Quick Summary: Predictive analytics in banking uses artificial intelligence, machine learning, and statistical algorithms to analyze historical and real-time data, enabling financial institutions to forecast customer behavior, detect fraud, assess credit risk, and personalize services. As of 2024, 75% of major banks and financial firms are already using some form of AI in their operations, up from 53% in 2022. This technology helps banks prevent fraud worth billions annually, reduce credit defaults, and deliver hyper-personalized customer experiences.

Banking hasn’t just gone digital. It’s gone predictive.

From the moment someone opens a mobile banking app to check their balance, algorithms are working in the background—analyzing spending patterns, flagging unusual transactions, and even predicting whether that person might switch to a competitor. This isn’t science fiction. It’s happening right now at every major financial institution.

According to data from the Bank of England, 75% of financial firms surveyed in 2024 are already using some form of AI in their operations. That’s a significant jump from 53% just two years earlier in 2022. The adoption isn’t limited to tech-forward startups either—all large UK and international banks, insurers, and asset managers that responded to the survey reported AI implementations.

But what exactly makes predictive analytics so transformative for banking? And why are institutions racing to implement these systems despite the complexity and regulatory scrutiny?

What Is Predictive Analytics in Banking?

Predictive analytics refers to the use of statistical algorithms, machine learning models, and artificial intelligence to analyze current and historical data in order to forecast future outcomes. In banking, this means turning massive datasets—transaction histories, customer interactions, market trends, social media activity—into actionable insights.

The technology combines several disciplines. Machine learning algorithms identify patterns humans would miss. Statistical models quantify probabilities and risk. Big data infrastructure processes information at scale. Together, these components enable banks to move from reactive to proactive decision-making.

Here’s the thing though—predictive analytics isn’t just one tool. It’s an ecosystem of technologies working together. A fraud detection system might use neural networks to spot anomalous transactions. A credit scoring model might blend logistic regression with gradient boosting. Customer churn prediction often relies on ensemble methods combining multiple algorithms.

The shift from traditional analytics to predictive systems represents a fundamental change in how banks operate. Traditional business intelligence tells you what happened last quarter. Predictive analytics tells you what’s likely to happen next quarter—and what to do about it.

Why Banks Are Going All-In on Predictive Technology

The financial services industry faces pressures that make predictive analytics not just useful, but essential. Fraud is escalating. Customer expectations are rising. Regulatory requirements are tightening. Competition from fintech startups is intensifying.

Consider fraud alone. According to the Financial Crimes Enforcement Network, there were over 15,000 reports related to check fraud involving mail theft received between February and August of 2023, associated with over $688 million in fraudulent transactions. Traditional rule-based systems struggle to keep pace with sophisticated fraud schemes that constantly evolve.

