Quick Summary: AI will not replace underwriters entirely, but it will fundamentally transform their role. The technology excels at automating routine tasks like data extraction and initial risk scoring, but lacks the contextual judgment, relationship-building skills, and accountability that human underwriters provide. The future belongs to ‘bionic underwriters’ who use AI as a tool to enhance decision-making rather than compete with it.

The question keeps surfacing in insurance boardrooms and mortgage lending offices: will artificial intelligence make underwriters obsolete?

It’s not an unreasonable fear. AI can process thousands of applications in minutes, flag anomalies humans might miss, and work 24/7 without coffee breaks. But here’s the thing—the conversation about AI replacing underwriters misses the actual transformation happening right now.

According to recent industry analysis, the real story isn’t replacement. It’s augmentation.

What AI Already Does in Underwriting

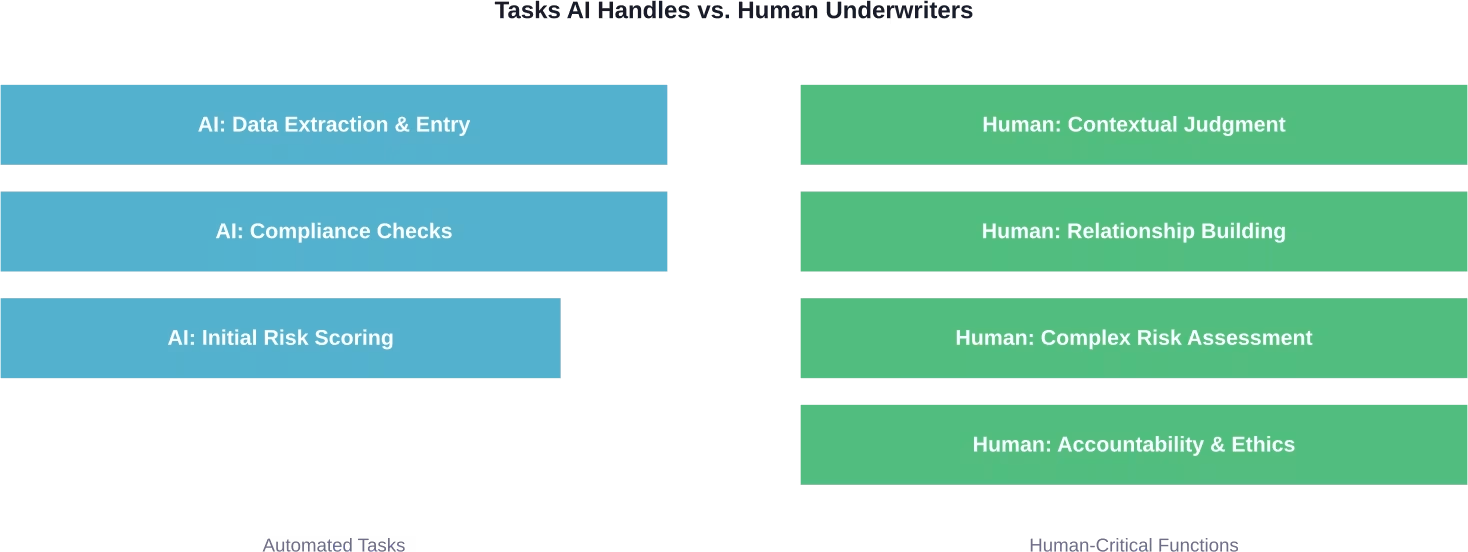

Let’s talk specifics. AI has carved out a clear lane in underwriting workflows, and it’s handling tasks that used to consume hours of an underwriter’s day.

Routine data extraction from submission documents? Automated. Basic compliance checks against regulatory requirements? Done. Initial risk scoring based on historical patterns? Complete before a human even opens the file.

According to hyperexponential research cited by industry sources, 86% of underwriters spend more than two hours per day on manual data entry. That’s the grunt work AI is absorbing first.

Based on McKinsey 2025 AI Report findings referenced in industry discussions, automation can handle up to 70% of straightforward claims, with studies across insurance processes showing similar automation potential. The technology triages submissions, extracts relevant data points, and presents underwriters with pre-analyzed information rather than raw documents.

But here’s where it gets interesting. Shadow mode deployments—where AI runs parallel to human underwriters without making final decisions—show something surprising.

What AI Cannot Do (And Why That Matters)

AI stumbles when the situation demands something beyond pattern recognition.

Think about a commercial real estate application where the numbers look shaky, but the applicant has a compelling business plan and a track record of pivoting successfully during market downturns. Or a mortgage application where income documentation is unconventional because the borrower works in the gig economy.

