Quick Summary: Machine learning transforms banking through fraud detection, risk management, personalized services, and operational automation. Banks deploy ML models to analyze transaction patterns in real-time, assess credit risk more accurately, and reduce false positives in anti-money laundering systems. Federal Reserve data shows ML-driven fraud prevention recovered $4 billion in fiscal year 2024, while industry adoption continues accelerating with banks increasingly implementing agentic AI solutions.

Banking institutions face unprecedented pressure to process massive transaction volumes, detect sophisticated fraud schemes, and deliver personalized customer experiences—all while maintaining regulatory compliance. Machine learning has emerged as the solution to these challenges.

The technology isn’t speculative anymore. It’s operational infrastructure powering the financial sector’s most critical functions.

According to the Federal Reserve, ML and AI tools enabled fraud prevention and recovery totaling $4 billion in fiscal year 2024. That’s not hype. That’s a measurable impact on bank balance sheets and customer protection.

But here’s the thing—machine learning adoption in banking extends far beyond fraud detection. The applications span risk assessment, customer service automation, trading algorithms, regulatory compliance, and operational efficiency. Each application solves specific problems that traditional rule-based systems can’t handle at scale.

Why Machine Learning Matters for Financial Institutions

Traditional banking systems rely on predetermined rules. If the transaction amount exceeds X, flag it. If a customer hasn’t made payment in Y days, send a reminder. These rules work until they don’t.

The limitations become obvious at scale. Rule-based fraud detection generates false positives that frustrate customers. Static credit scoring models miss nuanced risk patterns. Manual compliance reviews can’t keep pace with transaction volumes.

Machine learning models learn patterns from historical data rather than following rigid rules. They identify subtle correlations that humans miss. They adapt as fraud tactics evolve. They process millions of data points in milliseconds.