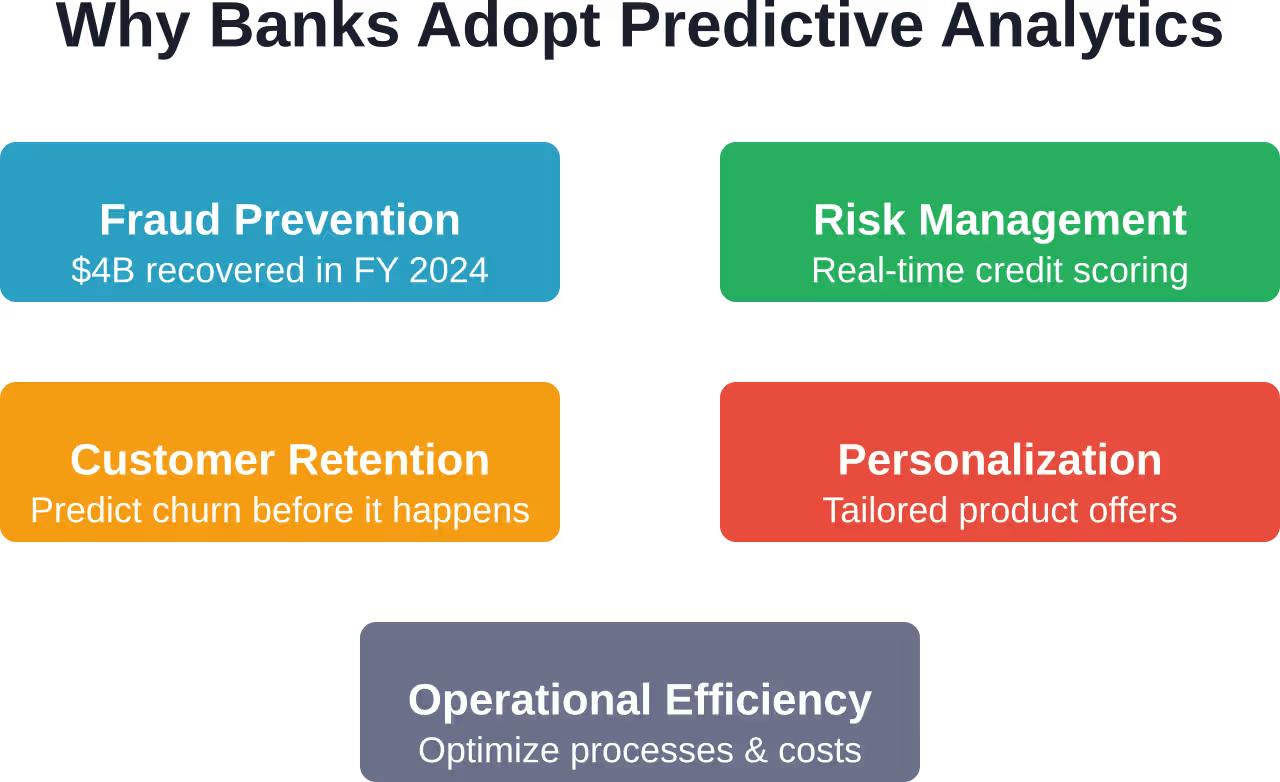

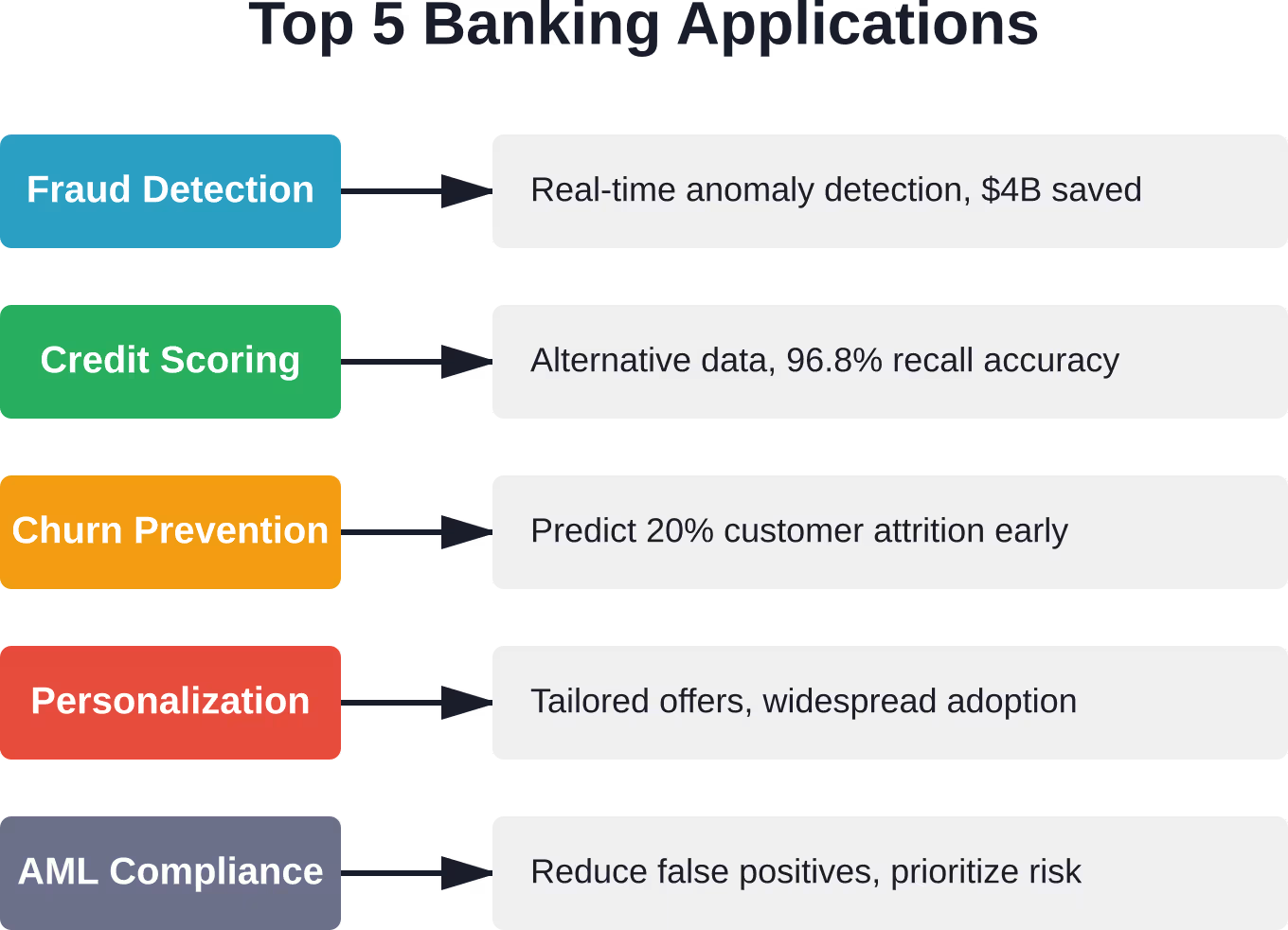

Predictive models offer a different approach. Instead of relying on predetermined rules, machine learning systems learn from patterns in fraudulent and legitimate transactions. They adapt as fraud tactics change. The U.S. Treasury reported that AI tools prevented and recovered $4 billion in fraud during fiscal year 2024, with $1 billion of that specifically from treasury check fraud.

But the drivers go beyond fraud prevention. Banks are sitting on unprecedented volumes of customer data. Every card swipe, mobile app interaction, customer service call, and branch visit generates information. The question becomes: how do you turn that data into competitive advantage?

Predictive analytics provides the answer. It enables personalization at scale, risk assessment in real-time, and operational efficiency that cuts costs while improving service.

Critical Use Cases Transforming Banking Operations

Predictive analytics isn’t theoretical. Banks are deploying these systems across core functions right now. Let’s look at the applications driving the most value.

Fraud Detection That Actually Works

Traditional fraud systems rely on rules. If a transaction exceeds $5,000 and occurs internationally, flag it. If someone makes three purchases within ten minutes, review it. The problem? Fraudsters know these rules and design attacks to evade them. Meanwhile, legitimate customers get blocked trying to buy a flight or make a large purchase.

