Quick Summary: Predictive analytics in fintech leverages AI and machine learning to forecast financial trends, assess credit risk, detect fraud, and personalize customer experiences. According to authoritative sources, AI-driven predictive analytics increases fraud detection accuracy by 40% and improves forecast accuracy by 55% compared to traditional methods. Financial institutions use these tools for credit scoring, market forecasting, churn prediction, and real-time risk management—transforming reactive banking into proactive, data-driven decision-making.

Financial institutions no longer wait for problems to surface. They predict them.

In 2026, predictive analytics has become the nervous system of modern fintech—processing millions of data points in real time, identifying fraud before it happens, and offering credit to underserved populations who’d never pass a traditional scorecard. The question isn’t whether your competitors are using predictive models. It’s how far ahead they’ve gotten.

Here’s the thing though—predictive analytics isn’t magic. It’s a combination of historical data, machine learning algorithms, and real-time behavioral signals that together forecast outcomes with remarkable accuracy. Studies show AI-driven predictive analytics significantly enhances fraud detection capabilities, with research demonstrating a 40% increase in accuracy over traditional methods. Market forecasting improvements have been documented in peer-reviewed research., according to peer-reviewed research.

So what does that actually look like in practice? And more importantly, how can financial services firms implement these models without stumbling over the same pitfalls that derail 40% of AI initiatives during the exploration phase?

Let’s break it down.

What Predictive Analytics Really Means for Fintech

Predictive analytics uses statistical algorithms and machine learning techniques to analyze historical and real-time data, then forecast future events. In fintech, that translates to answering questions like: Will this borrower default? Is this transaction fraudulent? Which customers are about to churn?

Traditional financial models relied on rigid rules and backward-looking indicators. Credit scores, for instance, penalized anyone without a lengthy credit history—locking out millions of creditworthy individuals. Fraud detection systems flagged transactions based on static thresholds, missing sophisticated attacks and annoying legitimate customers with false positives.

Machine learning changes the game. Models trained on massive datasets identify patterns humans miss. They adapt as new data flows in. And they operate at speeds traditional systems can’t match.

The Bank for International Settlements noted in a November 2025 keynote that machine learning and artificial intelligence offer new opportunities to predict market stress and dysfunction, overcoming the limitations of traditional econometric models. Central banks and regulators now use these tools to monitor financial stability in real time.

That’s not some distant future. It’s happening right now across credit scoring, fraud prevention, investment forecasting, and customer retention.

Apply Predictive Analytics in Fintech with AI Superior

AI Superior builds predictive models for financial data to support decision-making, risk assessment, and process automation.

They focus on models that fit into existing systems and can be used reliably in production environments.

Looking to Use Predictive Analytics in Fintech?

AI Superior can help with:

- evaluating financial data

- building predictive models

- integrating models into existing systems

- refining performance over time

👉 Contact AI Superior to discuss your project, data, and implementation approach

Why Fintech Firms Are Betting Big on Predictive Models

The numbers tell the story. AI-related job postings in the financial sector now account for roughly 18% of all listings, according to Federal Reserve labor market analysis. Compare that to 12% across all industries, and it’s clear where the momentum sits.

Financial institutions adopt predictive analytics for four core reasons:

Risk Reduction

Lending decisions become more accurate when models analyze thousands of variables—transaction history, spending patterns, social signals, even time-of-day behaviors. Credit risk drops. Default rates fall. Profitability climbs.

Operational Efficiency

Manual underwriting takes days. AI-powered credit scoring happens in seconds. Fraud analysts can’t review every transaction. Machine learning models screen millions per hour, escalating only the genuine threats.

Customer Experience

Personalization at scale wasn’t possible before. Now predictive models segment users into micro-cohorts, tailoring product recommendations, pricing, and messaging to individual preferences. The result? Higher conversion rates and deeper engagement.

Competitive Advantage

When a challenger bank approves loans in 60 seconds while incumbents need three days, customers switch. Speed and accuracy become the moat. Firms that master predictive analytics pull ahead—and stay there.

Credit Scoring Reimagined: Beyond FICO

Traditional credit scores paint an incomplete picture. FICO models weigh payment history, credit utilization, and account age—all backward-looking metrics that exclude anyone new to credit or recently immigrated.