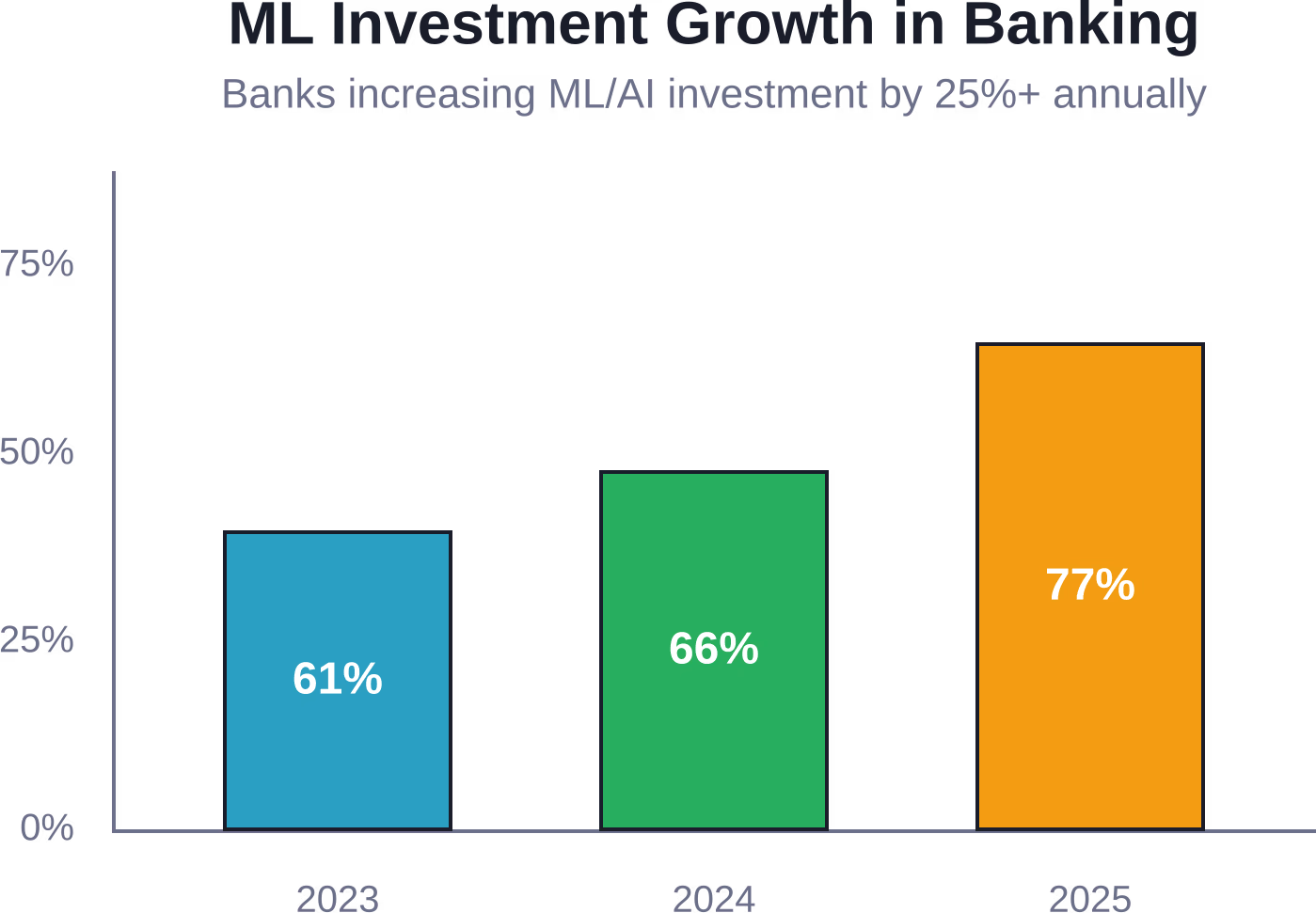

Industry data shows adoption rates rising from 61% in 2023 to 77% in 2025. Of those implementations, 16% represent fully deployed solutions while 52% remain in pilot projects. The adoption curve is accelerating, not theoretical.

Real talk: banks that don’t deploy ML capabilities will struggle to compete on fraud prevention, customer experience, and operational costs. The technology has moved from competitive advantage to operational necessity.

Upgrade Banking Workflows with Advanced ML Systems

Banks and financial teams process large amounts of operational and transactional data every day, but turning that data into useful insights often requires more than standard automation tools. AI Superior helps companies develop machine learning systems for predictive analytics, operational optimization, AI-driven data analysis, and scalable business automation.

Need AI Support for Banking Data and Operations?

AI Superior supports organizations with:

- Predictive analytics and behavioral pattern analysis

- AI systems for processing large operational datasets

- Machine learning PoC and prototype development

- Integration of AI solutions into existing business environments

👉Contact AI Superior to discuss machine learning solutions for banking operations, analytics, and internal workflows.

Fraud Detection and Prevention

Check fraud alone generated over 15,000 reports received between February and August 2023, representing $688 million in transaction value. Those numbers come from the Financial Crimes Enforcement Network via Federal Reserve reporting.

Machine learning models detect fraud by analyzing transaction patterns across multiple dimensions: amount, location, merchant category, time of day, device fingerprint, behavioral biometrics, and historical customer patterns. When anomalies appear, the system flags them instantly.

HSBC, using Google Cloud’s AML AI, cut the number of alerts by more than 60% while finding 2–4 times more confirmed suspicious activity.

That 60% false positive reduction matters enormously. Every false positive requires human investigation, wastes analyst time, and potentially frustrates legitimate customers whose transactions get blocked unnecessarily. Machine learning delivers precision that rule-based systems can’t match.

The models continuously improve. Each confirmed fraud case and each false positive feeds back into training data. The system learns what genuine fraud looks like in current conditions, not just historical patterns.

Credit Risk Assessment and Lending Decisions

Traditional credit scoring relies on limited variables: payment history, credit utilization, length of credit history, types of credit, recent inquiries. Machine learning models incorporate hundreds of additional data points.

Alternative data sources include bank account transaction patterns, utility payment history, rental payment records, employment stability indicators, and behavioral patterns. The models identify creditworthy borrowers that traditional FICO scores would reject.

DBS Bank deployed ML-driven early warning systems that proactively identify credit risks among small and medium enterprises. In 2022, the system successfully identified over 95% of non-performing SME loans at least three months before businesses experienced actual defaults.