Predictive fraud detection systems take a different approach. Machine learning models analyze hundreds of variables for each transaction—device fingerprints, location data, transaction velocity, merchant category, historical patterns, even typing rhythm on mobile devices. The system doesn’t look for rule violations. It looks for deviations from each customer’s normal behavior.

The results speak for themselves. Financial institutions using advanced AI-powered fraud detection have dramatically reduced false positives while catching sophisticated attacks that rule-based systems miss entirely.

Real talk: the technology isn’t perfect. Models require constant retraining as fraud patterns evolve. There’s also the challenge of explainability—regulators want to understand why a transaction was flagged, but complex neural networks operate as black boxes. Banks are working on this through hybrid approaches that combine model accuracy with rule-based transparency.

Credit Risk Assessment Beyond FICO Scores

Credit scoring has traditionally relied on a narrow set of factors. Payment history carries the heaviest weight at 35%, followed by credit utilization at 30%, credit history length at 15%, types of credit at 10%, and recent credit inquiries at 10%.

But here’s the limitation: these factors only capture part of the picture. Someone with a thin credit file—a recent immigrant, a young adult, someone recovering from bankruptcy—may be creditworthy but score poorly under traditional models.

Predictive analytics expands the dataset. Alternative data sources like rent payments, utility bills, cash flow patterns, education, and employment history provide additional signals. Machine learning models can identify relationships between these variables and default risk that traditional scoring misses.