Predictive analytics flips the script. Alternative data sources—rent payments, utility bills, mobile phone usage, even social media activity—feed machine learning models that assess creditworthiness without traditional credit histories.

The impact? Millions of previously “unscorable” consumers gain access to loans, credit cards, and financial services. Lenders reduce risk while expanding their addressable market. Analysis from case studies found AI-driven insights improved revenue forecasting by 45% by identifying at-risk accounts early enough to intervene.

How Alternative Credit Scoring Works

Models ingest structured data (bank transactions, bill payments) and unstructured signals (app usage patterns, geolocation stability). Algorithms identify correlations between behaviors and repayment likelihood. The system assigns a risk score in real time.

But here’s where it gets tricky. Bias can creep in. If training data reflects historical discrimination, models perpetuate it. Regulators and academic institutions have published extensive guidance on AI fairness in finance, emphasizing the need for explainability and bias testing.

Responsible fintech firms now implement explainable AI frameworks—ensuring every credit decision can be traced back to specific, defensible factors. The Federal Reserve highlighted this challenge in multiple 2025 speeches on AI governance, noting that transparency and accountability remain critical as adoption accelerates.

| Scoring Method | Data Sources | Speed | Inclusivity |

|---|---|---|---|

| Traditional FICO | Credit bureaus, loan history | Days | Excludes thin-file users |

| AI-Powered Alternative | Bank data, utilities, mobile, rent | Seconds | Includes underserved segments |

| Hybrid Model | Traditional + alternative signals | Minutes | Balanced risk and reach |

Fraud Detection That Actually Keeps Up

Fraudsters adapt faster than rule-based systems. They probe for weaknesses, find patterns that slip past static thresholds, and exploit them at scale. By the time compliance teams spot the new tactic, millions are gone.

Predictive analytics changes the dynamic. Machine learning models trained on billions of transactions recognize anomalies in real time—flagging suspicious activity the moment it deviates from expected behavior.

Academic research demonstrates AI-driven predictive analytics significantly enhances fraud detection capabilities, with studies showing a 40% increase in accuracy over conventional methods. That’s not incremental. That’s transformational.

Real-Time Behavioral Modeling

Modern fraud systems don’t just check transaction amounts or merchant categories. They build behavioral profiles for every user—tracking spending velocity, device fingerprints, geolocation patterns, and interaction timings.

When a transaction breaks the profile, the system flags it instantly. A user who normally shops in New York suddenly makes a purchase in Lagos? Could be fraud. But maybe they’re traveling. The model cross-references flight bookings, location history, and notification responses before deciding.

This layered approach reduces false positives—one of the biggest pain points in fraud prevention. Legitimate customers stop getting blocked. Fraud analysts focus on genuine threats. Everyone wins.

Market Forecasting and Investment Intelligence

Predicting market movements has always been part art, part science. Traders analyze fundamentals, technicals, sentiment—but human cognition has limits. Markets process information faster than analysts can react.

Enter predictive analytics. Machine learning models ingest news feeds, earnings reports, social media sentiment, macroeconomic indicators, and historical price data—then forecast likely movements with measurably better accuracy than traditional econometric approaches.

The Bank for International Settlements noted that machine learning offers new opportunities to predict market stress and dysfunction, overcoming the limitations of models that rely solely on linear relationships and static assumptions.

Robo-Advisors and Automated Wealth Management

Robo-advisors use predictive models to manage portfolios at scale. They assess risk tolerance, forecast market conditions, and rebalance holdings—all without human intervention. The result: institutional-grade wealth management accessible to retail investors at a fraction of traditional advisory fees.

Performance improves, too. Research in competitor sources indicates market trend forecasting using AI improves investment decisions by 35%, reducing drawdowns and capturing upside more consistently than passive strategies.

But automation introduces new risks. Models trained on historical data may fail when market regimes shift. Black swan events—pandemics, geopolitical shocks, sudden regulatory changes—lie outside typical training sets. Responsible firms layer human oversight and stress testing on top of algorithmic decision-making.

Churn Prediction and Customer Retention

Acquiring a new customer costs 5–7 times more than retaining an existing one. Yet most fintech firms don’t know a customer is leaving until they’re gone.

