalies. AI is the broader concept encompassing ML plus natural language processing, computer vision, and expert systems.

Can machine learning replace human auditors?

No. ML automates data analysis and flags items requiring attention, but professional judgment, stakeholder communication, and ethical reasoning remain human responsibilities. The role shifts from vouching individual transactions to validating algorithmic outputs and investigating flagged items. Strategic advisory functions expand as routine testing gets automated.

How accurate are ML fraud detection algorithms?

Accuracy varies dramatically based on training data quality, algorithm selection, and fraud pattern complexity. Well-tuned models achieve 85-95% accuracy in controlled environments, but real-world performance typically falls to 70-80% due to data inconsistencies and evolving fraud schemes. False positive rates matter as much as detection rates—too many false alarms and auditors ignore the system.

What data volume do you need for effective ML auditing?

Minimums depend on the algorithm and use case. Classification models typically need several thousand labeled examples. Clustering can work with hundreds of observations if variables are well-defined. More data generally improves performance, but data quality matters more than volume. Clean, consistent records from 12 months outperform five years of messy, incomplete data.

How do auditors validate that ML models are working correctly?

Validation combines statistical testing, benchmark comparisons, and substantive review. Auditors assess the training data’s representativeness, test model performance on holdout datasets, compare results against prior periods, and investigate samples of flagged and non-flagged items. Regulatory guidance increasingly requires formal model governance frameworks with periodic validation cycles.

What skills should auditors develop to work with ML systems?

Core competencies include basic programming (Python or R), statistical literacy to interpret model outputs, data visualization for communicating findings, and conceptual understanding of common algorithms. Auditors don’t need to build models from scratch, but they must understand enough to challenge assumptions, recognize limitations, and explain results to clients and regulators.

Conclusion: The Transformation Isn’t Optional

Machine learning fundamentally alters what audits can accomplish and what stakeholders should expect. The shift from sampling to comprehensive testing, from annual reviews to continuous monitoring, and from transaction focus to predictive intelligence creates both opportunities and obligations.

Firms that embrace these capabilities thoughtfully—investing in skills, governance, and transparency—position themselves to deliver unprecedented audit quality. Those that don’t risk irrelevance as clients and regulators demand the insights only ML-enabled audits can provide.

The technology exists. The standards are evolving. The question facing every audit organization is whether to lead this transformation or scramble to catch up after competitors have defined the new normal.

Start small, govern rigorously, and keep professional judgment at the center. That’s the formula for turning algorithmic promise into audit value.