Academic research using neural networks for credit prediction has demonstrated strong results. One study using a dataset of 10,000 records with 14 features achieved a 96.8% recall rate, with an AUC score of 0.91. The multi-layer perceptron architecture used 128 and 64 neurons in hidden layers to capture complex non-linear relationships.

The implications are significant. Better credit models mean more accurate risk pricing. Borrowers who would be rejected or charged premium rates under traditional scoring might qualify for standard rates. Meanwhile, applicants who look good on paper but carry hidden risks get appropriately priced.

Customer Churn Prediction and Prevention

Acquiring a new banking customer costs significantly more than retaining an existing one. Yet customer churn remains a persistent problem. Industry data suggests financial services experience roughly a 20% customer churn rate—one in five customers leaves within a given period.

Predictive models can identify at-risk customers before they leave. The approach combines multiple data sources: transaction frequency, product usage, customer service interactions, mobile app engagement, competitor research searches, and even social media sentiment.

Machine learning algorithms spot patterns that precede churn. Maybe it’s declining transaction volume. Perhaps it’s reduced mobile app logins. Or it could be increased balance inquiries suggesting someone is preparing to transfer funds elsewhere.

Once the model flags at-risk customers, banks can intervene. Targeted retention offers, proactive customer service outreach, personalized product recommendations—whatever the data suggests will be most effective for that particular customer.

The key is timing. Intervene too early and resources get wasted on customers who weren’t actually leaving. Wait too long and the customer has already made their decision. Predictive models help banks find that optimal intervention window.

Hyper-Personalized Product Recommendations

Generic marketing is dead. Customers expect banks to understand their needs and present relevant offers at the right moment.

Predictive analytics enables this personalization at scale. The system analyzes transaction patterns to understand each customer’s financial life. A customer with regular childcare payments might be interested in education savings accounts. Someone frequently traveling internationally could benefit from a premium credit card with no foreign transaction fees. A recent home buyer likely needs insurance products and home equity lines of credit.

Major financial firms are using AI to enhance customer support and optimize internal processes—many of these applications involve personalized service delivery and intelligent product matching.

The sophistication goes beyond simple pattern matching. Advanced systems use collaborative filtering—identifying customers with similar profiles and recommending products that worked well for comparable users. They incorporate timing models that predict when someone is most receptive to an offer. They even optimize channel selection, determining whether a particular customer responds better to email, mobile app notifications, or direct mail.

Compliance and Anti-Money Laundering

Regulatory compliance represents a massive cost center for banks. Anti-money laundering (AML) systems generate thousands of alerts that compliance teams must investigate manually. The majority turn out to be false positives, but each requires staff time to review.

Predictive analytics improves this process in two ways. First, machine learning models reduce false positives by learning what legitimate unusual activity looks like for each customer. Second, they prioritize alerts by risk level, ensuring compliance teams focus on the most suspicious cases first.

The regulatory environment is paying attention. In July 2023, the Securities and Exchange Commission proposed new rules requiring broker-dealers and investment advisers to address conflicts of interest associated with predictive data analytics.

This regulatory scrutiny reflects both the power and the risk of predictive systems. When algorithms make decisions that affect customers, regulators want assurance that those decisions are fair, transparent, and don’t create hidden conflicts of interest.

The Technology Stack Behind Predictive Banking

Implementing predictive analytics requires more than just data scientists. Banks need a complete technology infrastructure that can collect, process, analyze, and act on data at scale.

Data Infrastructure and Big Data Platforms

Predictive models are only as good as the data they’re trained on. Banks generate terabytes of information daily, but that data often sits in silos—core banking systems, card processing platforms, mobile apps, CRM systems, fraud detection tools, and more.

Modern data platforms solve this through centralized data lakes or warehouses. These systems aggregate information from disparate sources, clean and normalize it, and make it accessible for analysis. Cloud infrastructure has made this more feasible—instead of building massive on-premises data centers, banks can leverage elastic compute and storage from providers.

This infrastructure investment reflects the computing power required for advanced analytics as financial institutions and other industries scale their AI capabilities.