Predictive analytics changes that. Models analyze engagement signals—login frequency, transaction volume, support tickets, feature usage—to identify at-risk customers weeks before they churn.

Real-world implementations show churn prediction enables proactive retention, with implementations reporting savings of 25–40% of at-risk customers through targeted interventions. A personalized offer, a timely support call, or a product recommendation can flip the script.

How Churn Models Work

Historical data trains the model on what disengagement looks like. Common signals include declining transaction frequency, fewer logins, increased support complaints, or exploration of competitor products.

Once the model identifies an at-risk user, automated workflows trigger retention campaigns—discounts, feature tutorials, account reviews. The highest-risk customers get flagged for human outreach.

One fintech platform analyzed booking patterns and cancellation behaviors, predicting cancellation risks with enough lead time to optimize pricing and improve booking reliability. The outcome: reported improvements including 20% increase in revenue predictability and 30% reduction in late-stage cancellations.

Implementing Predictive Analytics: The Reality Check

Theory sounds great. Implementation? That’s where most projects stall.

According to Federal Reserve research, 40% of enterprises remain in exploration and experimentation phases of AI adoption. They pilot models, see promising results, then struggle to scale into production.

Why? Data quality issues, organizational resistance, lack of AI talent, and regulatory uncertainty all play a role.

Data Quality Is Non-Negotiable

Garbage in, garbage out. Predictive models are only as good as the data feeding them. Incomplete records, inconsistent formats, and siloed systems torpedo accuracy.

Successful implementations start with data infrastructure—centralized data lakes, clean ETL pipelines, and governance frameworks that ensure consistency across sources.

Regulatory Compliance and Explainability

Regulators demand transparency. A black-box model that denies credit or flags fraud without explanation won’t fly. Fintech firms must implement explainable AI techniques—SHAP values, LIME, or attention mechanisms—that trace predictions back to specific input features.

The Bank for International Settlements and Federal Reserve have both published extensive guidance on AI regulation in financial services, emphasizing risk management, bias testing, and consumer protection as non-negotiable requirements.

Talent and Organizational Readiness

Building and maintaining predictive models requires data scientists, ML engineers, and domain experts who understand finance. According to Federal Reserve labor market analysis, roughly 1 in 10 job postings in the financial sector mention AI-related skills—a clear signal of the talent crunch.

Firms that can’t hire in-house often partner with specialized vendors or invest in upskilling existing teams. Either way, organizational buy-in is critical. Executives, compliance officers, and front-line staff all need to understand what models do and don’t do.

| Challenge | Impact on Implementation | Solution Approach |

|---|---|---|

| Data Quality | Inaccurate predictions, model drift | Centralized data lakes, governance frameworks |

| Regulatory Compliance | Legal risk, fines, deployment delays | Explainable AI, bias testing, audit trails |

| Talent Shortage | Slow development, poor model performance | Upskilling programs, vendor partnerships |

| Organizational Resistance | Low adoption, siloed initiatives | Executive sponsorship, cross-functional teams |