Three months of advance warning changes everything. Banks can work with struggling businesses to restructure loans, adjust terms, or implement support measures before problems become unrecoverable. That’s risk management, not just risk assessment.

But wait. There’s a regulatory dimension here too. Machine learning credit models must provide explainability. Banks can’t deploy opaque neural networks that deny loans without justification. Every decision requires documentation showing which factors influenced the outcome.

Model interpretability techniques like SHAP values and LIME explanations break down complex ML decisions into understandable components. Regulators can audit these explanations to ensure models don’t perpetuate historical biases or discriminate against protected classes.

Anti-Money Laundering and Regulatory Compliance

Money laundering schemes adapt faster than rule-based detection systems. Criminals structure transactions to stay below reporting thresholds. They move funds through complex networks of accounts. They exploit timing gaps between institutions.

Machine learning models analyze transaction networks to identify suspicious patterns that individual transaction rules miss. They detect structuring behavior, circular fund flows, unusual beneficiary relationships, and geographic anomalies.

| Compliance Application | Traditional Approach | ML-Enhanced Approach | Impact |

|---|---|---|---|

| Transaction Monitoring | Rule-based thresholds | Behavioral pattern analysis | 60% fewer false positives |

| Customer Due Diligence | Manual document review | Automated risk scoring | 75% faster onboarding |

| Sanctions Screening | Name matching algorithms | Entity resolution ML | 40% more accurate matches |

| Suspicious Activity Reports | Case-by-case analyst review | Prioritization algorithms | 3x investigation efficiency |

The efficiency gains from ML-driven compliance aren’t just cost savings. They represent better protection against financial crime. When analysts spend less time investigating false positives, they can focus on genuine threats.

Regulatory technology (RegTech) platforms now incorporate ML models for reporting automation, regulatory change management, and audit trail documentation. These systems track which regulations apply to which transactions, automatically generate required reports, and flag potential compliance gaps.

Customer Service and Personalization

Chatbots represent the visible face of ML in banking customer service, but the technology runs much deeper. Recommendation engines suggest relevant financial products. Predictive models identify customers likely to need specific services. Natural language processing analyzes customer inquiries to route them to appropriate specialists.

Capital One has deployed machine learning across customer-facing systems to detect unusual charges, answer real-time questions, and provide proactive alerts. The ML implementation continues expanding, with leadership estimating they’re approximately 10% complete with planned deployments.

That 10% figure is revealing. Even leading institutions with extensive ML investments consider themselves in early stages. The potential applications far exceed current implementations.

Personalization engines analyze individual customer behavior to optimize communication timing, channel preferences, product recommendations, and service delivery. Instead of generic mass marketing, banks deliver relevant offers when customers are most receptive.

Voice recognition and natural language processing enable conversational interfaces that understand context, handle complex requests, and escalate appropriately to human agents when needed. The systems learn from each interaction to improve response accuracy.

Trading and Investment Management

Algorithmic trading systems have used quantitative models for decades, but machine learning brings adaptive capabilities that traditional algorithms lack. ML trading models identify market regime changes, adjust strategies dynamically, and incorporate alternative data sources.

BlackRock’s Aladdin platform processes vast amounts of market data and regulatory information, condensing insights into concise reports that assist financial advisors. The system combines risk analytics, portfolio construction, and trading execution with ML-driven pattern recognition.

Sentiment analysis models extract market-moving signals from news articles, social media, earnings call transcripts, and regulatory filings. These unstructured data sources provide information that price and volume data alone can’t capture.

Portfolio optimization algorithms balance expected returns against risk constraints, transaction costs, tax implications, and investor preferences. Machine learning improves return forecasts by identifying complex relationships between assets, economic indicators, and market conditions.

Robo-advisors democratize access to algorithmic portfolio management. ML models power the asset allocation, rebalancing, tax-loss harvesting, and goal-tracking features that retail investors receive at low costs.

Operational Efficiency and Automation

Back-office banking operations involve massive document processing, data entry, reconciliation, and reporting tasks. Machine learning automation handles these workflows faster and more accurately than manual processes.

Optical character recognition combined with natural language processing extracts data from loan applications, account opening forms, identity documents, and financial statements. The systems validate extracted information against databases and flag inconsistencies for human review.