Machine Learning and AI Frameworks

The actual predictive models rely on machine learning frameworks and algorithms. Common approaches include:

- Logistic regression: Still widely used for binary classification problems like fraud detection or default prediction. Simple, interpretable, and effective for many banking applications.

- Random forests and gradient boosting: Ensemble methods that combine multiple decision trees. Excellent for structured data with complex non-linear relationships.

- Neural networks: Deep learning approaches that can capture extremely complex patterns. Used for image recognition (check processing), natural language processing (customer service), and sophisticated fraud detection.

- Support vector machines: Effective for classification tasks with clear margins between classes.

The choice of algorithm depends on the use case. Fraud detection often uses neural networks for their pattern recognition capabilities. Credit scoring might prefer gradient boosting for its balance of accuracy and interpretability. Customer segmentation could use clustering algorithms like k-means.

Real-Time Processing Capabilities

Many banking applications require real-time or near-real-time predictions. When someone swipes their card, the fraud detection system has milliseconds to evaluate the transaction and approve or decline it. Batch processing that runs overnight won’t cut it.

This requires stream processing infrastructure—systems that can ingest, process, and score transactions as they occur. Technologies like Apache Kafka for data streaming combined with frameworks that can serve machine learning models at low latency make this possible.

The architecture challenge is significant. Models need to be lightweight enough for fast inference while remaining accurate. They need to handle thousands or millions of predictions per second. And they need to do all this reliably, because downtime means transactions can’t be processed.

Model Governance and Monitoring

Deploying a model into production is just the beginning. Banks need systems to monitor model performance, detect drift, manage versioning, and ensure regulatory compliance.

Model drift happens when the statistical properties of the data change over time. A credit scoring model trained on pre-pandemic data might perform poorly after economic conditions shift. Monitoring systems track performance metrics and alert teams when accuracy degrades.

Governance includes documentation of model development, validation testing, bias audits, and regulatory reporting. When a regulator asks why a particular loan application was denied, the bank needs to explain the model’s decision process.

Implementation Challenges Banks Actually Face

Predictive analytics sounds great in theory. Implementation reveals complications that don’t appear in vendor presentations or conference talks.

Data Quality: The Persistent Problem

Machine learning models require clean, consistent, complete data. Banks rarely have this. Customer records might have duplicates. Transaction codes could be inconsistent across systems. Historical data might have gaps or errors.

Data cleaning consumes 60-80% of data science project time in many organizations. Before any modeling begins, teams must identify data quality issues, trace them to source systems, implement fixes, and build processes to prevent future problems.

Then there’s the integration challenge. Customer data lives in core banking. Transaction data comes from card processors. Mobile app interactions sit in separate analytics platforms. Web activity tracks through different tools. Bringing all this together requires significant engineering work.

Model Interpretability vs. Accuracy Trade-offs

The most accurate models—deep neural networks with dozens of layers—operate as black boxes. They make excellent predictions but can’t explain why.

Regulators don’t love black boxes. If a bank denies someone a loan, fair lending laws require explaining why. “The neural network said no” isn’t an acceptable answer.

This creates tension. Do you optimize for accuracy with complex models? Or do you prioritize interpretability with simpler approaches that may perform slightly worse?

Many banks split the difference. They use complex models where explainability isn’t critical (like internal forecasting) and simpler models for customer-facing decisions (like credit approvals). Others use hybrid approaches—complex models make the initial prediction, then interpretability layers explain the decision using simpler logic.

Talent Scarcity in Financial AI

Building and maintaining predictive analytics systems requires specialized skills. Data scientists who understand both machine learning and financial services are in short supply.

According to Federal Reserve data, about 10% of financial sector job listings mention AI-related skills. That’s higher than the 5% average across all sectors but still reflects a tight labor market. For comparison, the information sector sees AI skills mentioned in roughly 20% of job postings.

Banks compete for this talent against tech companies that often offer better compensation, more interesting problems, and fewer regulatory constraints. The result? Hiring challenges and retention difficulties.

Some institutions address this through partnerships with fintech firms or cloud providers that offer managed AI services. Others invest heavily in training existing staff. Neither approach completely solves the problem.