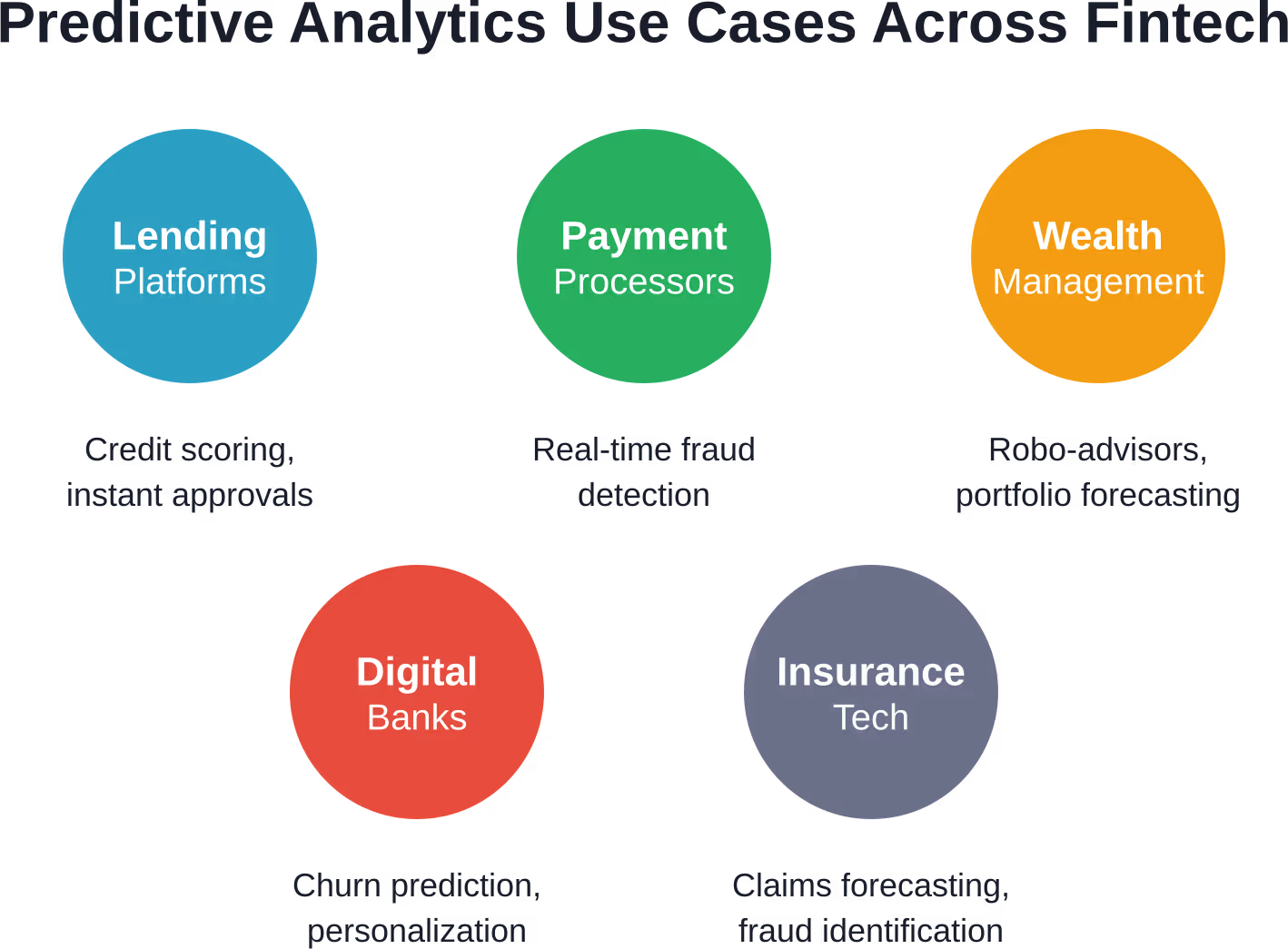

Real-World Use Cases Across Fintech

Abstract concepts matter less than concrete results. Here’s how predictive analytics plays out across different fintech verticals:

Lending Platforms

AI-powered underwriting approves loans in under a minute, analyzing hundreds of alternative data points to assess risk. Default rates drop. Approval rates for thin-file borrowers climb. Revenue grows.

Payment Processors

Real-time fraud detection screens every transaction against behavioral profiles, blocking suspicious activity before funds move. Chargebacks fall. Merchant satisfaction rises. Compliance costs shrink.

Wealth Management Apps

Robo-advisors tailor portfolios to individual risk profiles, rebalancing automatically based on market forecasts. Users get institutional-grade strategies at consumer-friendly fees.

Digital Banks

Churn prediction models flag at-risk customers, triggering personalized retention campaigns. Customer lifetime value increases. Acquisition costs justify themselves faster.

Insurance Tech

Predictive models assess claim likelihood, pricing policies more accurately and identifying fraud during submission rather than after payout.

The Data Explosion Fueling Predictive Models

None of this works without data. Lots of it.

Federal Reserve research noted that Federal Reserve research noted that in 2013, roughly 90 percent of the world’s data had been created in the prior two years, and by 2016 this acceleration continued with the vast majority of data created in recent periods. That acceleration continues—data generation doubles every 12–18 months.

More data means better models. Machine learning thrives on volume and variety. The more transactions, behaviors, and signals available, the more accurate predictions become.