Process automation extends to loan origination, account reconciliation, regulatory reporting, and customer onboarding. ML models route tasks to appropriate processors, predict processing times, and optimize workflow sequences to minimize bottlenecks.

Predictive maintenance for ATMs and banking infrastructure uses sensor data to identify equipment likely to fail. Preemptive repairs reduce downtime and improve customer experience while lowering maintenance costs.

Workforce planning models forecast transaction volumes, call center demand, and branch traffic to optimize staffing levels. The systems account for seasonality, economic conditions, product launches, and external events that influence banking activity.

Current Adoption Trends and Investment Patterns

The data shows clear acceleration in ML adoption across banking institutions. Survey findings indicate 50% of respondents increased their ML and AI investments by more than 25% from 2023 to 2024.

That investment growth continues. Additional survey data shows adoption of AI applications increased from 61% in 2023 to 77% in 2025. The trajectory points toward ML becoming standard infrastructure rather than experimental technology.

Look—not all adoption represents production deployment. Of banking organizations using agentic AI, only 16% have fully deployed solutions while 52% operate pilot projects. That gap between pilots and production reflects the complexity of implementing ML at banking scale.

Regulatory uncertainty remains a constraint. Banks need clarity on model governance requirements, explainability standards, and liability frameworks before deploying ML in high-stakes decision systems. Federal Reserve guidance on AI programs emphasizes responsible use and risk mitigation.

The Federal Reserve’s AI program for its staff promotes responsible AI use, enables innovation, and mitigates risks through robust governance frameworks. This regulatory guidance shapes how banks approach their own ML implementations.

Implementation Challenges and Risk Management

Data quality determines ML model performance. Banks often maintain data in siloed legacy systems with inconsistent formats, missing values, and documentation gaps. Consolidating clean training data requires significant engineering effort.

Model risk management frameworks must address development standards, validation procedures, performance monitoring, and governance processes. Banks need independent validation of ML models before production deployment and ongoing monitoring after launch.

Explainability requirements create tension with model complexity. Deep neural networks often deliver superior predictive accuracy but limited interpretability. Banks must balance performance against regulatory explainability requirements.

Bias detection and mitigation represent critical concerns. ML models trained on historical data can perpetuate past discrimination. Banks must test for disparate impact across demographic groups and implement bias correction techniques.

Cybersecurity risks expand with ML adoption. Adversarial attacks can manipulate model inputs to cause misclassifications. Model theft through API queries can extract proprietary algorithms. Banks need ML-specific security controls.

Vendor risk management becomes more complex when banks rely on third-party ML platforms, data providers, and model developers. Due diligence must assess vendor model development practices, data governance, and operational resilience.

Future Directions and Emerging Applications

Federated learning enables collaborative model training across institutions without sharing sensitive customer data. Banks can improve fraud detection and risk models by learning from industry-wide patterns while maintaining data privacy.

Quantum computing promises to accelerate ML training and optimization for portfolio construction, risk simulation, and cryptographic security. Though practical quantum advantages remain years away, banks are exploring potential applications.

Generative AI applications extend beyond chatbots to document generation, code development, regulatory report drafting, and synthetic data creation for model testing. These capabilities could dramatically reduce operational costs.

Real-time payment systems require fraud detection models that render decisions in milliseconds. Streaming ML architectures that process transactions as they occur will become standard infrastructure.

Climate risk modeling represents an emerging ML application. Banks need to assess physical risks to collateral, transition risks to carbon-intensive industries, and portfolio-level climate exposures. ML models analyze climate scenarios, supply chain vulnerabilities, and geographic risk concentrations.

Frequently Asked Questions

How do banks use machine learning for fraud detection?

Banks deploy ML models that analyze transaction patterns across dozens of features including amount, location, merchant type, time, device fingerprint, and historical customer behavior. When transactions deviate from expected patterns, the system flags them for review or blocks them automatically. According to Federal Reserve data, ML-driven fraud prevention and recovery totaled $4 billion in fiscal year 2024. These models continuously learn from new fraud cases and false positives to improve accuracy over time.

What’s the difference between traditional credit scoring and ML-based lending?