Regulatory Compliance Complexity

Financial services is among the most heavily regulated industries. Every predictive model must comply with fair lending laws, consumer protection regulations, data privacy requirements, and risk management standards.

The SEC’s 2023 proposed rules on conflicts of interest in predictive data analytics signal increasing scrutiny. Regulators worry that algorithms might optimize for bank profitability at customer expense—recommending products that generate high fees rather than products that best serve customer needs.

The Bank for International Settlements has highlighted financial stability concerns around AI adoption. When many institutions use similar models trained on similar data, there’s risk of herding behavior—everyone making the same decisions at the same time, potentially amplifying market volatility.

Navigating this regulatory landscape requires ongoing dialogue with regulators, robust governance processes, and sometimes accepting that the most profitable model isn’t the most compliant one.

Legacy System Integration

Most banks operate on technology infrastructure built over decades. Core banking systems might run on mainframes. Different business units use incompatible platforms. Modern predictive analytics needs to integrate with all of it.

API development, middleware, data transformation layers—these integration projects can take longer than building the models themselves. The challenge isn’t machine learning. It’s getting the model’s predictions into the systems where they’re needed and ensuring those systems can act on the recommendations.

Some banks address this through gradual modernization, building new capabilities alongside legacy systems. Others pursue full platform replacements, which carry enormous risk and cost. There’s no easy answer.

| Challenge | Impact Level | Primary Mitigation Strategy |

|---|---|---|

| Data Quality Issues | High | Dedicated data governance programs and automated validation |

| Model Interpretability | High | Hybrid approaches combining accuracy with explainability layers |

| Talent Scarcity | Medium | Partnerships with vendors, internal training programs |

| Regulatory Compliance | High | Robust governance, regular audits, regulator engagement |

| Legacy Integration | Medium | API-first architecture, gradual modernization |

| Model Drift | Medium | Continuous monitoring, automated retraining pipelines |

The Evolution Path: Where Predictive Banking Is Heading

The current state of predictive analytics in banking is impressive. The trajectory suggests even more significant changes ahead.

Foundation Models and Generative AI

Foundation models and generative AI systems are emerging applications in banking use cases. These are the large language models that have captured public attention.

Foundation models could transform customer service through more natural conversational interfaces. They might improve fraud detection by analyzing unstructured data like customer emails or social media. They could assist compliance teams by automatically reviewing contracts and regulatory filings.

But they also introduce new risks. Large language models can hallucinate—generating plausible-sounding but false information. They require massive computational resources. And their decision-making processes are even less transparent than traditional neural networks.

Banks are proceeding cautiously. Pilot programs test capabilities while risk management teams evaluate downsides. Adoption may progress gradually given the operational and regulatory complexities involved.

Federated Learning for Privacy-Preserving Analytics

Privacy regulations like GDPR limit how banks can share customer data. But collaborative analytics could improve fraud detection—if ten banks pooled their fraud data, models would be far more robust.

Federated learning offers a potential solution. Instead of sharing data, institutions share model updates. Each bank trains a model on its local data, then shares only the learned parameters. A central system aggregates these updates to improve a global model without ever seeing the underlying customer information.

This technology is still maturing, but pilot programs are underway in financial services. If successful, it could enable collaboration while maintaining privacy and regulatory compliance.

Embedded Analytics in Every Banking Process

Right now, predictive analytics often operates as a separate function—the data science team builds models, then hands them off to business units. The future embeds analytics directly into every process.

Loan officers would see real-time risk assessments within their application processing systems. Branch staff would receive next-best-action recommendations as they speak with customers. Treasury teams would get automated cash flow forecasts updated continuously.

This requires tighter integration between analytics and operational systems. It demands user interfaces that present predictions in context rather than requiring separate analytics dashboards. And it needs change management so staff trust and act on algorithmic recommendations.

Predictive Regulation and Compliance

Regulators themselves are beginning to use predictive analytics for supervision. Instead of scheduled examinations, supervisory systems might flag institutions showing early warning signs of trouble.

This creates an interesting dynamic. Banks use predictive models to comply with regulations. Regulators use predictive models to monitor banks. The interaction between these systems will shape the future regulatory landscape.