But scale introduces complexity. Processing millions of events per second requires robust infrastructure—cloud platforms, distributed databases, and streaming analytics frameworks. Organizations without robust data infrastructure and technical capabilities struggle to operationalize models effectively, regardless of algorithmic sophistication.

Model Drift and Continuous Learning

Markets shift. Customer behaviors evolve. What worked last year may fail tomorrow.

Predictive models suffer from drift—gradual degradation in accuracy as the real world diverges from training data. A credit model trained on pre-pandemic data might underperform post-pandemic. A fraud system tuned for desktop transactions could miss mobile-first attack vectors.

The solution? Continuous learning. Modern pipelines retrain models regularly, incorporating fresh data and adapting to new patterns. Monitoring systems track performance metrics—accuracy, precision, recall—and alert teams when drift exceeds acceptable thresholds.

This requires operational discipline. Data scientists can’t just build models and walk away. MLOps practices—versioning, testing, deployment automation—ensure models stay current and reliable in production.

Ethical Considerations and Bias Mitigation

Predictive models encode the biases present in training data. If historical lending decisions discriminated against certain demographics, a model trained on that data will perpetuate the bias—possibly at scale.

Regulatory bodies and academic institutions have sounded the alarm. Academic research and regulatory guidance on AI fairness in finance emphasize the need for bias testing, diverse training sets, and transparent decision-making.

Responsible fintech firms now implement fairness audits—testing models across demographic groups to ensure equitable outcomes. Techniques like adversarial debiasing and fairness constraints during training help mitigate systematic discrimination.

But technical fixes aren’t enough. Organizations need diverse teams, inclusive design processes, and accountability mechanisms that prioritize fairness alongside profitability.

The Role of Generative AI in Fintech Analytics

Generative AI—large language models, synthetic data generation, and multimodal systems—adds a new layer to predictive analytics.

Chatbots powered by generative models handle customer inquiries, extracting insights from unstructured conversations that feed predictive systems. Synthetic data generation augments small or imbalanced datasets, improving model performance without compromising privacy.

The Bank for International Settlements published guidance on AI in the financial sector, including a December 2024 report on regulating AI, noting that generative AI adoption is accelerating across banking and insurance, with implications for risk management, customer experience, and operational efficiency.

One example: a generative model trained on millions of support tickets can predict which customers are likely to escalate complaints, enabling preemptive intervention. Another: synthetic transaction data helps train fraud models without exposing real customer information.

But generative AI introduces new risks—hallucinations, biased outputs, and adversarial attacks. Fintech firms must validate generated content rigorously and layer human oversight on automated processes.

Regulatory Landscape and Compliance Challenges

Regulators worldwide are racing to keep pace with AI adoption in finance. Regulatory bodies including the Bank for International Settlements and Federal Reserve have published guidance emphasizing transparency, risk management, and consumer protection.

Key themes include:

- Explainability: Financial institutions must be able to explain how models make decisions, especially when those decisions affect credit access or fraud allegations.

- Bias Testing: Models must be audited for disparate impact across protected classes.

- Data Privacy: GDPR, CCPA, and similar regulations impose strict requirements on data collection, storage, and usage.

- Model Governance: Institutions need documentation, version control, and audit trails for all production models.

Non-compliance carries real consequences—fines, reputational damage, and restrictions on operations. Firms that treat regulation as an afterthought risk expensive setbacks.

What’s Next: Prescriptive Analytics and Autonomous Finance

Predictive analytics tells you what will happen. Prescriptive analytics tells you what to do about it.

The next frontier combines prediction with optimization—recommending specific actions to achieve desired outcomes. A churn model doesn’t just flag at-risk customers; it suggests the best retention offer for each individual. A credit model doesn’t just assess risk; it proposes alternative loan structures that balance profitability and approval rates.

Fully autonomous finance—systems that make decisions without human intervention—remains years away for most applications. Regulatory concerns, liability questions, and ethical considerations slow adoption.

But the trajectory is clear. As models improve, as infrastructure scales, and as governance frameworks mature, more decisions will shift from human judgment to algorithmic execution. The firms building those capabilities today will define the competitive landscape tomorrow.

Frequently Asked Questions

How accurate are predictive analytics models in fintech?