Data says no. Context says maybe. Experience says yes with conditions.

That’s human territory. AI processes information; underwriters interpret situations. The technology can’t pause and ask, “Does this actually make sense given what’s happening in this specific market right now?”

It can’t sense when an applicant’s story doesn’t match the numbers in ways that matter. It can’t weigh how a sudden regulatory change or market shift might alter the risk profile tomorrow versus today.

And critically—AI cannot be accountable to a client when a decision impacts their financial future. Someone needs to own the call, explain the reasoning, and stand behind the judgment.

The Relationship Factor

Underwriting isn’t just about analyzing risk. It’s about building trust with brokers, understanding client needs beyond the application form, and negotiating terms that work for all parties.

Global specialty insurance leaders emphasize this point: the winners in the next decade won’t be carriers with the flashiest AI tools. They’ll be underwriters who learn to “pilot” AI and data effectively while maintaining the human relationships that drive business.

The Rise of the Bionic Underwriter

Here’s a better framework than replacement: augmentation.

The insurance industry isn’t lacking data anymore. It’s drowning in it. Access to information used to be the biggest hurdle. Now it’s making sense of the flood.

This is where the “bionic underwriter” concept emerges. Not replaced by AI, not ignoring AI, but amplified by it.

These underwriters use artificial intelligence to handle the volume work—the data entry, the initial screening, the compliance verification. That frees them to focus on what machines can’t replicate: strategic thinking, complex risk assessment, client relationships, and portfolio management.

| Traditional Underwriter Role | Bionic Underwriter Role |

|---|---|

| Manual data extraction from documents | AI extracts data; underwriter validates context |

| Hours on compliance verification | Automated compliance with human oversight |

| Individual risk assessment | Portfolio-level strategy and optimization |

| Administrative focus | Relationship and judgment focus |

| Reactive decision-making | Proactive risk management |

According to Brookings research on generative AI and the American worker, more than 30% of all workers could see at least 50% of their occupation’s tasks disrupted by generative AI. For underwriters, that transformation is already underway.

How the Underwriter Role Is Changing

The shift is from risk picker to portfolio architect. From document processor to strategic advisor.

Underwriters increasingly spend time on higher-value activities. They’re analyzing market trends, developing pricing strategies, mentoring junior staff, and building broker relationships. The administrative burden that used to consume 60-70% of their day? AI handles that now.

One industry professional noted in community discussions that AI is brilliant at volume work—scanning thousands of applications, highlighting anomalies, flagging risks. But the human element remains irreplaceable for decisions requiring accountability and contextual understanding.

New Skills for a New Era

The underwriters thriving in 2026 aren’t just insurance experts. They’re becoming data interpreters, AI tool operators, and strategic thinkers.

They need to understand what AI recommendations mean, when to trust them, and when to override them. That requires comfort with technology, but also confidence in professional judgment.

Change management is critical here. Insurance companies need to rewire operations from the ground up, adopting what some call “agentic” architecture—multiple AI systems collaborating under human direction.

But technology is only part of it. Internal talent development and cultural buy-in matter just as much. Companies seeing success start with leadership commitment, identify champions in the middle ranks, and give teams permission to experiment.

Industry-Specific Impacts

The AI effect varies by underwriting type.

Mortgage Underwriting

Residential mortgage underwriting sees heavy AI adoption for conforming loans. Standard documentation, clear guidelines, predictable risk factors—perfect for automation.

But non-qualified mortgage applications? Self-employed borrowers? Complex financial situations? Human underwriters remain essential for these edge cases, which represent a significant portion of the market.

Commercial Insurance

Commercial lines present more complexity. Every large commercial risk is somewhat unique. The property might be standard, but the business operations, management quality, loss control measures, and market conditions create layers of nuance.

AI assists by pulling relevant loss data, comparing similar risks, and identifying potential red flags. The underwriter synthesizes this information with site visit impressions, broker intelligence, and market knowledge to make the call.

Specialty Lines

Specialty insurance—think cyber liability, directors and officers coverage, professional indemnity—relies heavily on emerging risk assessment. AI can track trends and flag concerns, but underwriting these lines requires industry expertise and forward-looking judgment that machines don’t possess.

What the Data Shows About Job Security

According to industry reporting, AI replacement fears fall sharply among underwriters and actuaries.

Why? Because professionals working alongside AI realize it’s a tool, not a threat. It makes their work more interesting by removing drudgery and elevating their role to strategic advisor.

The concern shouldn’t be “will I have a job?” It should be “am I developing the skills to work effectively with AI?”