Some scenarios to watch: automated compliance reporting where banks’ systems directly feed regulators’ monitoring platforms; model registries that document every algorithm used in customer-facing decisions; and stress testing that includes AI system performance under adverse conditions.

Getting Started: Practical Steps for Banks

For institutions looking to implement or expand predictive analytics capabilities, the path forward requires careful planning.

Start With High-Value, Low-Complexity Use Cases

Don’t begin with the hardest problems. Identify applications where predictive analytics can deliver clear value without requiring complete system overhauls.

Fraud detection often works well as an initial project. The data is available, the business case is clear, and improvements deliver immediate measurable impact. Customer segmentation for marketing represents another good starting point—valuable insights without touching core transaction systems.

Build success stories. Early wins generate executive support and organizational momentum for more ambitious projects later.

Invest in Data Infrastructure First

Rushing to build models before data infrastructure is ready leads to frustration. Teams spend months wrestling with data integration instead of developing analytics.

Prioritize data quality programs, establish governance processes, and build the pipelines that make clean data accessible. This foundational work isn’t glamorous, but it’s essential.

Consider cloud platforms that provide managed data services. Building everything in-house works for large institutions with extensive IT resources. Smaller banks often benefit from leveraging vendor solutions that handle infrastructure complexity.

Build Teams With Domain Expertise

Data scientists need to understand banking, not just algorithms. A fraud detection model built by someone who doesn’t understand payment processing will miss critical nuances.

Either hire people with both skill sets or build teams that combine data science expertise with deep banking domain knowledge. The collaboration between these roles produces better results than either working alone.

Training matters too. Invest in programs that teach data scientists about financial services and teach banking professionals about data analytics. Cross-functional understanding improves outcomes.

Establish Governance Early

Model governance isn’t something to bolt on after deployment. Build it into the development process from the start.

Document everything—data sources, model architecture, training procedures, validation testing, performance metrics, known limitations. When regulators ask questions, having thorough documentation makes compliance straightforward.

Implement review processes. Models should undergo validation by teams independent from the developers. Bias audits should test for discriminatory outcomes. Risk assessments should evaluate what happens if the model fails.

Plan for Continuous Improvement

Deploying a model isn’t the end. It’s the beginning of an ongoing cycle of monitoring, evaluation, and refinement.

Build systems that track model performance in production. Set thresholds that trigger reviews when accuracy degrades. Establish retraining schedules that keep models current as data distributions shift.

Create feedback loops so business users can report when model predictions seem off. Their domain expertise often catches issues that automated monitoring misses.

Use Predictive Analytics to Detect Banking Risk and Fraud

Fraud patterns shift, customer behavior changes, and risk builds before it becomes visible in reports. AI Superior develops custom AI software that includes predictive analytics, helping banks analyze financial and behavioral data, forecast possible outcomes, and support decisions across fraud detection, risk assessment, and customer-related processes. Their approach combines historical and real-time data to reflect how financial activity evolves over time.

Apply Predictive Analytics in Daily Banking Decisions

AI Superior helps you:

- Work with risk patterns before they fully develop

- Make decisions based on evolving customer and transaction data

- Use predictive models within ongoing banking processes

To see how predictive analytics can be applied in your banking processes, contact AI Superior and discuss your use case.

Frequently Asked Questions

What is the difference between predictive analytics and traditional business intelligence in banking?

Traditional business intelligence looks backward, analyzing historical data to understand what happened and why. Dashboards might show last quarter’s loan volume or monthly fraud losses. Predictive analytics looks forward, using historical patterns to forecast what will happen next. Instead of reporting that fraud increased 10% last month, predictive systems identify which transactions are likely fraudulent before they’re approved. The shift is from descriptive to prescriptive—from reporting outcomes to shaping them.

How accurate are predictive models for credit scoring compared to traditional FICO scores?

Accuracy depends on implementation, but research demonstrates that machine learning models can achieve impressive performance. Studies using neural networks for credit prediction have reported recall rates as high as 96.8% with AUC scores of 0.91 using datasets with 14 features and 10,000 records. These models often outperform traditional scoring, especially for populations with thin credit files, because they can incorporate alternative data sources. However, the improvement varies by use case and data quality. Traditional scores remain valuable for their standardization and regulatory acceptance.