Accuracy varies by application and data quality. Authoritative research shows AI-driven predictive analytics increases fraud detection accuracy by 40% and improves forecast accuracy for market trends by 55% compared to traditional methods. Credit scoring models typically achieve 85–90% accuracy in real-world deployments, though performance depends on the richness of alternative data sources and the sophistication of the model architecture.

What data sources do fintech predictive models use?

Models ingest structured data like bank transactions, payment histories, and credit bureau reports, plus alternative signals including utility bills, rent payments, mobile phone usage, social media activity, device fingerprints, geolocation patterns, and behavioral metrics like login frequency and session duration. The broader the data mix, the more accurate the predictions—assuming proper governance and privacy compliance.

Can predictive analytics replace human decision-making in finance?

Not entirely. Models excel at processing large datasets and identifying patterns humans miss, but they lack contextual judgment, ethical reasoning, and the ability to handle edge cases outside training data. Best practice combines algorithmic prediction with human oversight—especially for high-stakes decisions like loan approvals, fraud investigations, and regulatory compliance. The most effective systems augment human expertise rather than replace it.

How do fintech firms prevent bias in predictive models?

Responsible firms implement fairness audits, testing models across demographic groups to detect disparate impact. Techniques include diverse training sets, adversarial debiasing algorithms, fairness constraints during optimization, and explainable AI frameworks that trace decisions back to specific features. Regulatory guidance from the Federal Reserve and Bank for International Settlements emphasizes transparency, accountability, and regular bias testing as non-negotiable requirements.

What’s the difference between predictive and prescriptive analytics?

Predictive analytics forecasts what will happen—this customer will churn, that loan will default, this transaction is fraudulent. Prescriptive analytics goes further, recommending specific actions to achieve desired outcomes—offer this discount to retain the customer, approve the loan with these terms, block the transaction and notify the user. Prescriptive systems combine prediction models with optimization algorithms that evaluate multiple scenarios and suggest the best course of action.

How long does it take to implement predictive analytics in a fintech company?

Timelines vary widely based on data infrastructure, organizational readiness, and model complexity. Simple use cases like churn prediction can reach production in 8–12 weeks if clean data and technical talent are available. Complex applications like alternative credit scoring or real-time fraud detection often require 6–12 months, factoring in data integration, model development, regulatory review, and testing. Federal Reserve analysis notes that 18% of enterprises remain stuck in experimentation phases, suggesting implementation challenges are common and timelines frequently stretch.

Do predictive models work for small fintech startups or only large institutions?

Both can benefit, though approaches differ. Large institutions build custom models in-house, leveraging massive proprietary datasets and dedicated data science teams. Startups often use pre-built solutions from cloud providers—AWS SageMaker, Google Vertex AI, Azure ML—or partner with specialized vendors. Pre-trained models via developer-friendly APIs have democratized access, allowing even small teams to deploy sophisticated predictive capabilities without deep ML expertise. The key constraint is data quality and volume, not organization size.

Conclusion: From Prediction to Action

Predictive analytics isn’t a futuristic concept anymore. It’s the operating system of competitive fintech in 2026.

The firms pulling ahead—approving loans in seconds, blocking fraud before it lands, retaining customers proactively, and forecasting markets with measurably better accuracy—have moved past experimentation. They’ve invested in data infrastructure, hired or trained the right talent, built governance frameworks that satisfy regulators, and integrated predictive models into every corner of their operations.

The data is clear. AI-driven predictive analytics increases fraud detection accuracy by 40%. It improves forecast accuracy by 55%. It saves 25–40% of at-risk customers through churn prediction. And it unlocks financial services for millions previously excluded by outdated credit models.

But getting there requires more than spinning up a machine learning model. It demands clean data, continuous learning pipelines, explainability frameworks, bias testing, and organizational buy-in from executives to front-line staff.

The opportunity is enormous. The competitive gap is widening. And the technology is more accessible than ever.

So the question isn’t whether predictive analytics will transform your business. It’s whether you’ll lead the transformation or watch competitors pull ahead.

Ready to start building? Focus on data quality first, pick one high-impact use case, and prove the value before scaling. The models are ready. The infrastructure exists. The talent is out there.

All that’s missing is the decision to begin.