Underwriters who resist the technology, who insist on doing everything manually because “that’s how we’ve always done it”—they’re at risk. Not from AI directly, but from underwriters who embrace augmentation and deliver better results faster.

As industry leaders have noted: AI won’t replace underwriters, but underwriters who use AI will replace underwriters who don’t.

Implementation Realities

Rolling out AI in underwriting isn’t flip-a-switch simple.

Insurance companies face challenges integrating AI with legacy systems. Data quality issues emerge—garbage in, garbage out applies ruthlessly to machine learning. Regulatory concerns about algorithmic bias and decision transparency require careful navigation.

Smart insurers start small. Pilot programs in specific lines of business. Shadow mode deployments where AI makes recommendations that underwriters review but don’t necessarily follow. Iterative learning and adjustment.

Industry analysis from 2025 Joint Industry Forum discussions highlighted that beyond technology implementation, change management and talent development are essential for realizing AI’s potential in insurance operations.

Break Underwriting Down Before Assuming Replacement

Underwriting isn’t one task that AI can take over. It’s a chain of checks, data inputs, and decisions. Some parts are structured and repeatable, others depend on context and risk judgment. That’s why AI usually fits into specific steps, not the whole role. AI Superior works on that level.

They help companies map how processes actually work, then build AI components around the parts that can be improved, using data-driven models and custom systems that connect to what’s already in place. The focus is on making those pieces work together in real conditions, not creating isolated tools. If you’re looking at AI in underwriting, it’s more useful to start with how your process is structured today.

👉Reach out to AI Superior and see which parts can be optimized without changing how decisions are made.

The Path Forward

So will AI replace underwriters?

No. But it will fundamentally reshape what underwriting looks like as a profession.

The administrative underwriter—the person who primarily processes applications and verifies documentation—that role is endangered. Automation handles those tasks more efficiently.

The strategic underwriter—the professional who assesses complex risks, builds relationships, manages portfolios, and exercises seasoned judgment—that role is more valuable than ever. AI amplifies these capabilities rather than replacing them.

The transformation is already happening. Underwriters spending less time in spreadsheets and more time thinking strategically. Less time on data entry and more time on risk assessment. Less time as order-takers and more time as trusted advisors.

That’s not replacement. That’s evolution. And for underwriters willing to adapt, it’s an upgrade.

Frequently Asked Questions

Will AI completely replace underwriters in the next 5-10 years?

No. AI will automate routine underwriting tasks like data extraction and initial risk scoring, but human judgment remains essential for complex risk assessment, relationship management, and accountability. The role will transform rather than disappear, with underwriters focusing on higher-value strategic work while AI handles repetitive tasks.

What underwriting tasks can AI handle effectively?

AI excels at data extraction from documents, compliance verification, initial risk scoring, pattern recognition, fraud detection, and triaging submissions. According to industry research, AI can automate up to 70% of straightforward cases, particularly in personal lines and conforming mortgage applications where guidelines are clear and standardized.

What skills do underwriters need to stay relevant as AI advances?

Underwriters need to develop comfort with AI tools and data interpretation, strengthen strategic thinking and portfolio management capabilities, and enhance relationship-building skills. The ability to understand AI recommendations, know when to trust or override them, and apply contextual judgment that machines lack will differentiate successful underwriters.

Which types of underwriting are most vulnerable to AI automation?

Personal lines insurance and conforming residential mortgages face the highest automation potential due to standardized guidelines and clear documentation requirements. Simple commercial risks with straightforward applications are also candidates. Complex commercial lines, specialty insurance, and non-standard mortgage applications require human expertise that AI cannot replicate.

How is AI currently being used in underwriting?

Insurance companies deploy AI for automated data extraction, preliminary risk assessment, compliance checking, and submission triage. Many insurers use “shadow mode” where AI makes recommendations alongside human underwriters for validation and learning. The technology processes routine applications while flagging complex cases for human review.

What are the biggest challenges in implementing AI for underwriting?

Major challenges include integrating AI with legacy insurance systems, ensuring data quality for accurate machine learning, addressing regulatory concerns about algorithmic bias and transparency, and managing organizational change. Beyond technology, companies need cultural buy-in from underwriters and investment in training to realize AI’s benefits.

Should current or aspiring underwriters be worried about their career prospects?

Underwriters who embrace AI as a tool to enhance their capabilities have strong career prospects. The profession is shifting toward strategic advisory roles that offer more interesting work and higher value. Those who resist technology and insist on manual processes face greater risk—not from AI directly, but from colleagues who leverage augmentation to deliver better results.