Traditional credit scoring relies on limited variables like payment history and credit utilization from credit bureau reports. ML-based lending incorporates hundreds of additional data points including bank account transaction patterns, utility payments, employment stability, and behavioral indicators. This enables banks to assess creditworthiness for applicants who lack traditional credit histories. DBS Bank’s ML system identified over 95% of non-performing SME loans three months before default, demonstrating the predictive power of these enhanced models.

Can machine learning models comply with banking regulations?

Yes, but compliance requires careful model design and governance. Banks must implement explainability techniques that document which factors influenced lending decisions, fraud flags, and risk assessments. Methods like SHAP values and LIME explanations break down ML predictions into interpretable components. The Federal Reserve’s AI program emphasizes responsible use and risk mitigation through robust governance frameworks. Banks need independent model validation, bias testing, ongoing performance monitoring, and documentation of model development processes.

How much are banks investing in machine learning?

Investment has accelerated significantly. Survey data shows 50% of financial services respondents increased ML and AI investments by more than 25% from 2023 to 2024. Adoption rates rose from 61% in 2023 to 77% in 2025. However, only 16% of banks using agentic AI have fully deployed production solutions, while 52% operate pilot projects. This indicates substantial investment in development and testing that hasn’t yet reached full-scale deployment across all institutions.

What are the biggest challenges in implementing ML in banking?

Data quality represents the primary challenge, as banks maintain information in siloed legacy systems with inconsistent formats. Model risk management requires validation procedures, governance frameworks, and ongoing monitoring. Explainability requirements create tension with complex model architectures. Bias detection and mitigation are essential to prevent discrimination. Cybersecurity risks expand with ML adoption, requiring protections against adversarial attacks and model theft. Regulatory uncertainty about governance standards and liability frameworks also constrains some deployment decisions.

How does machine learning improve anti-money laundering detection?

ML models analyze transaction networks to identify suspicious patterns that rule-based systems miss. They detect structuring behavior where criminals split large transactions to avoid reporting thresholds, circular fund flows, unusual beneficiary relationships, and geographic anomalies. HSBC, using Google Cloud’s AML AI, cut the number of alerts by more than 60% while finding 2–4 times more confirmed suspicious activity. This precision allows compliance analysts to focus investigative resources on actual threats rather than wasting time on false alarms.

What ML applications will become standard in banking over the next five years?

Real-time fraud detection will become ubiquitous infrastructure as instant payment systems grow. Conversational AI for customer service will expand beyond basic chatbots to handle complex requests with minimal human escalation. Predictive analytics for credit risk, customer churn, and product recommendations will shift from competitive advantage to standard practice. Climate risk modeling using ML will become regulatory requirements as financial authorities mandate climate stress testing. Process automation for document processing, reconciliation, and reporting will eliminate most manual back-office workflows.

Conclusion: Machine Learning as Banking Infrastructure

Machine learning has transitioned from experimental technology to operational infrastructure across the banking sector. The applications span fraud prevention, credit risk assessment, regulatory compliance, customer service, trading, and operational automation.

Federal Reserve data documenting $4 billion in fraud prevention and recovery demonstrates measurable impact. HSBC, using Google Cloud’s AML AI, cut the number of alerts by more than 60% while finding 2–4 times more confirmed suspicious activity.

The adoption trajectory is clear. Investment growth of 25% or more annually, implementation rates rising from 61% to 77% over two years, and widespread deployment of agentic AI all point toward ML becoming standard infrastructure.

Implementation challenges remain—data quality, model governance, explainability requirements, bias mitigation, and regulatory uncertainty. But these obstacles represent engineering problems, not fundamental limitations. Banks that solve these challenges will capture competitive advantages in fraud prevention, risk management, customer experience, and operational efficiency.

The institutions that treat machine learning as optional will find themselves unable to compete on costs, unable to detect sophisticated fraud, unable to deliver personalized experiences customers now expect. The technology has moved beyond competitive advantage to operational necessity.

Start evaluating where ML can address specific institutional pain points. Prioritize applications with clear ROI and manageable regulatory complexity. Build data infrastructure and governance frameworks that enable responsible deployment. The banks winning in 2026 and beyond will be those that operationalized machine learning today.