What are the main regulatory concerns around AI in banking?

Regulators focus on several key issues. First, fairness and bias—algorithms must not discriminate based on protected characteristics. Second, transparency and explainability—banks need to explain decisions made by AI systems, especially for credit denials. Third, conflicts of interest—the SEC’s 2023 proposed rules specifically address concerns that predictive analytics might optimize for firm profitability rather than customer benefit. Fourth, systemic risk—if many institutions use similar models, correlated behavior could amplify financial stability risks. Finally, operational resilience—AI systems must be robust, secure, and recoverable if they fail.

How long does it typically take to implement a predictive analytics system in a bank?

Implementation timelines vary dramatically based on scope and complexity. A focused use case like fraud detection for a specific payment channel might take 3-6 months from project kickoff to production deployment. Enterprise-wide implementations touching multiple systems and processes often require 12-24 months or longer. The longest phases are typically data integration and infrastructure setup rather than model development itself. Banks with mature data platforms and governance processes move faster than those building foundation capabilities from scratch.

Can small and mid-sized banks implement predictive analytics, or is it only feasible for large institutions?

Smaller institutions absolutely can implement predictive analytics, though the approach differs from large banks. Cloud-based platforms and vendor solutions have democratized access to advanced analytics capabilities. Instead of building everything in-house, smaller banks can leverage managed services that provide pre-built models for common use cases like fraud detection or customer churn prediction. The key is starting with targeted applications that deliver clear ROI rather than attempting comprehensive transformation. Many fintech partnerships and banking-as-a-service platforms now include embedded analytics, making sophisticated capabilities accessible regardless of institution size.

What skills do banks need to hire for building predictive analytics capabilities?

Successful predictive analytics teams combine multiple skill sets. Data scientists bring expertise in statistics, machine learning algorithms, and programming languages like Python or R. Data engineers build the infrastructure for collecting, cleaning, and processing data at scale. ML engineers specialize in deploying models into production systems and maintaining them. Banking domain experts ensure models address real business problems and comply with regulations. Product managers translate business needs into analytics requirements. According to Federal Reserve data, approximately 10% of financial sector job postings now mention AI-related skills, reflecting the growing demand for these capabilities.

How do banks address the black box problem with complex AI models?

Banks use several strategies to balance model accuracy with explainability. Some implement hybrid architectures where a complex neural network makes the initial prediction, then a simpler interpretable model approximates that decision in human-understandable terms. Others use SHAP values or LIME techniques that explain individual predictions by showing which features contributed most to the outcome. For customer-facing decisions like lending, many institutions opt for inherently interpretable models like logistic regression or decision trees, accepting slightly lower accuracy for regulatory compliance. Model documentation, validation testing, and bias audits provide additional layers of transparency that help address regulator concerns even when the underlying algorithms are complex.

The Competitive Imperative

Predictive analytics has moved from experimental to essential. The gap between institutions that effectively leverage these capabilities and those that don’t will only widen.

Banks that excel at predictive analytics will offer better customer experiences through personalization. They’ll manage risk more effectively through earlier identification of problems. They’ll operate more efficiently by automating decisions that currently require manual review. And they’ll prevent fraud more successfully by adapting faster than criminals.

Technology continues to evolve. Foundation models, federated learning, embedded analytics—these advances will expand what’s possible. But the fundamentals remain constant: clean data, appropriate algorithms, robust governance, and teams that understand both banking and analytics.

For financial institutions, the question isn’t whether to invest in predictive analytics. The 75% adoption rate among major firms makes clear that this ship has sailed. The question is how quickly and effectively to implement these capabilities before competitive disadvantage becomes insurmountable.

The banks that started this journey years ago are already seeing results—billions in preventing fraud, reduced credit losses, improved customer retention, and operational efficiencies. Those still getting started face an uphill climb, but the path is well-established.

Start with clear use cases. Build solid data foundations. Hire the right talent or partner with the right vendors. Establish governance that satisfies regulators. Monitor, measure, and continuously improve.

The predictive future of banking is here. Time to build the capabilities that will define success in that future.